Here's what the insurance company won't tell you: on its own, a carrier's default move is to pay a claim at or near its face value, close the file, and call it a win. That's cheaper for them than fighting it, and it's not their premium that goes up afterward — it's yours. For a mid-sized healthcare employer — a nursing home, a home-health agency, a hospital — where injury frequency is highest, that default behavior is exactly how a manageable incident turns into a multi-year premium problem.

This guide covers how West Virginia workers' comp premiums actually accumulate, what drives them up, and what employers can do — at their own level — to reduce cost year over year. It's written the way we'd explain it to a business owner across the table, not the way an insurer would.

Key Takeaways

- WV workers' comp premiums compound across three factors: payroll by class code, the carrier's loss-cost multiplier, and the experience modification rate (EMR)

- The EMR is the highest-leverage cost driver — one large claim raises premiums across three future policy years, and once premiums rise they rarely come all the way back down

- The "lawyer number" on a claim (a $250,000 reserve) is rarely the real cost (~$30,000 in actual medical spend, paid ~$1,500–$2,000/month, not a lump sum) — but only if someone contests it

- Classification errors and padded payroll are routine overcharges most employers never catch; clerical staff shouldn't be rated like hands-on roles

- High-deductible program structures can roughly halve annual premium for qualifying businesses — not every business qualifies, and they have to be actively administered

How WV Workers' Comp Premiums Actually Build Up

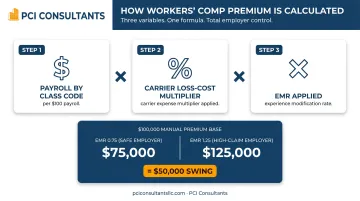

Workers' comp premium isn't a flat charge. It's a formula, and every variable in that formula compounds against the others.

The basic structure works like this:

- Payroll by class code — each employee's wages are assigned to an NCCI classification, each carrying its own loss cost per $100 of payroll

- Carrier loss-cost multiplier — the carrier layers its own expense multiplier on top of NCCI's advisory loss costs to produce the final rate

- Experience modification rate (EMR) — NCCI's multiplier based on your prior claim history, applied directly to the manual premium

NCCI's experience rating documentation illustrates this clearly: $100,000 of manual premium becomes $75,000 at a 0.75 EMR and $125,000 at a 1.25 EMR. That's a $50,000 swing on the same payroll and class codes — driven entirely by claims history. And here's the part that stings: once a claim pushes your EMR up, premiums rarely come all the way back down after the claim resolves. The increase sticks for years.

Why Cost Build-Up Is Gradual and Hard to See

The EMR uses up to three years of prior loss data, generally covering policies effective 21 to 57 months before the rating date. A claim filed today doesn't show up in the EMR calculation until the next renewal cycle — and its effect persists across three subsequent policy years.

Most employers see stable premiums right up until one high-severity loss triggers an EMR spike — translating to 20–50% higher premiums at renewal long after the original incident. By the time the increase hits the invoice, the window to influence the underlying number has already closed. That's why what happens in the first hours and weeks of a claim matters more than anything you can do at renewal.

The Real Cost of a Claim vs. the "Lawyer Number"

This is where most premium reduction is actually won or lost, and it's the part carriers are happy to leave alone.

When a worker is injured, a reserve gets set — the insurer's estimate of what the claim will ultimately cost. Left to the default process, that reserve balloons. A back injury at a nursing home gets a $250,000 reserve attached to it because that's the number an attorney would put on it. That inflated figure is what feeds your EMR and your renewal, whether or not the claim ever costs that much.

The actual cost is usually a fraction of it. In practice a claim reserved at $250,000 often resolves for around $30,000 in real medical spend — and it's paid incrementally, typically $1,500–$2,000 a month as treatment actually occurs, not as a lump sum written the day of the injury. The gap between the lawyer number and the real number is the money on the table. Nobody captures it for you automatically. Individual results vary, but the pattern is consistent: when someone contests the inflated reserve and manages the claim to its real cost, the employer's loss history — and future premium — reflect the real number instead of the scary one.

Why direct claims handling changes the math

At PCI Consultants, we handle the claim directly for the life of the policy — the employer calls us, not the insurer. That single change drives most of the difference:

- Day-one documentation. When an incident happens, we evaluate it immediately and may send the injured worker to urgent care right away. That creates an accurate, timely medical record of exactly what was and wasn't injured — the record that protects you if the claim is exaggerated weeks later.

- Legitimate claims paid, exaggerated ones contested. A genuine injury gets paid without a fight; that's the deal and it's the right thing to do. But an exaggerated or fraudulent claim gets investigated and contested instead of quietly paid at face value. That protects your loss history and your future premiums.

- We're not paid on your claims. Our revenue comes as commission from the insurer, not from how many claims you file or how large they are. We have no incentive to let a reserve sit inflated — we're incentivized to get it to its real number.

If you want to go deeper on how active handling reshapes an EMR, our overview of workers' compensation claims management walks through the mechanics.

Faster Return to Work: The Fastest Way to Cut a Claim's Cost

Every day an injured worker stays fully off-duty adds indemnity cost and reserve exposure — both of which feed the EMR. The most reliable lever to shrink a claim is getting that worker back to productive work quickly, even in a modified role.

In a healthcare setting this is very concrete. An injured nurse who can't be on the floor can often move into a light-duty, receptionist-type role within weeks — answering phones, handling intake, doing chart work — while they recover. The worker keeps earning, the indemnity clock slows dramatically, and the claim's real cost drops sharply. Instead of a lost-time claim that runs many months, it becomes a short modified-duty stint.

A formal, written program is what makes this repeatable rather than ad hoc. See how a structured return-to-work program and a documented light-duty policy turn this from a good intention into a claims-cost control. Individual results vary, but early, structured return to work is one of the few levers that pays off on nearly every claim.

Key Cost Drivers for WV Workers' Comp Premiums

The Experience Modification Rate (EMR)

The EMR is a multiplier NCCI calculates by comparing your actual losses to the expected losses for your industry class. Above 1.0 means you pay more than standard; below 1.0, less.

What makes it so consequential is the timing:

- NCCI's first unit statistical report is valued 18 months after policy inception and due by the 20th month

- Subsequent reports follow at 12-month intervals for open or reopened claims

- The full rating window spans three prior policy years

This means an inflated reserve on an open claim — even one that will eventually close for far less — can drag your EMR upward across multiple renewals before it resolves. For a WV healthcare employer running $300,000 in manual premium, the difference between a 0.85 EMR and a 1.20 EMR is roughly $105,000 per year, and that differential persists for three renewal cycles. This is precisely why letting an adjuster carry a $250,000 reserve on a claim that's really worth $30,000 is so expensive: you're paying the inflated number three times over.

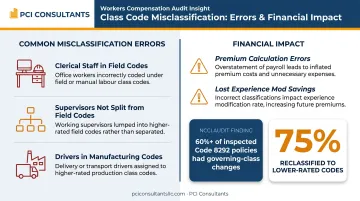

Risk Classification and Payroll Reporting

Every employee is assigned an NCCI classification code, and the loss-cost rates vary enormously between a clerical role and a hands-on, high-risk one. Getting this segmentation right is straight savings — you shouldn't be paying a floor-nurse rate on your billing and admin staff.

Common misclassification patterns include:

- Clerical and administrative staff lumped into higher-rated field or clinical codes

- Supervisory employees not split out from hands-on codes

- Drivers and transport staff assigned to the wrong classification

NCCI's classification research found that more than 60% of inspected policies with one common warehouse code had a governing-class change — most reclassified to lower-rated codes. Misclassification is the norm, not an edge case.

Beyond class codes, padded payroll inflates the base in ways employers rarely catch:

- Overtime premium (the excess above the straight-time rate)

- Expense reimbursements and uniform allowances

- Subcontractor or 1099 payroll applied to the policy without certificates of insurance on file

For closely held businesses and LLCs, West Virginia Code §23-2-1(d) also permits qualifying officers and members to elect exclusion from coverage, reducing the payroll base subject to premium. A proper carrier and coverage review catches these before the audit true-up, not after.

Policy Structure and Market Placement

Classification and payroll set the base — but two structural decisions shape what you actually pay, independent of claims history: where the policy is placed and how it's structured.

Market tier matters. WV's workers' comp market now has over 350 licensed carriers competing for business. Employers stuck in the assigned risk pool who have improved their safety record can often qualify for voluntary-market placement at materially lower rates.

Program structure matters just as much. Standard guaranteed-cost policies are the default — and for many larger employers, the most expensive option. Which brings us to the structure that changes the economics most.

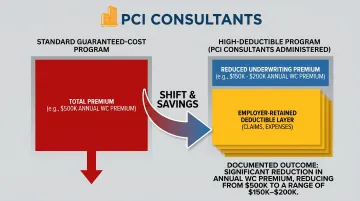

High-Deductible Programs: Roughly Halving Premium for Qualifying Employers

For the right employer, a high-deductible program is the single biggest lever available. The idea is simple: you take on a defined first layer of loss, and the insurer covers everything above it. Because the carrier's projected payout drops, the underwriting premium drops with it.

Here's the shape of it. On a program where the total exposure is, say, $500,000, the employer might retain the first $200,000 per the program design, with the insurer covering the rest. That structure can roughly halve the annual premium — moving an employer from around $100,000 to $50,000 a year in premium for a qualifying business. And the retained claims aren't pre-funded in a lump sum: they're paid monthly as treatment happens — on the order of ~$3,000/month — and the payments stop when the condition resolves. Cash stays on your balance sheet instead of being handed to the carrier up front.

The catch — and the reason this isn't a gimmick — is that a high-deductible program has to be actively administered. Someone has to manage every claim inside that retained layer to its real cost, because now those dollars are yours. That's exactly the direct-handling model described above, applied to a structure where it pays off most. Not every business qualifies — it depends on your loss history, cash flow, and size — and part of an honest review is telling you when it doesn't fit.

For employers weighing the trade-offs, our breakdown of large-deductible workers' comp and the self-insured / retention options covers who qualifies and how the numbers work. Individual results vary.

Cost-Reduction Strategies for WV Workers' Comp Premiums

Premium reduction starts with identifying where the excess cost originates: coverage design, claims management, or market positioning. Each source needs a different fix.

Strategies That Target Coverage Design

Run a classification code audit. Verify that every employee's class code reflects their actual primary duties, and that low-risk clerical roles aren't rated like high-risk hands-on ones. Mixed workforces — healthcare especially — routinely carry errors that produce four-to-six-figure annual overcharges. The fix is documentary and the recovery is often immediate.

Audit payroll inclusions before the true-up. Strip out overtime premium above straight-time, expense reimbursements and per diems, subcontractor payroll without certificates, and wages for officers who've elected exclusion under WV Code §23-2-1(d).

Evaluate a high-deductible structure — if you qualify. As above, this can roughly halve premium for qualifying businesses. Not every business qualifies, and it only works if the retained layer is actively managed.

Strategies That Target Claims Management

Once a policy is in force, the primary lever is controlling the claim outcomes that feed the next EMR.

Handle claims directly and immediately. Day-one evaluation, immediate urgent-care documentation, and active management of every open reserve is what keeps the lawyer number from becoming your real number. Left to the carrier's adjuster, reserves stay inflated, temporary disability outlasts the injury, and medical authorizations drag. Our loss-control and claims oversight approach exists to prevent exactly that.

Put a real return-to-work program in writing. Light-duty transitions — the injured nurse moved to a front-desk role within weeks — cut lost-time cost on nearly every claim.

Contest exaggeration; pay the legitimate. Genuine injuries get paid without dispute. Exaggerated or fraudulent claims get investigated so they don't quietly inflate your loss history for three years.

Read your EMR worksheet before renewal. Request your current experience-rating worksheet from NCCI to see which specific claims drive your modification, then dispute inflated reserves and push long-tail claims toward closure at defensible values before they lock into the unit-stat calculation.

Strategies That Target Market Context

Shop the voluntary market — and consolidate. With 350+ carriers licensed in WV, rates for the same risk vary widely. Employers in the assigned risk pool with improved loss history should actively seek voluntary placement. And if you own multiple locations — several nursing homes under one owner, for instance — those can often be consolidated onto a single master policy for better terms than each carrying its own.

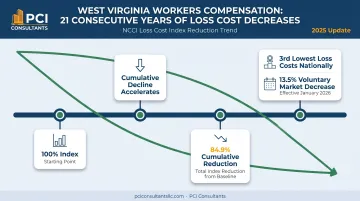

Benchmark against WV's rate trend. WV has posted more than 20 consecutive years of NCCI loss-cost decreases. If your renewals aren't trending down, your carrier or broker may not be applying current filings correctly.

Conclusion

Reducing WV workers' comp premiums isn't a matter of waiting for NCCI's annual filings to improve the baseline. Statewide decreases are real — but they lower the floor for everyone equally. The employers who outperform their peers do it by auditing classifications, defending their payroll base, and — above all — handling claims so the inflated "lawyer number" never becomes their real cost.

These variables compound, so early action pays off far more than late action:

- A classification error corrected before renewal saves money this year and every year after

- A claim managed to its real cost — $30,000 instead of a $250,000 reserve — improves the EMR for three renewal cycles

- A qualifying employer restructured into a high-deductible program can see premium roughly halved at day one

WV employers with 100+ employees and $100K+ in annual WC premium who haven't reviewed their program recently are likely paying more than their loss experience justifies. The concrete next step is simple: send us a copy of your current workers' comp policy and your five-year loss runs. With those two documents we can show you exactly where the excess cost lives — classification, claims, or placement — and whether a different structure fits. Not every business qualifies for every program, and individual results vary — but you'll know where you stand.

Frequently Asked Questions

How can I reduce workers' compensation premiums in West Virginia?

Three levers do most of the work: correcting job classification codes and payroll inclusions so you're not overpaying on low-risk staff, managing claims directly so inflated reserves don't compound into a higher EMR, and evaluating alternative structures — including high-deductible programs for qualifying businesses — in WV's competitive private market. Most employers find excess cost in at least two of these areas. The fastest way to know is to send your current policy and five-year loss runs for review.

Why does one claim raise my premium for years in West Virginia?

Because the EMR uses up to three years of prior loss data, a single claim affects your rate across three future policy years — and once premiums rise after a claim, they rarely come all the way back down even after it resolves. Worse, the number that feeds your EMR is often an inflated reserve (a "$250,000" figure) rather than the claim's real cost (often closer to $30,000, paid ~$1,500–$2,000/month). Contesting that reserve early is how you keep the real number, not the scary one, on your loss history. Individual results vary.

What does it mean that PCI handles the claim directly?

It means when a worker is injured, you call us, not the insurer. We evaluate the incident immediately, may send the worker to urgent care right away to create an accurate medical record, and then manage the claim to its real cost for the life of the policy — paying legitimate claims without dispute and contesting exaggerated ones. Left to the default process, a carrier tends to pay claims at or near face value and call it a win, because it's your premium that rises, not theirs.

Does West Virginia require employers to carry workers' compensation insurance?

Under WV Code §23-2-1, most employers regularly employing one or more persons must maintain workers' comp coverage. Limited exceptions apply to certain domestic-service, qualifying agricultural, and casual employers as enumerated in the statute.

What is a high-deductible workers' comp program, and would mine qualify?

You take on a defined first layer of loss (for example, the first $200,000 of a $500,000 exposure) and the insurer covers the rest. Because the carrier's projected payout drops, premium can be roughly halved for a qualifying business — retained claims are then paid monthly as treatment happens and stop when the condition resolves. The trade-off is that the retained layer must be actively administered, which is why not every business qualifies. A review of your loss history, size, and cash flow tells you whether it fits.

How do I get started reviewing my West Virginia workers' comp program?

Send us two documents: a copy of your current workers' comp policy and your five-year loss runs. That's enough for us to review your classifications, EMR drivers, and program structure and show you where the reduction opportunities actually are — usually within 24 hours. There's no obligation, and if a different structure doesn't make sense for you, we'll say so.