There's no single national answer. Workers' compensation is governed by state law, so coverage obligations depend on how a worker is classified, which state is involved, and what industry they work in. A contract that says "independent contractor" offers less protection than most employers assume. Misclassification can trigger retroactive premiums, civil penalties, and direct lawsuits, all at once.

This article covers the general rule on IC coverage, how classification is actually determined, the state-specific exceptions, the real cost of getting it wrong, and the practical steps that reduce your exposure. We'll also cover the part most articles skip: what happens to the claim and your premium after a contractor injury lands on your policy.

Key Takeaways

- Independent contractors are generally not covered by an employer's workers' comp policy by default.

- Worker classification, not job title or contract language, controls coverage obligations.

- Several states require workers' comp for ICs in construction and manual-labor roles.

- Misclassification can mean back premiums, civil penalties, and loss of the exclusive-remedy defense.

- A wrongly classified injury that lands on your policy raises your premium, and premiums rarely come back down once they rise.

- Certificates of insurance, well-drafted agreements, regular audits, and active claims oversight sharply reduce your exposure.

The General Rule: Workers' Compensation and Independent Contractors

Workers' compensation was built around the employment relationship. Benefits (medical expenses, partial wage replacement, rehabilitation costs) flow to employees, not independent contractors. Businesses are generally not required to carry coverage for ICs, who are expected to either carry their own policy or absorb the financial risk of a work-related injury themselves.

Why the 1099 Doesn't Settle It

A common misconception: if a worker receives a 1099 instead of a W-2, they're automatically an independent contractor for workers' comp purposes. That's not how it works.

Colorado's Division of Workers' Compensation states directly that "paying someone with a 1099 does not make them a contractor." Most state workers' comp agencies take the same position, tax forms are evidence, not conclusions.

South Carolina's Workers' Compensation Commission, for example, notes that 1099 payment status may still require coverage depending on control, equipment, and the employer's right to terminate.

The Health Insurance Gap

Here's something many ICs discover too late: standard health insurance typically doesn't cover work-related injuries. According to CMS, workers' compensation pays primary for health care tied to job-related illness or injury. Private health plans, including employer-sponsored group coverage, often exclude injuries for which workers' comp benefits are available.

For an uninsured IC hurt on the job, out-of-pocket costs can reach tens of thousands of dollars with no safety net. Voluntary workers' comp coverage fills that gap, and for businesses that regularly engage ICs in high-risk roles, it also reduces the misclassification liability that comes with leaving the question unanswered. It also changes who controls the claim, which, as you'll see below, is where most of the real money is won or lost.

Employee vs. Independent Contractor: How Classification Is Determined

Classification isn't what you call someone. It's what the actual working relationship looks like, and state agencies and courts dig into the facts.

The Factors Courts and Agencies Examine

Most states evaluate some combination of the following:

- Whether the worker controls how and when the work is done

- Whether they supply their own tools and equipment

- Whether they work for multiple clients simultaneously

- Whether they can profit or suffer a loss on the engagement

- Whether they maintain a separate business with independent liabilities

- Whether they're paid per job versus hourly

Courts weigh the totality of these factors. No single element decides the outcome, and different states assign different weights to each.

State Tests Vary Significantly

Different states apply meaningfully different frameworks:

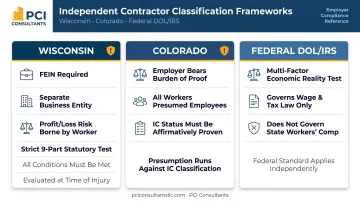

- Wisconsin uses a strict nine-part statutory test under Wis. Stat. 102.07(8)(b). All nine conditions must be met, including maintaining a separate business, having a federal employer identification number or business tax filings, and bearing the risk of profit or loss. The test is evaluated at the time of injury.

- Colorado presumes all workers are employees unless IC status is affirmatively proven. The burden is on the employer.

- Federal (DOL/IRS) tests use multi-factor economic-reality analyses, but these govern wage and tax law, not state workers' comp obligations.

The Moment-of-Injury Problem

Even a worker who legitimately qualifies as an independent contractor can shift into employee status if, at the moment of injury, they were operating under the hiring party's direct control or outside the scope of their own independent business. Wisconsin's framework makes this explicit: IC status is evaluated at the time of injury, not at the time of hire.

A framing subcontractor who spends most of the year working independently but follows detailed instructions on one particular job may be an employee for that job. A per-diem home-health aide sent to a specific patient on your schedule, using your supplies, may be too. That's precisely when injuries tend to happen, and it's exactly the moment you want an advocate managing the claim instead of a carrier deciding on its own how much to pay.

When Independent Contractors Must or Can Be Covered: State-by-State Variations

The general exclusion of ICs from mandatory coverage has significant exceptions. Businesses operating across multiple states need to know where the floor changes.

States With Construction-Specific Mandates

Construction has the densest set of IC-specific rules:

| State | Rule |

|---|---|

| Florida | Workers' comp law does not allow ICs in construction. A worker is either a business owner or an employee. Employers with one or more employees must carry coverage. |

| New York | Construction ICs must satisfy the two-part Construction Industry Fair Play Act test. Workers injured performing services for a contractor are presumed employees of that contractor. |

| California | Construction employers need coverage with just one employee. Certain license classifications (including C-39 Roofing) cannot claim a no-employee exemption. |

| Tennessee | Owners of construction businesses must carry workers' comp on themselves, though they may apply for an exemption. |

| Michigan | General contractors can be held liable for employees of uninsured subcontractors. |

Louisiana's Manual Labor Exception

Louisiana excludes independent contractors from coverage as a general rule, but Louisiana RS 23:1021 creates a statutory exception: ICs are expressly covered when a substantial part of their work time involves manual labor. This exception covers industries where hands-on physical work is the norm, including:

- Landscaping and tree service

- Construction trades

- Freight handling and transport

Voluntary Coverage and Its Risks

Beyond state-mandated exceptions, some states, including Texas, South Carolina, and Georgia, allow businesses to voluntarily elect workers' comp coverage for independent contractors through a specific form or policy endorsement.

There's a trade-off worth understanding: voluntarily covering an IC can be used as evidence that the employer treated that person as an employee. If coverage is extended without clear written disclaimers stating it doesn't constitute an acknowledgment of employment status, it can work against the employer in a later classification dispute. This is one of those places where the right paperwork, drafted up front, is worth far more than it costs.

The Real Cost of Misclassifying a Worker

When a state agency or court determines that a worker you classified as an independent contractor was actually an employee, the financial exposure is immediate, and it hits from multiple directions at once. Retroactive premiums, penalties, and uncovered injury claims can accumulate simultaneously.

What Employers Face

- Retroactive workers' comp premiums covering the entire misclassification period

- Civil penalties assessed on top of the premium liability

- Full out-of-pocket cost of any injury claim filed during that period

- Direct civil lawsuit exposure. Without valid coverage, the injured worker can bypass the workers' comp system entirely and sue in civil court for uncapped damages

California Labor Code 3706 makes this explicit: an injured employee whose employer failed to secure coverage may bring a civil action as though the workers' comp system never applied. Most states have equivalent provisions. The table below shows what the statutory penalty structures look like in practice.

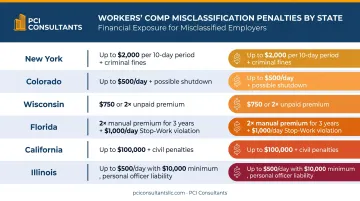

Penalty Exposure by State

| State | Penalty |

|---|---|

| New York | Up to $2,000 per 10-day period of noncompliance; criminal fines from $1,000 to $50,000 depending on employee count |

| Colorado | Up to $500 per day uninsured; business may be shut down |

| Wisconsin | Greater of $750 or twice the unpaid premium during the uninsured period |

| Florida | 2x the manual premium that would have been paid for up to 3 years of noncompliance; $1,000/day for violating a Stop-Work Order |

| California | Up to $100,000; civil penalty of twice the premium or $1,500 per employee (whichever is greater) where no compensable injury occurred |

| Illinois | Up to $500/day with a $10,000 minimum; corporate officers may be personally liable |

State agencies apply these figures routinely, not as a last resort. For an employer already paying $100K or more in annual WC premium, a misclassification finding can effectively double the cost of coverage retroactively.

The Cost Most Employers Never See Coming: What the Injury Does to Your Premium

The penalty table is the visible bill. The quieter, bigger one shows up in your loss history. When a contractor injury gets reclassified onto your policy, the carrier doesn't just pay the claim; it reserves it, and reserves are usually set at a worst-case "lawyer number." We routinely see a strain injury opened with a $250,000 reserve when the actual medical spend, managed properly, is closer to $30,000, paid incrementally at roughly $1,500 to $2,000 a month rather than as a lump sum. Left alone, the insurer often pays at or near that inflated face value and calls it a win, because it isn't their premium that goes up afterward.

Yours does. Once a claim inflates your experience rating and pushes your premium up, that increase rarely comes back down after the claim resolves. You can be paying for a single mishandled contractor injury for years. That multi-year drag is why active claims management matters more than the sticker price of the policy, and why we handle the claim directly rather than leaving it to the carrier's default settings.

How Employers Can Protect Their Business

Reducing IC-related workers' comp exposure comes down to a handful of practical habits, plus one thing most articles leave out: who runs the claim when an injury actually happens.

Require certificates of insurance before work begins. Every independent contractor should provide a current COI showing their own workers' comp coverage. Keep those certificates on file and verify renewal dates. An expired certificate offers no protection.

Use well-drafted IC agreements. Contracts should reflect the actual working relationship: who controls the work, who supplies equipment, how payment is structured, and whether the contractor works for other clients. A contract that contradicts reality won't survive scrutiny.

Audit contractor relationships regularly. A worker who starts as a true IC can drift toward employee status as their role evolves: more direction, more integration into operations, fewer other clients. Periodic reviews catch that drift before a claim or an audit does.

Classify your real workforce by actual risk. Your clerical staff should not be rated at the same risk as your hands-on crews. When roles are segmented properly, you stop overpaying premium on low-risk people, which frees up budget and makes the whole program more defensible at audit time.

Have someone managing the claim from day one. The single biggest lever on a contractor injury's real cost is what happens in the first 48 hours. When a legitimate injury occurs, the right move is often to get the worker to urgent care immediately and build an accurate, timely medical record, then transition them to light duty (an injured crew member to a scheduling or intake role) within weeks. That record protects you against later exaggeration and cuts the real claim cost sharply.

Where Workers' Comp Consultants Add Value

For businesses with complex or high-volume contractor arrangements (construction, staffing, home care, trucking), working with a workers' comp specialist matters. These are the industries where the employee-IC line is contested most often and where the financial consequences of misclassification are highest.

PCI Consultants brings over 30 years of workers' compensation program experience to exactly these verticals. A few things that separate active management from a policy that just sits in a drawer:

- We handle the claim directly. When a worker is hurt, you call us, not the insurer, for the life of the policy. We evaluate the incident immediately, pay legitimate injuries without dispute, and investigate and contest the exaggerated or fraudulent ones. Genuine claims get handled fairly; inflated ones get challenged, which protects your loss history and your future premiums. Because we're paid by commission from the insurer rather than by claim volume, we're not incentivized to let your claims run high. See how our claims management and fraud prevention work fits together.

- We defend your payroll at audit. One of the most common and costly carrier audit errors is subcontractor payroll being attributed to your policy when the subcontractor carried their own coverage. Getting that attribution right can mean the difference between an accurate premium and a five-figure overcharge.

- We write the disclaimers correctly. If you choose to cover ICs under your policy, the coverage documentation and IC agreement should both state that extending coverage does not acknowledge employment status. That small step keeps the coverage from being weaponized against you later.

For businesses that qualify, we can also structure higher-deductible and alternative programs so you take on a defined first layer of risk while the insurer covers the rest, actively administered by us, not every business qualifies, but for the ones that do it can meaningfully lower annual premium. Individual results vary.

Frequently Asked Questions

Does workers' compensation cover independent contractors?

Not by default. Workers' comp coverage is designed for employees, and businesses are generally not required to extend it to ICs. Exceptions exist in certain states and industries, particularly construction and manual labor, and misclassification can create retroactive coverage obligations regardless of what the contract says. If you regularly use contractors, the smarter question isn't just "am I required to cover them" but "if one gets hurt and it lands on my policy, who's managing that claim so it doesn't balloon."

What happens if a subcontractor doesn't have workers' compensation insurance?

If an uninsured subcontractor is injured and later found to be an employee, the hiring business becomes liable for the full claim cost plus penalties. In states like Florida, a Stop-Work Order can follow until coverage is secured, and where no policy existed, the injured worker may pursue civil damages directly against the employer. This is also where carriers frequently over-charge at audit, so it's worth reading more on subcontractor payroll and audits and on hiring a contractor without workers' comp.

What is the new independent contractor rule?

The DOL's updated rule under 29 CFR Part 795, effective March 11, 2024, restores a multi-factor "economic reality" test to classify workers as employees or ICs, but it governs wage and labor law under the FLSA, not workers' comp. States apply their own separate classification tests for coverage purposes.

Can an independent contractor purchase their own workers' compensation insurance?

Yes. ICs can buy their own workers' comp policy voluntarily in most states. This is particularly important for sole proprietors doing physical work, since standard health insurance typically excludes work-related injuries for which workers' comp benefits would otherwise apply. Carrying your own policy also means you, not the hiring party's carrier, have a say in how a claim is handled.

Are 1099 workers covered by workers' compensation?

Not automatically, but receiving a 1099 doesn't automatically exclude a worker either. If the actual working relationship resembles employment under state classification tests, the employer may owe coverage and face penalties regardless of how the worker was paid or what tax form was issued.

How much does a misclassified contractor injury really cost me?

More than the claim itself, and for longer. The claim may be reserved at an inflated "lawyer number" (say, $250,000) even though the true, actively managed cost is closer to $30,000 paid incrementally at roughly $1,500 to $2,000 a month. On top of that, once the claim inflates your experience rating, your premium goes up and rarely comes back down after the claim closes. That's why the value is in managing the claim from day one, not just buying the policy. Individual results vary.

Not Sure Where Your Contractor Exposure Sits? Let's Look.

The fastest way to know whether your contractor payroll is classified correctly, whether your premium reflects your real risk, and whether any open claim is being managed or just paid, is a policy review. Send us two things: a copy of your current workers' comp policy and your five-year loss runs. We'll tell you where your exposure actually is and what it would take to bring it down. Not every business qualifies for every program, and individual results vary, but the review itself costs you nothing but the paperwork.