The numbers behind the churn are stark. According to BLS JOLTS data for Accommodation and Food Services, total annual separations ran 83.6% in 2022 and 75.4% in 2023 before moderating to roughly 65% in 2024. Black Box Intelligence reported that rolling-12 hourly turnover in limited-service restaurants still hovered around 110% through Q3 2025. That is a nearly continuous cycle of new, inexperienced workers — the group most likely to get hurt.

This article covers why that cycle exists, how it mechanically inflates premiums through the Experience Modification Rate (EMod), why the damage compounds over three years, and — the part most brokers gloss over — how the way a claim is actually handled determines whether it costs you the face value the insurer reserves or a fraction of it.

Key Takeaways

- Restaurant turnover regularly exceeds 70–80% annually, creating a near-permanent pool of first-year workers, statistically the highest-risk group for on-the-job injuries.

- Premiums are driven by payroll and claims history; turnover inflates injury frequency and the EMod multiplier that sets your actual rate.

- Each claim stays in the EMod calculation for three years, so one bad turnover-driven year costs you at three consecutive renewals — and premiums rarely fall back to where they started even after a claim resolves.

- Left to their own devices, insurers tend to pay claims at or near face value and call it a win. Who manages the claim — and how fast — often matters more to your real cost than how many claims you have.

Why Restaurant Employee Turnover Is Chronically High

The restaurant industry doesn't have a turnover problem the way other industries do. It has a structural design that produces turnover as a predictable output.

The Workforce Is Built for Churn

The BLS notes that food and beverage service work commonly involves part-time schedules covering early mornings, late evenings, weekends, and holidays — hours that attract students, transitional workers, and people supplementing other income, not workers building long-term careers. A 2019 ICHRIE study found part-time restaurant employees had significantly higher turnover intentions than full-time staff, with roughly one-third of restaurant employees working part time. The median hourly wage for food and beverage workers was $14.92 in May 2024 — low enough that small income improvements elsewhere trigger departures.

The Conditions That Keep People From Staying

Beyond workforce composition, the work itself drives exits. The factors that push people out are operational, not incidental:

- Physically demanding shifts on your feet for 6–8 hours straight

- Inconsistent scheduling that makes personal planning difficult

- Tip-dependent income that swings week to week

- Limited promotion paths, especially in single-location operations

- Management quality issues that are hard to screen for at hiring

Most operators have accepted this as normal, which is exactly why the downstream workers' comp costs rarely get traced back to their source.

The Low-Entry, High-Exit Trap

Anyone can get hired. The conditions that cause people to leave — physical toll, irregular pay, stress — are baked into the operating model. The comp costs that follow every round of new hires are a direct consequence, and most operators never connect the two.

New Workers, Higher Risk: The Turnover-Injury Connection

The relationship between employee tenure and injury risk is well-documented — and it matters enormously for restaurants.

What the Data Shows

Travelers' 2025 Injury Impact Report found that more than one-third of all workplace injuries occur during the first year of employment, accounting for one-third of total claim costs. WCIRB California data found workers with less than one year of tenure generated approximately 40% of workers' compensation claims and were more than twice as likely to file a claim as the statewide average. When annual turnover runs at 80–110%, the average tenure across your line at any given moment is very short — which means your exposure is concentrated in exactly the highest-risk group.

Why Kitchens Amplify the Risk

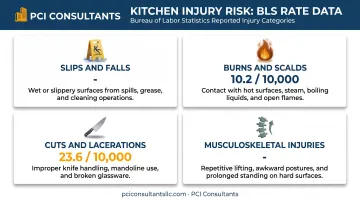

A restaurant kitchen is not a forgiving place for someone in their second week. The hazards are real and constant:

- Slips and falls — wet floors from spills, mopping, and dishwashing

- Burns and scalds — fryers, ovens, hot liquids, steam

- Cuts and lacerations — knives, mandolines, box cutters during receiving

- Musculoskeletal injuries — repetitive prep motion and heavy lifting in stocking

BLS data for full-service restaurants shows cuts and lacerations at 23.6 per 10,000 workers and thermal burns at 10.2 per 10,000. Experienced workers develop habits that prevent most of these — they know where the wet spots form and how to carry a sheet pan without burning a forearm. A new hire hasn't built that muscle memory yet.

The Training Gap Nobody Talks About

High turnover means you're in a near-constant state of onboarding, which compresses safety instruction. This isn't negligence — it's a capacity problem. There simply isn't time for thorough workplace safety and return-to-work training when the same role turns over every few months. There's also a behavioral dynamic that rarely gets acknowledged: new employees don't speak up. They won't refuse an unsafe task or flag a wet floor to a supervisor they've known three days. They absorb those lessons through trial and error — and sometimes through an injury report.

How Workers' Comp Premiums Are Calculated — and Why Turnover Matters

Understanding your premium requires understanding two numbers: payroll and the Experience Modification Rate (EMod).

The Two Premium Drivers

Payroll sets the base. Comp premium is calculated per $100 of payroll within your class code. More payroll, higher base premium. This is also where risk classification matters: a well-run program segments your workforce by actual risk, so front-of-house and clerical payroll isn't rated as if it were line-cook payroll. Get the class codes wrong and you overpay on your lowest-risk roles all year.

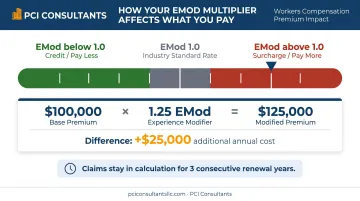

The EMod is where turnover does its real damage. According to NCCI's experience rating documentation, the EMod is a multiplier applied to your base premium based on three years of your actual claims history versus industry peers:

- EMod of 1.0 = you pay the industry standard rate

- EMod above 1.0 = you pay more (a 1.3 EMod pays 30% above standard)

- EMod below 1.0 = you receive a credit and pay less

NCCI's own example: a 1.25 EMod on a $100,000 manual premium produces a $125,000 modified premium. That extra $25,000 recurs at every renewal until your loss history improves — and as any operator who's lived through it knows, premiums are far stickier on the way down than on the way up.

The Three-Year Window

The EMod uses three years of claims data — typically the three most recent policy years, excluding the current one. A single bad year of claims doesn't just hurt this renewal; it sits in the calculation for three consecutive renewals before aging out. One frequency-heavy turnover year can quietly tax you three times.

Why Turnover Inflates the EMod

Claim frequency drives EMod damage. NCCI's formula weights how often claims occur through what it calls primary losses — the amount of each claim up to the split point. A high volume of smaller claims can damage your EMod more than a single large claim of equal total cost. High turnover produces exactly this pattern: more first-year workers on the line, more incidents, more claims, more primary-loss dollars entering the formula. Even modest burns and lacerations, in volume, signal a high-risk operation to both the formula and the underwriter.

The payroll audit is a second exposure. More employees cycling through means total auditable payroll can exceed the estimate at inception — especially when tip income and overtime are handled incorrectly — producing surprise audit invoices at year-end.

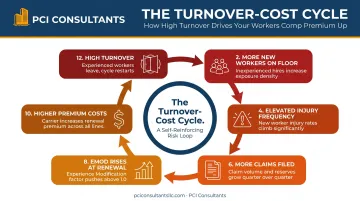

How Turnover Directly Drives Up Your Premiums — and the Claim Nobody Manages

The chain of causation is direct. A restaurant replaces a departed employee, the new hire — statistically more likely to be injured — gets hurt in month two, a claim is filed, the EMod rises at renewal, the premium increases. But there's a second, quieter driver that most operators never see: how the claim itself is handled.

The "Lawyer Number" vs. the Real Cost

Here's what the insurance company won't tell you. Left to its own devices, an insurer tends to reserve a claim high and pay it at or near face value — that's the path of least resistance, and closing it out counts as a "win" on their books, not yours. A dishwasher's shoulder injury can get reserved as a "$250,000 claim." The actual medical spend on that same injury is often closer to $30,000, and it isn't paid as a lump sum — it's paid incrementally, typically around $1,500–$2,000 a month, until the condition resolves. The gap between the scary reserve number and the real, incremental cost is where an active advocate saves you money. Nobody minimizes that cost unless someone is actively working the file. Individual results vary.

This is the core of how direct claims management changes the math. When PCI handles a claim, the operator calls us — not the insurer. We evaluate the incident immediately and, when warranted, send the injured worker to urgent care that same day. A prompt, accurate medical record created on day one protects you against a claim that gets exaggerated weeks later, and it starts the clock on resolution before reserves have a chance to balloon.

Frequency Matters More Than You Think

Underwriters read claim frequency as a signal of risk culture — often more heavily than severity. A restaurant with five small claims looks riskier than one with a single large claim of the same total cost. High turnover multiplies the number of at-risk new-worker periods across the year, so it drives frequency directly. Ten modest kitchen injuries can do more EMod damage than one significant claim.

Genuine Injuries Get Paid — Exaggerated Ones Get Contested

High-frequency environments attract a share of exaggerated and, occasionally, outright fraudulent claims — the "I hurt my back on the weekend but reported it Monday" pattern. Our stance is simple and it protects your loss history: a genuine injury is paid without dispute, quickly and fairly. A claim that doesn't add up gets investigated and contested. That day-one medical record is often the deciding evidence, and screening out inflated claims keeps them from padding the three-year EMod window and your future premiums. You can read more on how fraud and exaggeration screening fits into a comp program.

The Costs You Don't See on the Invoice

Direct claims costs are only part of the picture. OSHA's indirect cost data shows that for smaller claims (under $3,000 in direct costs), indirect costs can run 4.5 times the direct cost — lost productivity, supervisor time on modified-duty logistics, replacement training, and overtime to cover the gap. And every claim needs someone to manage it through resolution. Because PCI is paid by commission from the carrier rather than by your claim volume, we're not incentivized to let claims run — the opposite: our job is to close them at their real cost, fast.

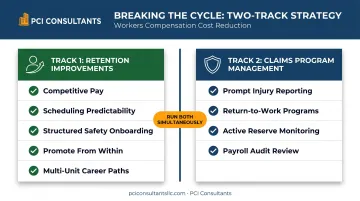

How to Break the Cycle: Reducing Turnover-Driven Costs

Breaking the cycle means working two tracks at once. Fixing only turnover or only claims leaves money on the table.

Track One: Retention Improvements

Keeping workers long enough to develop injury-preventing experience lowers your baseline exposure. Key levers:

- Competitive pay relative to local alternatives — Cornell research links lower turnover to higher relative wages

- Scheduling predictability that attracts workers who need reliability

- Structured onboarding with real safety training, not a checklist signed on day one

- Promotion from within so experienced workers have a reason to stay

- Multi-unit career paths across locations

None of these are quick fixes, and food-service turnover will never hit zero — which is why Track Two has to run in parallel.

Track Two: Active Workers' Comp Program Management

Some turnover is unavoidable; disciplined management limits the financial damage. The highest-leverage actions:

- Direct, day-one claims handling — you call us, we evaluate the incident immediately and create an accurate medical record before it can be inflated.

- Fast return-to-work on light duty — an injured line cook moved to a host or expo-type role within weeks stays on a medical-only footing instead of lost-time status, which carries far less weight in the EMod formula and sharply cuts the real claim cost.

- Active reserve monitoring — so aging claims don't carry inflated reserves into the EMod calculation.

- Class code and payroll audit review — tip income and overtime are routinely misvalued at restaurant audits, producing overcharges we contest.

Structural Options for Qualifying Operators

For larger multi-unit groups, the program structure itself can be re-engineered. High-deductible workers' comp programs let the employer take on a defined first layer of risk — for example, the first $200,000 of a $500,000 program — while the carrier covers the rest. For qualifying businesses, that structure can roughly halve annual premium (say, from $100,000 down to $50,000). Claim payments inside the deductible are then structured monthly — on the order of $3,000 a month — and stop when the condition resolves, rather than being fronted as a lump sum. It only works when the claims are actively administered, which is exactly what we do. Not every business qualifies, and it typically fits operators with $100,000 or more in annual comp spend and the loss history to support it. Multi-location owners — several restaurants under one entity — can often consolidate into a single master policy for better terms.

PCI Consultants works specifically with restaurant and hospitality operators facing this challenge. With more than 30 years placing and actively managing comp programs for high-turnover, high-frequency environments, we combine carrier placement with in-house claims handling, return-to-work, fraud screening, and payroll-audit defense — the areas where restaurant operators consistently overpay. If you also work with a staffing partner or PEO, it's worth understanding how a PEO arrangement affects hospitality comp before you renew.

The concrete next step: to quote your account or take over your current coverage, we need two things — a copy of your current workers' comp policy and your five-year loss runs. Send those over and we'll show you, claim by claim, where the turnover-driven frequency is actually costing you and what a managed program would look like. Individual results vary.

Frequently Asked Questions

Why is staff turnover so high in the restaurant business?

Low entry barriers plus a workforce that skews part-time, student, and transitional — people who don't view the role as a long-term career. Physically demanding conditions, tip-dependent income swings, and inconsistent scheduling compound it, producing exits that no single retention tactic fully prevents. The comp cost of that churn is what most operators miss.

How does employee turnover affect workers' comp premiums?

More turnover means more first-year workers on the line at any moment, and first-year workers are statistically more than twice as likely to file a claim. That raises injury frequency, drives up claim counts, and elevates the Experience Modification Rate applied to your base premium at renewal. It's a direct mechanical relationship — and because premiums are sticky, the increase tends to outlast the claim that caused it.

What is an Experience Modification Rate (EMod), and why does it matter for restaurants?

The EMod is a multiplier on your base premium based on three years of claims history versus industry peers. High-turnover restaurants often carry an EMod above 1.0, meaning they pay above standard at every renewal until their record improves. Frequency of small claims hurts it more than most operators expect, so how each claim is managed and closed directly shapes the number.

Are new restaurant employees really more likely to get hurt?

Yes. Travelers found more than one-third of all workplace injuries occur in the first year of employment, and WCIRB California found sub-one-year workers were more than twice as likely to file a claim as the statewide average. A restaurant with constant turnover has a disproportionate share of first-year employees on the floor at any given time.

If a worker files a claim, does it automatically cost six figures?

Usually not — though you might think so from the reserve. Insurers tend to reserve high and, left alone, pay at or near that face value. A genuine but modest injury reserved as a "$250,000 claim" often carries real medical costs closer to $30,000, paid incrementally at roughly $1,500–$2,000 a month until it resolves, not as a lump sum. Actively working the file — day-one medical records, fast light-duty return, reserve monitoring — is what keeps the real cost near the true number. Individual results vary.

What workers' comp options exist for restaurants with high turnover and rising premiums?

Alongside direct claims handling and return-to-work, larger multi-unit operators — typically those with $100,000 or more in annual comp spend — may qualify for high-deductible structures that can substantially cut upfront premium versus standard guaranteed-cost rates. Not every business qualifies. The fastest way to find out is to send your current policy and five-year loss runs so a specialist can read your actual turnover-driven claim pattern, something a standard broker relationship typically misses.