That eligibility is settled law. The part almost nobody explains to skilled nursing facility (SNF) operators is what happens after a worker gets hurt — who runs the claim, what it really costs, and how much of that cost is avoidable. Nursing homes carry some of the highest injury rates of any industry, recording roughly 6.3 injuries per 100 full-time workers a year. Left on autopilot, that injury frequency turns into a multi-year premium problem, because insurers, by default, tend to pay claims at or near face value, book it as a "win," and let your experience mod absorb the damage.

This article covers eligibility rules, common covered injuries, available benefits, how a claim actually gets filed — and, most importantly for operators, how a broker who manages the claim directly can keep a single injury from becoming a five-year cost.

Key Takeaways

- Every California employer with at least one employee must carry workers' comp — nursing homes of any size are included, no exceptions

- Coverage is no-fault — legitimate injuries get paid without the worker proving negligence

- The size of a claim is rarely fixed: inflated reserve figures and "lawyer numbers" often bear little relation to actual medical spend

- Once a claim pushes your premium up, it rarely comes back down — so how the claim is handled on day one matters for years

- For qualifying SNF operators, high-deductible program structures can roughly halve annual premium; not every business qualifies

- The fastest way to see where you're overpaying: send your current policy and five-year loss runs for review

California's Workers' Comp Law: What Nursing Home Employers Must Know

The Legal Foundation

California Labor Code Section 3700 requires every employer with one or more employees to secure workers' compensation coverage. Nursing homes and long-term care facilities are not exempt — regardless of size, bed count, or facility type. The California Division of Workers' Compensation (DWC) monitors compliance and administers claims statewide.

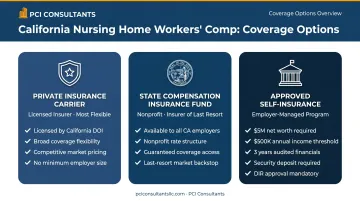

Three Ways to Secure Coverage

Nursing home operators have three options:

- Private insurance carrier: Purchase a policy from any licensed insurer operating in California

- State Compensation Insurance Fund (State Fund): A nonprofit, state-operated insurer that serves as California's insurer of last resort

- Approved self-insurance: Requires state approval through the Office of Self-Insurance Plans (OSIP), including a net worth of at least $5 million, annual net income of at least $500,000, three years of audited financials, and a security deposit

Here's what the insurance company won't lead with: which structure you pick, and who administers the claims underneath it, drives your cost far more than the sticker premium. A guaranteed-cost policy from a carrier with no advocate on your side means the insurer decides what each claim is worth — and their default is to pay generously and move on. That's the gap active claims management is built to close. For a deeper look at the alternatives to a plain guaranteed-cost policy, see our overview of alternatives to traditional workers' comp insurance.

Consequences of Non-Compliance

Operating without coverage is a criminal misdemeanor under Labor Code Section 3700.5, carrying:

- Fines starting at $10,000 (or double the avoided premium, whichever is greater)

- Up to one year in county jail

- Civil liability for all workers' comp benefits if an employee is injured, plus exposure to a direct lawsuit under Labor Code Section 3706

- Stop-work orders halting operations until coverage is obtained, plus penalties of $1,500 per employee

Which Nursing Home Workers Are Eligible for Workers' Comp?

Who Is Covered

Eligibility is broad. Any individual classified as an employee at a California nursing home or skilled nursing facility is covered — including:

- CNAs and nursing assistants

- LVNs and RNs

- Dietary and kitchen staff

- Housekeeping and laundry personnel

- Activities coordinators

- Administrative and billing staff

Part-time, per-diem, and temporary workers are covered under the same rules as full-time employees. Hours worked do not affect eligibility.

That breadth is exactly why risk classification matters on the employer side. Your billing clerk and your floor CNA carry wildly different injury risk, and they should not sit in the same rate bucket. When clerical or supervisory payroll gets misallocated to high-rate clinical codes, you overpay on people who will almost never file a lifting claim. Segmenting the workforce by actual risk is one of the first things we audit — see how this fits into a broader California risk management and workers' comp program.

The Independent Contractor Question

Some nursing homes attempt to classify workers as independent contractors to avoid workers' comp obligations. California's AB5 makes this difficult. The ABC test presumes every worker is an employee unless the hiring entity can prove all three prongs:

- A — The worker is free from the employer's control and direction

- B — The work falls outside the usual course of the facility's business

- C — The worker is independently established in that same type of work

In practice, most workers performing standard nursing home functions fail prong B entirely, meaning they qualify as employees and are entitled to coverage.

Agency-Placed Staff

When a nursing home hires workers through a staffing agency, Labor Code Section 2810.3 creates shared liability between the facility and the agency for coverage failures — applying when the facility has 25 or more workers or receives more than 5 workers from a labor contractor. Confirm which entity carries coverage before an injury forces the question.

No-Fault Coverage

Regardless of who employs them, workers get the same no-fault protection. An injured nursing home worker does not need to prove employer negligence — if the injury arose out of and in the course of employment, benefits are owed, even if the worker was partly at fault. This is the point advocates on the employer side are firm about: a genuine injury gets paid, promptly and without a fight. The scrutiny is reserved for claims that are exaggerated or fabricated.

Most Common Injuries Among Nursing Home Workers in California

Overexertion and Musculoskeletal Injuries

Patient handling is the leading cause of injury in nursing homes — lifting, repositioning, and transferring residents produce back injuries, herniated discs, shoulder strains, and muscle tears at a rate that outpaces most other industries. BLS 2024 data puts the total recordable injury rate for skilled nursing facilities at 6.3 per 100 full-time workers, with a days-away-from-work rate of 4.5.

Slips, Trips, and Falls

Wet floors, equipment in hallways, and constant movement between rooms create elevated fall risk — commonly fractures, head injuries, and sprains serious enough to pull workers off the floor for weeks.

Injuries from Resident Aggression

Nursing home workers regularly face scratching, biting, hitting, and other altercations from residents with dementia, Alzheimer's, or behavioral conditions. These are compensable under Labor Code Section 3600, which covers any injury arising out of and in the course of employment.

Needlestick Injuries and Infectious Disease Exposure

CNAs and nurses face exposure to bloodborne pathogens and communicable diseases including hepatitis, MRSA, and COVID-19. Under Labor Code Section 3208, occupational illness caused by workplace exposure is treated as an "injury," with the same coverage and filing rights as physical trauma.

Cumulative Trauma

Months and years of bending, lifting, and pushing equipment can produce cumulative trauma disorders. Labor Code Section 3208.1 defines these as repetitive activities whose combined effect causes disability. The "date of injury" is when the worker first suffered disability and knew, or should have known, it was work-related — which is exactly the kind of open-ended claim that inflates if nobody is managing it.

What Benefits Do Nursing Home Workers Receive?

California workers' comp covers five main benefit categories, from immediate medical care through long-term disability and death benefits.

Medical Care

All reasonably necessary treatment is covered — emergency care, hospitalization, surgery, physical therapy, prescriptions, and equipment. Care may route through the employer's Medical Provider Network (MPN) depending on policy structure. This is where day-one handling counts: a broker who evaluates the incident immediately and sends the worker to urgent care right away creates an accurate, timely medical record — the single best protection against a strain that gets exaggerated into a spinal claim weeks later.

Temporary Disability (TD) Benefits

Workers unable to perform their duties while recovering receive about two-thirds of average weekly wages, subject to a state minimum and maximum that adjust annually. TD is also the benefit that shrinks fastest under a real return-to-work program: moving an injured nurse into a light-duty receptionist-type role within weeks converts a lost-time claim toward medical-only and stops the wage-replacement clock.

Permanent Disability (PD) Benefits

A lasting impairment — chronic back damage, permanent nerve injury — may entitle the worker to long-term wage replacement. The payout depends on the disability rating assigned by a physician, the worker's age at injury, and their occupation.

Supplemental Job Displacement Benefit (SJDB)

Workers who cannot return to their prior job due to permanent disability may receive a nontransferable voucher of up to $6,000 for retraining, certification, or education at an approved institution.

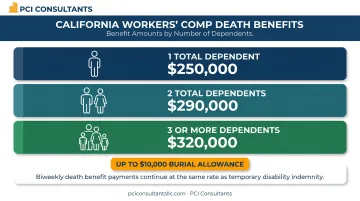

Death Benefits

If a worker dies from a work-related injury or illness, qualifying dependents receive ongoing death benefits paid biweekly, plus a burial allowance. Lump-sum amounts scale with the number of total dependents — rising with each additional dependent.

How to File a Workers' Comp Claim as a Nursing Home Worker

Step 1: Report the Injury in Writing

Notify your employer in writing as soon as possible. California requires written notice within 30 days of injury under Labor Code Section 5400 — missing it can forfeit eligibility. For occupational illness or cumulative trauma, the clock starts when disability first appears and the worker knew, or should have known, it was work-related.

Step 2: Complete the DWC-1 Claim Form

The employer must provide a DWC-1 form within one working day of learning about the injury. The worker completes Part A; the employer completes Part B and forwards it to the claims administrator — also within one working day. Once the completed form is received, the employer must authorize up to $10,000 in medical treatment within that same window.

On well-managed programs, the employer isn't chasing this paperwork alone. With PCI Consultants, the facility calls us, not the insurer — we evaluate the incident, trigger the medical record, and run the claim from the first hour. For a broader picture of how that works, see our workers' compensation claims management service.

If a Claim Is Disputed or Denied

A denial is not final. Injured workers can request an Independent Medical Review (IMR) for treatment disputes, file for a hearing before the Workers' Compensation Appeals Board (WCAB), or consult a workers' comp attorney. Employers, meanwhile, should never rubber-stamp a questionable determination — strong documentation and early claims involvement are what separate a $30,000 outcome from a $250,000 one.

How Nursing Home Employers Can Manage Workers' Comp Costs

Why SNF Premiums Run High — and Stay High

California classifies skilled nursing facilities under a high-risk category (WCIRB Classification 8829), which pushes base rates above most industries. Injury frequency then compounds through the experience modification rate (X-Mod): each claim inflates the mod for three consecutive policy years. And here's the part operators feel most — once premiums rise after a claim, they rarely come all the way back down, even after the claim resolves. That's why the number attached to a claim on day one is really a multi-year number.

The "Lawyer Number" Problem

Ask an operator what a serious lifting injury "costs" and you'll often hear a figure like $250,000 — the reserve the insurer set, or the number a plaintiff's attorney floated. The actual medical spend on that same injury is frequently closer to ~$30,000, paid incrementally — often around $1,500–$2,000 a month — not handed over as a lump sum. An insurer with no advocate on your side has little reason to correct that inflated figure; they'll reserve high, pay high, and let your mod carry it. A broker managing the claim directly works the number down to what the injury actually costs. Individual results vary, but the gap between the "lawyer number" and the real number is where most of the savings live. Our guide on whether workers' comp goes up after a claim covers the stickiness problem in more depth.

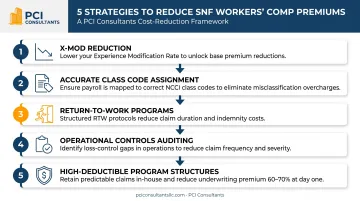

Levers That Actually Move the Number

- Direct claims handling — The facility calls the broker, not the carrier; incidents are evaluated immediately and a same-day medical record is created to protect against later exaggeration

- Fraud and exaggeration detection — Legitimate claims are paid without dispute; exaggerated or fabricated ones are investigated and contested, protecting your loss history and future premiums

- Fast return to work — Light-duty transitions within weeks convert lost-time claims toward medical-only, directly lowering the mod over successive years

- Accurate class-code assignment — Splitting clerical and clinical payroll by real risk so you're not overpaying on low-risk roles

- High-deductible program structures — Restructuring the policy to capture the spread between the mandated premium and the facility's actual loss outlay

High-Deductible Programs for Qualifying SNF Operators

For larger facilities, a high-deductible structure can be the single biggest lever. The employer takes on a defined first layer of loss — for example, the first $200,000 of a $500,000 program — while the carrier covers everything above it. That trade can roughly halve the annual premium (say, from $100,000 down to around $50,000). Retained claims are then paid the way real claims actually run: monthly — on the order of $3,000 a month — and the payments stop when the condition resolves, rather than being pre-funded to a carrier as a lump sum.

The catch: this only works when the program is actively administered — every retained claim managed, reserved accurately, and closed — and it is coordinated with how WCIRB actually calculates the California mod, which differs meaningfully from NCCI states. It also isn't for everyone: not every business qualifies, and the sweet spot is operators with roughly 100+ employees and $100,000+ in annual workers' comp spend. Multi-location owners — several nursing homes under one entity — can often consolidate into a single master policy for better terms. Learn more about large-deductible workers' comp and how a managing risk / retro program is structured.

One more thing worth saying plainly: our brokerage is paid by commission from the insurer, not from your claims. We don't make more when your claims run higher — which is exactly why we're built to drive them down. Individual results vary.

The Concrete Next Step

To quote your facility or take over an existing program, we need two things: a copy of your current workers' comp policy and five years of loss runs. That's enough to show you where your class codes, reserves, and mod are costing you money you don't need to spend. Send those over and we'll return a clear read within 24 hours.

Frequently Asked Questions

Is workers' compensation insurance mandatory for California nursing homes?

Yes. Labor Code Section 3700 requires every employer with at least one employee to carry coverage. Narrow exemptions exist for certain sole proprietors, but nursing homes of any size must be covered — and going without it is a criminal misdemeanor.

Are all nursing home workers covered by workers' comp in California?

Yes. Every employee — CNA, LVN, RN, dietary, housekeeping, or administrative, full-time or per-diem — is covered from their first day, regardless of fault or hours worked.

A serious injury was reserved at $250,000 — will it really cost that much?

Usually not. Reserve figures and "lawyer numbers" are often far higher than actual medical spend, which on many claims lands closer to ~$30,000 and is paid incrementally — often around $1,500–$2,000 a month — rather than as a lump sum. A broker managing the claim directly works that number down to what the injury actually costs. Individual results vary.

Can a hernia or back injury from lifting a resident be covered?

Yes. Injuries from a specific incident like a patient transfer, or aggravated by occupational duties, qualify. The key is documenting the incident immediately — ideally with a same-day urgent-care record — since timely recordkeeping is the first line of defense if the claim is later exaggerated or disputed.

How can a nursing home lower its workers' comp premium in California?

The levers that move the number are direct claims handling, fast light-duty return-to-work, correcting inflated reserves, accurate class-code splits between clerical and clinical staff, contesting exaggerated claims, and — for qualifying operators — high-deductible program structures. Remember that once premiums rise after a claim they rarely fully drop back, so how each claim is handled early matters for years.

We want a second opinion on our current program — what do you need?

Just two documents: your current workers' comp policy and five years of loss runs. That lets us review your claims profile, class codes, and mod, and show you where you're overpaying — typically with a response within 24 hours.