The warehousing sector faces roughly 70% annual attrition according to McKinsey research, far above most industries. Meanwhile, BLS data shows warehousing and storage recorded a total recordable incident rate of 4.8 per 100 workers in 2024, more than double the 2.3 rate across all private industry. Put those two facts together and a damaging pattern emerges: a workforce that constantly cycles new, untrained people into one of the most injury-prone environments in the country.

Here's the part the carrier won't volunteer. The financial damage isn't just more injuries in a given year. It's that most of those claims get paid at or near face value, with nobody actively working to bring the real cost down — and every one of those payouts follows you through your Experience Modification Rate for years. At PCI Consultants, we've spent 30+ years doing the opposite: handling the claim directly, containing the real cost, and keeping turnover-driven frequency from compounding into a permanent premium problem.

This article unpacks that cycle: why warehouse turnover is structurally high, how it feeds claim frequency, what that does to your EMR, and what specific insurance structures and hands-on claims practices contain the cost even when turnover can't be eliminated.

Key Takeaways

- New hires are the highest-risk segment of any workforce, and high turnover keeps that group perpetually stocked

- A single high-turnover period can inflate your EMR for three or more renewal cycles — and once premiums rise, they rarely come back down

- Left alone, insurers tend to pay turnover-driven claims at face value; a broker who handles the claim directly can cut the real cost dramatically

- Payroll volatility from constant staff changes creates real audit and misclassification exposure

- High-deductible and pay-as-you-go structures fit fluctuating-headcount operations better than standard annual-audit policies, for qualifying businesses

Why Warehouse and Staffing Turnover Is Unusually High

Warehouse turnover is largely structural. Several features of the work make retention inherently difficult:

- Physical demands that lead to burnout, particularly in high-volume fulfillment centers

- Temp and seasonal placements that are designed to be short-term from the start

- Shift-based scheduling that conflicts with workers' personal and secondary-employment commitments

- Limited advancement pathways, which reduce the incentive to stay when a competitor offers marginally better pay

For staffing agencies, the problem runs deeper. They manage a rotating pool of workers placed across multiple client sites — meaning a worker can leave a specific assignment without triggering a formal termination. Two layers of instability run at once: one at the agency level, one at the client site.

The numbers reflect this. McKinsey reports warehousing attrition at approximately 70%, while the broader transportation, warehousing, and utilities sector posts a 4.0% monthly separation rate versus 3.6% for all private industries per BLS JOLTS data — and NAICS 493 warehousing runs even hotter than that.

The consequence for workers' comp is direct. A workforce with 70% annual turnover is perpetually composed, in large part, of people in their first weeks on the job — and new hires file injury claims at far higher rates than experienced employees.

How Turnover Directly Increases Injury Rates and Claims

The New Worker Vulnerability Window

Peer-reviewed research published in Occupational and Environmental Medicine found that workers in their first month on a job are over four times more likely to file a lost-time claim than workers with more than a year of tenure. That's not a marginal difference — it's a structural exposure that compounds with every new hire.

In a high-turnover warehouse, a large share of the workforce sits inside that first-month window at any given moment. High turnover doesn't affect one cohort; it continuously resets the injury clock across the entire operation.

What Happens the Day an Injury Occurs

This is where most employers lose money without realizing it — and where handling the claim directly changes the outcome. When a new hire strains a back lifting a pallet, the default path is that the insurer opens a file, sets a reserve, and starts paying. Nobody is on the phone within the hour deciding what actually happened.

We run it differently. With PCI Consultants, you call us, not the carrier. We evaluate the incident immediately and, when it's warranted, send the injured worker to urgent care the same day. That does two things: it gets a legitimately hurt person real care fast, and it creates an accurate, timely medical record. That record is your protection against a soft-tissue tweak getting inflated into a career-ending injury three months later once an attorney is involved.

Genuine injuries get paid without a fight — that's the job. But an exaggerated or fraudulent claim gets investigated and contested rather than rubber-stamped, which protects your loss history and, by extension, every future renewal. Learn more about our approach to claims management and fraud investigation.

The Injury Types That Drive Costs

Warehouse injuries aren't typically minor. OSHA identifies the dominant categories in warehousing as:

- Musculoskeletal disorders from overexertion in lifting and lowering

- Struck-by incidents involving forklifts and powered industrial trucks

- Slips, trips, and falls, including from loading docks

- Repetitive motion injuries, particularly in e-commerce fulfillment

These frequently become lost-time claims with extended recovery timelines. Warehousing starts from an injury baseline more than twice the private-industry average, which is exactly why active management of each claim matters more here than in a clerical operation.

The Reserve Number vs. the Real Number

Here's a distinction that costs employers hundreds of thousands of dollars: the number on a claim file is not the real cost of the claim. Once an attorney is attached, you'll see a figure like $250,000 — the "lawyer number." The actual medical spend on that same injury is often closer to $30,000, and even that isn't paid as a lump sum. It's paid incrementally, frequently in the range of $1,500 to $2,000 a month, as treatment actually happens.

Left to run on autopilot, an insurer will often reserve at or near the inflated figure and call paying it a "win." When we handle the claim, we work it down to the real number and make sure it's paid the way real medical costs are actually incurred — over time, and only for as long as the condition genuinely requires. Patterns vary case to case, but the difference between the reserve number and the real number is where most of the savings live.

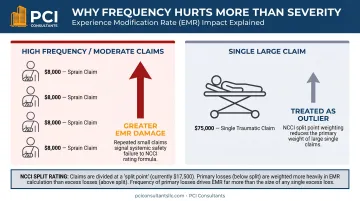

Why Frequency Matters More Than Severity

Many operators focus on the rare huge claim. That misses the bigger insurance risk. A pattern of frequent small-to-medium claims — sprains, minor falls, soft-tissue injuries — signals systemic problems to underwriters and carries heavy weight in EMR calculations. In the formula, claim count and recency both push the modifier up, so a steady stream of $8,000 sprains can do more damage to your renewal than a single large outlier.

The EMR Cycle: How Turnover-Driven Claims Compound Into Higher Premiums

What EMR Actually Is

Your Experience Modification Rate is a multiplier applied to your base premium. An EMR of 1.0 means you pay the industry average. 1.25 means you pay 25% above it. 0.85 means 15% below.

IRMI defines the experience modifier as a factor comparing your actual past loss experience to what's expected for your industry class. Our experience-rating specialists work this number as an input you can influence, not a verdict you have to accept.

The Three-Year Trap and Premium Stickiness

EMR isn't calculated on this year's claims. It's built from several years of historical loss data, with the most recent policy year typically excluded. Under standard rating methodology, a bad loss year follows you for three or more renewal cycles before it ages off.

Worse, there's a stickiness problem the carrier won't emphasize: once your premium rises after a bad claim year, it rarely comes all the way back down, even after the claims resolve and your loss runs clean up. That's why containing the real cost of each claim as it happens beats trying to repair a damaged mod after the fact. For turnover-driven operations, that timing is brutal — an elevated-turnover period keeps inflating renewals long after the workforce situation improves.

How Frequency Penalizes You Doubly

NCCI's experience rating uses a split rating approach: primary losses (below the split point) receive greater weight because they reflect accident frequency, while excess losses receive less. Many small-to-moderate claims — the exact profile chronic turnover generates — can damage your EMR more than their raw dollar amount suggests. Even a shift from 1.0 to 1.2 adds tens of thousands to a $200,000-plus annual policy.

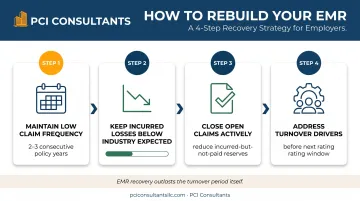

Recovery Is Slow — So Get Ahead of It

Once an EMR is elevated, bringing it down requires sustained clean loss history across multiple policy years:

- Maintaining low claim frequency for two to three consecutive policy years

- Keeping incurred losses well below your industry expected losses

- Actively closing open claims to reduce incurred-but-not-paid reserves

- Addressing turnover drivers before the next rating window opens

The fastest lever here is actually closing claims fast and low — which is a claims-handling job, not an accounting one. Getting an injured worker back on light duty in weeks instead of months, and paying only the real medical cost, keeps incurred losses down while the file is still open. That's work an advocate does; it isn't work the insurer does for free.

Return to Work: The Cheapest Way to Shrink a Claim

Every week a warehouse worker sits at home on total disability, the claim's incurred cost climbs and your EMR exposure grows. The single most effective lever we pull is a fast, structured return-to-work program.

The principle transfers cleanly from healthcare, where we do this constantly: an injured nurse who can't lift patients can often work a receptionist-type role within weeks. In a warehouse, a picker with a lifting restriction can run inventory scans, staff a returns desk, or handle light kitting. Getting someone onto modified duty within weeks — rather than leaving them home indefinitely — sharply cuts the real claim cost and shortens the file's life. It also keeps a marginal, recoverable injury from drifting into the exaggerated, attorney-driven territory that produces those inflated reserve numbers. Individual results vary, but the pattern is consistent.

Payroll Complexity and Audit Exposure in High-Turnover Operations

Workers' comp premiums are calculated on payroll, so the constant movement of employees in and out of a warehouse creates real financial risk beyond claim costs.

Risk Classification and Misclassification

Different job functions carry different class codes and manual rates, and in a high-turnover operation classification errors are common:

- Clerical and administrative staff absorbed into higher-rated warehouse class codes

- Supervisory employees not split out from floor-worker codes

- Drivers dropped into warehouse codes instead of the correct driver classification

This cuts both ways. Getting it wrong overcharges you; getting it right saves money. We segment your workforce by actual risk — clerical and low-risk roles priced separately from high-risk hands-on labor — so you're not paying forklift-operator rates on your front-office staff. On a 100-plus-employee operation, those corrections add up to four-to-six-figure annual differences that then compound through the EMR multiplier.

The Audit Surprise Problem

Standard policies are based on estimated payroll at inception, with a year-end audit to reconcile. For high-turnover warehouses with fluctuating headcount, this creates cash-flow risk: a warehouse that budgets for 80 employees but averages 110 through peak season can face a five-figure audit bill due at renewal.

Pay-as-you-go structures close that gap by calculating premium against actual payroll each pay period, so there's no year-end surprise. For operators with multiple facilities under one owner — several distribution sites, for example — we can often consolidate coverage into a single master policy for better terms and cleaner administration. We'll also grow a smaller or newer operation into stronger structures over time as its loss history earns them.

Practical Strategies to Manage Costs Despite High Turnover

You may not be able to eliminate turnover. You can manage its insurance consequences.

Prioritize the First-Week Safety Intervention

Injury risk peaks in the first days on a new assignment. A brief, standardized, site-specific orientation — facility layout, equipment hazards, lifting mechanics, emergency procedures — cuts first-month injury rates without meaningful overhead. It needs to be consistent and documented every time. Pair it with our loss-control work and the documentation doubles as underwriting evidence.

Track Claims by Site, Role, and Tenure

Identify whether claims cluster at specific client locations, in specific job functions, or among workers in their first 30/60/90 days. That turns a reactive claims history into an actionable risk map — and it's exactly the data we use when we handle a claim to decide fast whether it's legitimate or inflated.

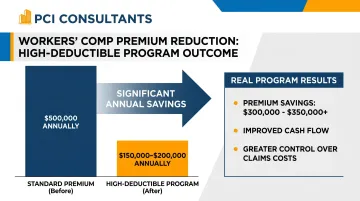

Explore High-Deductible Workers' Comp Programs

For operators with sufficient scale, high-deductible programs can produce substantial premium reductions. The employer retains a defined first layer of risk — say the first $200,000 of a $500,000 program — while the insurer covers the rest. Because the carrier's exposure drops, so does the underwriting premium: an employer paying $100,000 a year can often move to roughly $50,000. Retained claims are paid incrementally as they age (frequently in the range of $3,000 a month) and stop when the condition resolves — not fronted as a giant escrow.

The catch, and the insurance company won't lead with this: these programs only work when someone is actively administering the claims to keep that retained layer small. That's the piece we own. And not every business qualifies — it depends on your scale, loss history, and cash-flow profile, which is exactly what your policy and loss runs let us assess.

Build a Documentation Trail

A documented risk narrative gives underwriters something concrete at renewal:

- Written safety orientation logs for every new hire

- Incident and near-miss reports

- Corrective-action documentation

- Training records tied to specific roles and dates

The goal is to show that high turnover is a structural feature of the industry, not a sign of mismanagement. Underwriters respond to that distinction when operational evidence backs it up.

One More Thing on Incentives

A fair question: if a broker is this hands-on with claims, what's in it for them? We're paid by commission from the insurer, not out of your claim payments — so we're not incentivized by your claims volume. When we work a claim down to its real cost, that's aligned with you, not against you.

The Concrete Next Step

If turnover is driving your warehouse or staffing comp costs, the fastest way to know what's fixable is a review of your actual numbers. Send us two things: a copy of your current workers' comp policy and your five-year loss runs. That lets us see your class codes, your open claims, your EMR trajectory, and whether a high-deductible or pay-as-you-go structure fits — and quote or take over coverage from there. It's a no-cost consultation to start.

Frequently Asked Questions

What are the effects of high staff turnover on workers' comp?

High turnover increases injury frequency among inexperienced new hires, worsens your EMR over time, and drives up recruitment and training costs. The financial damage compounds across multiple renewal cycles — and because premiums rarely fall all the way back down once they rise, a single bad turnover year can cost you for years. It's both a safety issue and a direct financial liability.

What is an acceptable staff turnover rate in warehousing?

The sector sees roughly 70% annual attrition according to McKinsey, well above most industries. There's no universal "acceptable" benchmark, but keeping turnover below your peer group measurably improves safety outcomes and, over time, your claim history and EMR. What matters more than the raw number is how each resulting claim is handled.

Why does my insurer pay claims at full value instead of fighting them?

Without an advocate, insurers tend to pay a claim at or near its face value and call it a win — it's the path of least resistance for them. That's the default we exist to change. We handle the claim directly: legitimate injuries get paid without dispute, but exaggerated or fraudulent ones get investigated and contested, and every claim gets worked down toward its real cost rather than its inflated reserve figure. Individual results vary.

What's the difference between the claim reserve and the real claim cost?

A lot. Once an attorney is involved you'll often see a figure like $250,000 on the file — the "lawyer number." The actual medical spend is frequently closer to $30,000, and it's paid incrementally (often $1,500 to $2,000 a month) as treatment happens, not as a lump sum. A broker actively handling the claim works it toward the real number instead of accepting the inflated one.

How can a warehouse operator lower workers' comp premiums when turnover can't be eliminated?

Focus on consistent new-hire orientations, claim tracking by site and tenure, fast return-to-work, and active claims handling that contains real cost. On the structure side, correct risk classification, and explore high-deductible or pay-as-you-go coverage designed for fluctuating workforces. Not every business qualifies for every structure, but most high-turnover operations have room to lower their costs.

What type of workers' comp coverage works best for high-turnover warehouses?

Pay-as-you-go policies align premiums with actual payroll in real time, eliminating audit surprises. High-deductible programs can significantly reduce the carrier-charged premium for operations with effective internal risk management — but only when the retained-claims layer is actively administered, and not every business qualifies. Both generally fit high-turnover warehouses better than standard guaranteed-cost policies. The right answer depends on your scale and loss history, which is why we start from your policy and five-year loss runs.