6 Ways to Get a Real Reduction of Premium on Workers' Comp

For most employers, a workers' compensation premium arrives like a utility bill: a fixed number you have no choice but to pay. That is the story the insurance company is happy to let you believe. It isn't true.

Your premium is not a flat fee. It is the output of a calculation built on your risk profile and, more than anything else, on how your claims get handled once someone gets hurt. Change how the risk and the claims are managed, and the number changes with it.

This is written for mid and large employers, especially in healthcare, where a nursing home, home-health agency, or hospital can be carrying six figures of annual workers' comp spend. Below are the six levers that produce a genuine reduction of premium, and the one nobody at your carrier is going to point out.

Key Takeaways for a Lower Premium

- A reduction of premium comes from lowering the true cost of your claims, not just re-shopping rates.

- Classify your workforce by real risk so clerical staff aren't rated like hands-on caregivers.

- A high-deductible program can roughly halve annual premium for qualifying businesses.

- How a claim is handled in the first 48 hours drives its final cost more than anything else.

Why Workers' Comp Premiums Get So High

A premium is the insurer's prediction of how often your people will get hurt and how much those injuries will cost. In healthcare that prediction runs high for a reason: lifting and transferring patients, needlesticks, slips, and repetitive strain make caregiving one of the highest-injury occupations there is. But the number that shows up on your renewal is driven by a handful of specific factors.

The Core Drivers Behind Your Premium

- Job classification sets the baseline. A registered nurse on the floor and a billing clerk down the hall carry very different rates. If your whole staff is lumped into one high-risk code, you are overpaying on every low-risk role.

- Your claims history, expressed through the Experience Modification Rate (EMR), multiplies that baseline. An EMR under 1.0 is a discount; over 1.0 is a surcharge that follows you.

- Payroll is the exposure base. More payroll means more potential injuries in the insurer's model, which is exactly why misclassified payroll quietly inflates your bill.

- Deductible structure shifts risk. Agreeing to absorb a defined first layer of loss lowers the premium because you are taking on more of the early cost yourself.

- Geography and state rules move rates up or down. The median workers' comp rate is about $1.09 per $100 of payroll, but it can climb to $2.33 in states like New Jersey.

Here is the part the insurance company won't tell you: the single biggest driver of what you pay next year is what your claims actually cost this year. And left to run on autopilot, claims almost always cost more than they should.

The 6 Strategies That Actually Lower Your Premium

There is no single magic move. A real reduction of premium comes from stacking smart policy structure on top of disciplined risk and claims management.

Policy Structure and Program Design

1. Use a Higher, Strategic Deductible

A deductible is the portion of each claim you agree to cover before the insurer pays. By choosing a higher deductible, you tell the carrier you'll absorb the small, predictable losses yourself, and the premium drops in exchange.

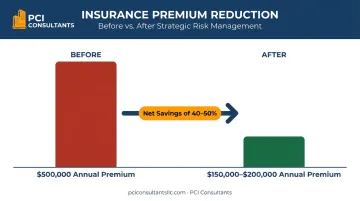

For employers with steady cash flow and a decent loss history, this can go much further through a high-deductible program, where you take a defined first layer of risk (say the first $200,000 of a $500,000 program) and the insurer covers the rest. For qualifying businesses this can roughly halve the annual premium, cutting a $100,000 bill toward $50,000. Not every business qualifies, and the layer has to be administered actively, not just signed. Claim payments inside that layer are structured monthly, around $3,000 a month, and they stop when the condition resolves, so you are never fronting a lump sum. You can read more on how these large-deductible programs work.

2. Classify Your Workforce by Real Risk

This is where healthcare employers leak money quietly for years. A facility that codes its receptionists, schedulers, and billing staff at the same rate as its floor nurses is paying a hands-on-injury rate on people who never leave a desk. Segmenting the workforce by actual risk, clerical versus high-risk direct-care roles, can meaningfully lower the premium without changing a thing about your operation. An honest classification review is often the fastest reduction of premium available, and it is also the first thing a real audit catches.

Proactive Risk Management

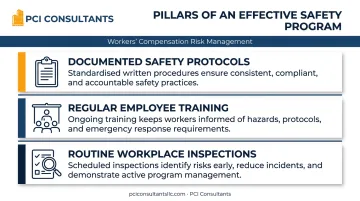

3. Build a Documented Safety Program

Insurers reward employers who stop claims before they start. In a nursing home or home-health setting that means safe patient-handling and lift protocols, sharps and infection-control procedures, and slip-and-fall prevention, all written down and actually trained.

Key components of a working program:

- Documented protocols for every high-risk task, from patient transfers to medication handling.

- Regular training on lifting mechanics, equipment use, and incident response.

- Routine inspections that find hazards before they injure someone.

The return is well documented. OSHA estimates that for every $1 invested in safety and health programs, employers see a return of $4 to $6. A formal workplace safety program is the long game that steadily pulls your EMR down.

4. Manage Claims Actively, From the First Hour

This is the lever that moves the number the most, and the one most employers hand straight to the insurer. Here is what the insurance company won't tell you: left alone, an insurer tends to pay a claim at or near its face value and call that a win. There is no one on the carrier's side whose job is to make the claim cost less.

We do the opposite. When someone is hurt, the call comes to us, not the insurer, and it comes right away. We evaluate the incident immediately and, when it's warranted, send the injured worker to urgent care that same day. That day-one medical record is what protects you later, because it pins down what actually happened before a claim can drift or get exaggerated weeks down the line.

That groundwork is what lets us correct the "lawyer number." A claim gets presented as $250,000; the real medical spend behind it is closer to $30,000, and it gets paid incrementally, roughly $1,500 to $2,000 a month, not as a lump sum. Legitimate injuries get paid without a fight, every time. Exaggerated or fraudulent ones get investigated and contested so a single bad claim doesn't wreck your loss history and your premium for years. This is the heart of good claims management, and individual results vary.

5. Return People to Work on Light Duty

The longer a claim stays open, the more it costs, and the more it inflates next year's premium. A structured return-to-work program shortens that clock. An injured nurse who can't yet handle floor duty can often move into a receptionist-type or scheduling role within weeks, keeping a skilled employee on payroll and sharply cutting the real cost of the claim. It is better for the worker and cheaper for you at the same time.

Strategic Review and Partnership

6. Audit the Policy Every Year and Partner With a Specialist

Never let a workers' comp policy auto-renew. Businesses change, headcounts shift, roles get reclassified, and stale payroll estimates cost real money. An annual audit confirms your payroll figures, checks that every role carries the correct class code, and catches the overpayment where a desk job is riding a caregiving rate.

The deeper point is who runs that review. A broker who only places the policy and disappears is not the same as a partner who manages your total cost of risk. A specialist brings risk modeling, direct claims oversight, and access to programs that never surface on the open market, and, importantly, is paid by commission from the insurer rather than by how many claims you file. That means the incentive is to shrink your claims, not process them.

How PCI Consultants Drives Your Reduction of Premium

Putting all six levers into practice takes dedicated people, and that is exactly what we are. PCI Consultants brings over 30 years of experience cutting workers' compensation losses and premiums, and we manage the claim directly for the life of the policy. When an incident happens, your team calls us, not a carrier's 1-800 line.

Our in-house risk and claims managers use custom software to monitor every open claim, flag possible fraud, and push each one toward the lowest honest cost, faster and more accurately than an overloaded carrier ever will. For multi-location owners, several facilities under one owner can often be consolidated into a single master policy for better terms, and smaller or newer operations can be grown into stronger programs over time.

For qualifying businesses, a well-run high-deductible program can move a $500,000 annual cost down toward the $150,000 to $200,000 range, with net savings that can land in the 40 to 50 percent range even after claims are paid. And because premiums are sticky, once a claim pushes your rate up it rarely comes all the way back down, the money saved by keeping claims small compounds year after year. Individual results vary.

From Unavoidable Cost to Managed Variable

A workers' comp premium feels fixed only when nobody is actively working to lower it. Treat it as a variable, tied to how well your risk is classified and how tightly your claims are managed, and you take back control of one of your largest operating costs.

The concrete next step is simple. Send us a copy of your current workers' comp policy and your five-year loss runs. We'll review your classifications, your claims, and your program structure, and show you exactly where a real reduction of premium is sitting.

Frequently Asked Questions

What is a reduction of premium?

It is a genuine decrease in what you pay for coverage. On workers' comp, the durable way to get there isn't re-shopping the same risk, it's lowering the true cost of your claims, correcting your job classifications, and structuring the deductible to fit your actual risk tolerance.

Can you really get a workers' comp premium lowered?

Yes, and usually by more than employers expect. The biggest wins come from managing claims actively so an inflated claim gets corrected to its real cost, returning injured staff to light duty quickly, and, for qualifying businesses, moving into a high-deductible program. Individual results vary.

How does a higher deductible lower my premium?

By agreeing to absorb the first layer of each loss, you take on more of the early risk, so the insurer charges less up front. In a high-deductible program that first layer is paid out monthly as claims resolve, not as a lump sum, which protects your cash flow. Not every business qualifies.

What is an Experience Modification Rate (EMR) and why does it matter?

Your EMR compares your claims history to your industry's average and multiplies your premium directly, below 1.0 is a discount, above 1.0 a surcharge. Because premiums are sticky, a single inflated claim can raise your EMR and keep your cost high for years, which is why controlling each claim's real cost matters so much.

Why does handling the claim directly lower my cost?

Left alone, an insurer tends to pay a claim at or near face value and move on, there's no one on their side trying to make it cost less. When we take the call first, evaluate the incident immediately, document it at urgent care on day one, and pay only the real cost incrementally, the claim resolves smaller, and your loss history and future premium stay protected.

How often should I review my workers' comp policy?

At least once a year at renewal, and again after any real change in payroll, headcount, or services. A copy of your current policy plus five years of loss runs is all we need to spot misclassifications and missed savings before you re-sign.