The structural reality of staffing — dozens of class codes, workers rotating across client sites, payroll that can swing 40% inside one policy term — means audit surprises hit harder here than almost anywhere else. According to the American Staffing Association, about 11 million people work for US staffing firms in a given year, and every payroll dollar is a class-code decision waiting to be second-guessed by an auditor.

Here's the part the insurance company won't volunteer: without an advocate in the room, an auditor's job is to resolve every ambiguity in the carrier's favor and move on. At PCI Consultants we've spent 30+ years doing the opposite — showing up to the audit for the agency, challenging the assumptions before they're baked into the number, and disputing the final statement when it's wrong. This article covers what the audit actually examines, where staffing firms consistently get burned, and what a year-round posture looks like when someone is actually managing it for you.

Key Takeaways

- Workers' comp audits are mandatory at policy year-end and reset your future premium, not just last year's bill

- Staffing agencies face heavier scrutiny because of multi-site placements and frequent class-code changes

- The most common audit failures are worker misclassification, underreported payroll, and missing or expired subcontractor COIs

- Non-cooperation triggers an audit noncompliance charge of up to two times estimated annual premium

- An inflated audit figure raises your experience mod — and that increase rarely comes back down even after the number is corrected

What a Workers' Comp Audit Actually Determines

A workers' comp audit is a formal review by the carrier or a third-party auditor, usually opened about 30 days after the policy term ends. It reconciles the estimated payroll used to set your original premium against actual payroll and operational data for the coverage period.

Two outcomes are possible: you owe additional premium, or you're owed a credit. Left to run on its own, most staffing agencies land in the first bucket — not because they did anything wrong, but because nobody was managing the documentation trail the auditor grades against.

Why the Audit Result Compounds Over Time

The audit doesn't just close last year's books. Per WCIRB California, audited payroll is reported to rating bureaus and used to calculate experience modifications — estimated or unaudited payroll is explicitly prohibited in that math.

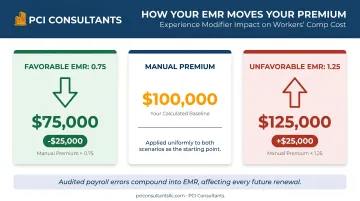

Your experience modifier (EMR) compares your loss history to industry averages and directly scales your manual premium. An NCCI example makes it concrete: a 0.75 mod drops a $100,000 manual premium to $75,000; a 1.25 mod raises it to $125,000. Source: NCCI ABCs of Experience Rating.

This is the mechanism most agencies underestimate. When an audit surfaces underpaid premium from misclassification or unreported payroll, those corrected figures feed the EMR at renewal. And premium is sticky in the worst way: once a claim-driven or audit-driven increase lands in your mod, it rarely comes back down even after the underlying issue is resolved. You don't pay for a bad audit once — you pay for it across the three-year rating window. That's why the loss history feeding the audit matters as much as the audit itself, and why we manage claims directly to keep that history clean rather than waiting for renewal to react.

Audit Formats

Auditors pick the format based on account size, policy complexity, and carrier discretion:

- In-person / on-site — most common for larger or higher-risk staffing accounts

- Virtual / video — increasingly standard post-pandemic

- Mail-in / self-report — used for smaller, simpler policies

Non-cooperation is not a strategy. Under NCCI Item B-1429, carriers can apply an Audit Noncompliance Charge of up to two times estimated annual premium where approved — layered on top of whatever worst-case figures they invent without your input.

Why Staffing Agencies Face Unique Audit Challenges

Most employers have one work environment and a handful of class codes. Staffing agencies have neither, and the audit rules are written in a way that punishes ambiguity.

The Class Code Problem

Every placement can require a distinct classification code based on the client worksite and the actual duties performed — not the worker's title. One policy can carry dozens of codes at wildly different rates. Two rules make this brutal for staffing:

- NCRB Rule 2: If payroll records don't show actual amounts by classification for each employee, the entire payroll for that employee is assigned to the highest-rated classification representing any part of the work. Sloppy documentation doesn't get you a middle-ground result — it gets you the worst case.

- NYCIRB Rule IV: Workers placed at a client site are classified as if they were that client's direct employees, not the agency's. Agencies that code placements around their own back-office operations are building an audit liability from day one.

There's an upside hiding in this same rule set, though. Because classification follows actual risk, a properly segmented payroll means your clerical and administrative staff aren't rated as if they're on a warehouse floor. Getting your workforce split correctly by real risk — low-risk desk roles separated from high-risk hands-on placements — is one of the fastest ways to stop overpaying. It's the same risk classification discipline we apply when we take over a policy.

Payroll Volatility

Temp and contract payroll fluctuates more than almost any other industry. Estimated payroll at inception routinely diverges from year-end actuals, which makes large audit adjustments structurally predictable rather than occasional.

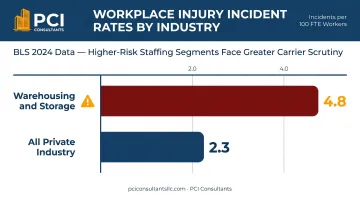

Agencies in higher-risk segments — CDPAP, home health, traveling-nurse and healthcare staffing, light industrial — draw heavier carrier scrutiny because injury frequency runs higher there. BLS 2024 data puts warehousing and storage at 4.8 incidents per 100 full-time workers versus 2.3 for all private industry, and healthcare support roles carry some of the highest musculoskeletal-injury rates of any occupation.

What This Means Operationally

PCI Consultants works with staffing agencies across these verticals, and at initial engagement we almost always find the same structural leaks:

- Clerical staff payroll swept into higher-rated field or production codes

- Subcontractor payroll wrongly attributed to the agency (the sub carried their own coverage)

- Overtime premium not capped to straight-time equivalent as most states require

- Tips, bonuses, and per diems improperly folded into the payroll base

- Multi-state operations not split by state rating-bureau rules

Each error looks minor alone. Stacked together, they routinely produce four-to-six-figure overcharges on policies above $100,000 annually — money that walks out the door quietly because no one is reviewing the auditor's math.

The Three-Stage Audit Process — and Where to Intervene

Understanding what happens at each stage is the foundation of any real audit posture. Here's where an advocate changes the outcome.

Stage 1: Documentation Request

The auditor asks for:

- Payroll records segmented by employee, client name and location, class code, and gross earnings

- Federal 941s and state quarterly returns for the full policy period

- Executive officer and owner compensation details

- Subcontractor records including names, amounts paid, duties, and certificates of insurance

The subcontractor COI requirement blindsides agencies constantly. If you can't produce a valid COI for a subcontractor or 1099 worker, that individual's earnings can be added to your auditable payroll at the highest applicable code. It's one of the most consistently costly oversights in the industry — and one of the easiest to prevent when someone owns the checklist year-round.

Stage 2: Classification and Payroll Review

The auditor cross-references your payroll against tax filings and verifies each placement's governing class code. Any discrepancy — a light-industrial worker coded as clerical, a supervisor not split from a field code — gets reclassified at the higher rate for the entire period that worker was active.

This is where having someone in the room for you matters most. Left alone, an auditor resolves every gray area in the carrier's favor and calls the inflated figure a win. Our audit defense model puts us at this review directly, challenging misclassifications in real time before they harden into the final calculation. Without that presence, auditors issue trueup invoices built on their own assumptions — and most agencies pay them without a second look. Our claims and payroll review work is built precisely for this stage.

Stage 3: Final Statement and Premium Adjustment

Once the review closes, the auditor issues a final statement with the premium adjustment. If you owe more, the insurer typically demands payment immediately or within 30 days.

For agencies growing headcount fast, this is where cash flow takes the hit. A $300,000 policy that grew headcount 40% mid-term can generate a $50,000–$100,000 trueup if codes and payroll weren't tracked in real time. And audit statements contain errors more often than agencies realize. When they do, a formal dispute and revision can recover the overcharge — but only if someone catches it and files it. That post-audit dispute is the third leg of how we work.

The Loss History Behind the Audit: Where Claims Handling Comes In

Audits grade your payroll, but your experience mod grades your claims. You can run a flawless payroll audit and still get hammered at renewal if a handful of open claims are sitting on your loss runs at inflated reserves. This is the piece a standard carrier relationship leaves entirely to chance — and where active management earns its keep.

The "Lawyer Number" Versus the Real Number

When a worker is injured on a client site, the first figure that surfaces — often a demand-driven "$250,000 claim" — is almost never the real cost. The actual medical spend on many of these injuries lands closer to $30,000, paid incrementally at roughly $1,500–$2,000 a month, not as a lump sum. The gap between the headline number and reality is exactly what quietly inflates your reserves, your mod, and next year's audited premium if nobody is managing it down.

We handle the claim directly for the life of the policy — the injured worker and the agency call us, not the insurer. When an incident happens, we evaluate it immediately and, where appropriate, send the worker to urgent care right away so there's an accurate, timely medical record. That record is what protects the agency later against exaggeration, because the facts were documented on day one instead of reconstructed by a plaintiff's attorney months later.

Fast Return to Work and Fraud Screening

Getting people back to work is the single biggest lever on real claim cost. A light-duty return-to-work transition — an injured nurse moved into a receptionist-type role for a few weeks — sharply cuts the loss that lands on your record. Legitimate injuries get paid without a fight; that's not in question. But exaggerated or fraudulent claims get investigated and contested rather than rubber-stamped, which protects both your loss history and the premiums that history drives. One note that matters given the compliance line above: we describe typical patterns here, not promised results — individual results vary.

And because we're paid by commission from the insurer rather than by your claims volume, we're not incentivized to let a claim ride. Our interest is in keeping your loss runs — and therefore your audit — as clean as possible.

Common Mistakes That Lead to Audit Penalties

Misclassification

The most financially damaging error. Using an approximate or generic code instead of the governing code for the actual client worksite produces retroactive reclassification at the higher rate for all affected payroll across the entire policy period. When records are ambiguous, auditors apply the highest defensible code — that's not a negotiating posture, it's the rule.

Agencies juggling dozens of client accounts with evolving duties and rotating workers are especially exposed. A placement that started clerical and shifted to warehouse work mid-assignment without a code update creates an audit liability for every dollar that worker earned after the role changed.

Overtime Miscalculation

Under NCCI Rule 2, only the overtime premium portion — the extra pay above straight-time equivalent — is excluded from workers' comp payroll. The straight-time equivalent stays in. And the exclusion only applies when records separately document overtime pay by employee and by classification summary. Agencies that blend regular and overtime wages without segmentation lose the exclusion entirely, and the auditor includes the full gross.

Ignoring or Delaying the Audit Response

Carriers can and do proceed without your input under a non-cooperative designation, applying worst-case estimates and stacking the noncompliance charge on top. In a hardening staffing market, that audit statement can trigger non-renewal and cut off your voluntary-market access.

Agencies pushed out of the standard market usually land in assigned risk pools. NCCI's 2024 residual market data shows average assigned-risk premiums at $3,672 per policy, with an ARAP surcharge applied where loss records exceed expectations — a cost spiral that takes years to climb out of. For larger agencies, a better-structured program is often the way back; see alternatives to standard workers' comp.

How to Stay Audit-Ready Year-Round

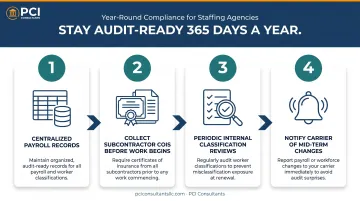

Scrambling to assemble documentation 30 days after a policy expires is the most expensive way to run this process. The alternative is a year-round discipline built on four habits:

- Keep a centralized payroll record listing each employee's name, client name and location, class code, and gross earnings — updated in real time as placements change, not reconstructed from memory at audit time.

- Collect COIs from every subcontractor before work begins — missing certificates are the fastest route to payroll being added to your base at the highest code.

- Run periodic internal classification reviews to catch placements where the assigned code no longer matches the actual work.

- Notify your carrier or program manager when you add client accounts, enter new states, or spike headcount — mid-term changes can trigger an endorsement that realigns estimated payroll and shrinks year-end exposure.

Multi-State Complexity

Agencies operating across multiple states face layered audit complexity. Class-code definitions, rate structures, and audit rules vary meaningfully between NCCI states and independent-bureau states like New York (NYCIRB), New Jersey (NJCRIB), Pennsylvania (PCRB), and California (WCIRB). Expanding into a new state without confirming how that bureau treats your placement types is a direct path to misclassification findings.

This is also where scale can work for you rather than against you. An owner running several staffing entities or care locations can often consolidate coverage into a single master policy for better terms and cleaner audits — for qualifying operations, not every structure fits.

High-Deductible Programs and Audit Exposure

For larger, well-run agencies, a high-deductible program changes the audit conversation entirely. The employer takes on a defined first layer of loss — say the first $200K of a $500K program — and the insurer covers the rest, which can roughly halve annual premium (for example, $100K down to $50K). Claim payments are then structured monthly, around $3,000 a month, and stop when the condition resolves — administered actively by the brokerage rather than left to the carrier. It's a powerful lever, but it demands disciplined claims handling and clean records, and it's for qualifying businesses only — not every agency qualifies. When it fits, we manage that first layer directly through our claims management team.

Program Structure Matters

The structure of the program itself drives audit risk. Agencies that partner with specialists maintaining in-house risk monitoring and active claims oversight — rather than relying on a standard carrier's once-a-year look — walk into audit season with cleaner payroll and more defensible class-code documentation. PCI Consultants' payroll audit defense model runs three phases: pre-audit preparation, audit-day direct participation, and post-audit dispute when the statement contains errors. For new staffing clients, the combined class-code reclassification and audit defense engagement is usually the year-one priority.

The Concrete Next Step

If you want to know where you actually stand before your next audit, the fastest path is to send us two documents: a copy of your current workers' comp policy and your five-year loss runs. That's everything we need to review your class codes, spot the payroll and classification exposure an auditor would seize on, and tell you whether a different program structure would lower your real cost. No generic quote — a real look at your setup.

Frequently Asked Questions

How long do workers' comp audits take?

Audits typically open about 30 days after the policy term ends, and the review usually wraps within 60 days. The timeline depends on how fast the agency submits documentation and how complex its payroll and class-code structure is. When we handle it, the prep is done before the auditor asks, which is what keeps the process short and the surprises out of it.

Are workers' comp audits mandatory for staffing agencies?

Yes. Every workers' comp policy is audited at term end, and staffing agencies can't opt out. Skipping participation triggers a non-cooperative audit where the carrier estimates values without your input — almost always higher, plus a noncompliance charge on top.

What are the consequences of failing a workers' compensation audit?

The main outcomes are retroactive premium adjustments, non-cooperative audit fees (up to two times estimated annual premium), possible policy cancellation, and trouble securing future voluntary-market coverage. Each feeds a higher experience mod at renewal — and because mods are sticky, that increase tends to stick around for years even after the issue is fixed.

What documents do staffing agencies need for a workers' comp audit?

Have these five categories ready before the auditor arrives:

- Payroll records broken down by employee, client, class code, and earnings

- Federal 941s and W-2s for the policy period

- Subcontractor details and certificates of insurance

- Executive officer compensation information

- Job descriptions for each classification used

If you're evaluating a new broker, the same two documents that start our review — your current policy and five-year loss runs — also tell us most of what a future audit will hinge on.

How do class codes affect workers' comp audit results for staffing agencies?

Class codes set the premium rate applied to each employee's payroll. Incorrect codes, even assigned in good faith, get reclassified at the correct (usually higher) rate during the audit — meaning additional premium for the entire period that employee was active. The flip side: segmenting your workforce by real risk, so clerical staff aren't rated like field workers, is one of the most reliable ways to stop overpaying.

What triggers a workers' comp audit outside of the annual review?

Mid-term audits can be triggered by significant payroll growth, ownership changes, expansion into new states or industries, or a high frequency of claims — all common events in staffing. That's exactly why proactive communication with the carrier throughout the year matters, and why active claims handling that keeps loss frequency down protects you well before the audit ever opens. Individual results vary.