Here's what most owners get wrong: they treat the rate on their policy as the cost. It isn't. The real cost of workers' comp for a moving company is decided long after the policy is bound — in how each claim is handled, how fast an injured mover gets back to light duty, and whether anyone is actually challenging the inflated numbers your insurer would otherwise pay without a fight. This article covers 2026 rate ranges, how premiums are calculated, which factors drive costs up or down, and the structural moves that meaningfully reduce your annual bill.

Key Takeaways

- Colorado moving companies pay workers' comp based on class codes, payroll size, and experience modification — not a flat rate

- The 2026 advisory loss cost for moving-related codes runs 40 to 70 times higher than clerical ($0.05) and well above warehouse ($1.41) classifications

- A 0.10 EMR shift moves your total premium by 10% of manual premium — and it repeats across three policy years, because premiums that rise after a claim rarely come back down

- Separating clerical, warehouse, and field-mover payroll reduces cost without changing a single operation

- How the claim is handled after an injury — not the rate at binding — is what actually decides your multi-year cost

- Operations paying $100K+ annually may qualify for high-deductible structures; not every business qualifies

How Much Does Workers' Comp Cost for Colorado Moving Companies in 2026?

Workers' comp for a Colorado moving company doesn't follow a single price. It depends on payroll size, workforce composition, and claims history. The most common mistake is budgeting with a flat dollar estimate instead of running a proper per-$100-of-payroll calculation — which is how owners get blindsided at the year-end audit.

Two errors show up constantly:

- Multi-role payroll treated as one rate — movers, drivers, warehouse staff, and office workers all carry different class codes and dramatically different rates

- Experience modifier ignored — a company with a 1.25 EMR is paying 25% more than manual premium, and most owners don't notice until it has already compounded across several renewals

Typical Rate Ranges by Company Size

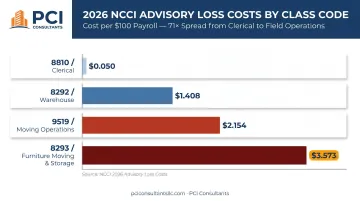

The most accurate starting point is Colorado's 2026 NCCI advisory loss costs, which set the baseline before carrier multipliers are applied:

| Code | Workforce Role | 2026 Advisory Loss Cost per $100 Payroll |

|---|---|---|

| 8810 | Clerical / dispatch | $0.050 |

| 8292 | Warehouse / storage workers | $1.408 |

| 9519 | Moving operations (verify phraseology via NCCI) | $2.154 |

| 8293 | Furniture moving / storage (verify phraseology) | $3.573 |

These are advisory loss costs, not final carrier rates. Carriers apply loss-cost multipliers, schedule credits or debits (up to 25%), and your experience modifier on top.

Small Operations (1–5 Field Employees)

At this scale most companies are on a standard guaranteed-cost policy with no experience modifier yet applied. Premium is driven almost entirely by payroll size and class code assignment, and new companies without prior claims pay base rates. This is also where a single mishandled claim does the most lasting damage: with a thin loss history, one exaggerated back injury can set an EMR that follows you for years. Smaller and newer movers are exactly the operations we grow over time — keeping the loss history clean early is what makes the later terms possible.

Mid-Size Operations (6–20 Employees)

The experience modifier becomes a factor once you've accumulated roughly three years of claims data. At this stage your EMR can meaningfully reduce — or significantly inflate — your base premium, and coverage typically spans multiple class codes. This is the range where active claims management starts paying for itself, because every claim you keep small keeps the modifier down.

Larger Operations (20+ Employees or Multi-Truck Fleets)

At this scale the EMR is mandatory and audits grow more complex due to crew-size variability. Alternative structures — including high-deductible policies — become financially relevant here, and annual premiums can reach $200,000 to $1.5M+ depending on total payroll. Owners running several franchises or locations can often consolidate into a single master policy for better terms, the same way we handle multi-site clients in other high-risk industries.

Key Factors That Affect Colorado Workers' Comp Rates for Moving Companies

Five variables determine what a Colorado moving company actually pays — and four of them are directly within your control.

Employee Classification Codes (NCCI Class Codes)

Every role carries its own NCCI class code with its own base rate, and the spread in moving is extreme: the 8293 advisory loss cost is roughly 71 times higher than the 8810 clerical rate. Misclassifying even part of your office or dispatch staff under a mover code creates a compounding overcharge across every payroll dollar. This is risk classification done right — you shouldn't be paying field-mover rates on people who never touch a dolly.

The most common misclassification errors in moving operations:

- Dispatchers and billing staff assigned to field mover codes instead of 8810

- Working supervisors lumped into the highest-rated field code rather than a separate supervisory classification

- Drivers misclassified under a higher-rated moving code when a dedicated driver code may apply

- Overtime included in full at audit rather than capped to straight-time wages (most states require only the straight-time portion)

NCCI's Class Look-Up tool is the authoritative source for state-specific phraseology. Verify codes 9519 and 8293 there before finalizing classification decisions.

Payroll Size

Colorado premiums are calculated per $100 of payroll, so workforce size directly drives total cost. Common audit triggers for movers:

- Seasonal hires added during peak moving season increase payroll — and audited premium

- Subcontractor crews without their own WC coverage may be treated as employees at audit

- Overtime wages, unless properly capped, inflate the payroll base

Claims History and Experience Modification Rating (EMR)

After a few years, NCCI assigns your company an Experience Modification Rating. An EMR of 1.0 is neutral. Above 1.0 means more claims than industry average; below 1.0 means fewer.

The math is direct:

- 0.75 EMR → $100,000 manual premium becomes $75,000

- 1.25 EMR → $100,000 manual premium becomes $125,000

A 0.10 move shifts your modified premium by 10% — every year, for three years, because NCCI rolls three policy years of loss data into each rating. And here's the part the insurance company won't put in writing: once your premium goes up after a bad claim, it rarely comes back down, even after that claim resolves. That stickiness is exactly why the size of each claim — not just whether you had one — matters so much.

How the Claim Is Handled After an Injury

This is the factor no rate table shows, and it's the one that separates a moving company with a runaway mod from one with a clean loss history. Left to their own devices, insurers tend to pay a claim at or near face value and call it a win — minimizing cost isn't their job, so they don't. A mover reports a strained back, an attorney attaches a $250,000 number to it, and the carrier reserves against that figure. Reserves feed your EMR whether or not the claim ever pays out at that level.

With an advocate handling the claim directly, the story changes. At PCI Consultants the injured worker calls us, not the insurer. We evaluate the incident immediately and, when warranted, send the worker to urgent care the same day — creating an accurate, timely medical record that documents the real injury before it can be exaggerated weeks later. A genuine injury gets paid without dispute. An exaggerated or fraudulent one gets investigated and contested. That same $250,000 "lawyer number" often reflects roughly $30,000 in actual medical spend, paid incrementally at around $1,500 to $2,000 a month — not a lump sum. Right-sizing the reserve is what protects your mod, and therefore your premium, for years. Individual results vary.

Return-to-Work Practices

Moving companies with documented return-to-work programs close claims sooner and cheaper. An injured mover who can't carry furniture can often handle dispatch, inventory, or packing supervision within weeks. In healthcare we do the same thing — an injured nurse moved into a receptionist-type role — and the principle is identical: a light-duty transition cuts the real claim cost sharply and reduces the claim's weight in the NCCI experience formula. A worker sitting at home on total disability is expensive; a worker back on modified duty is not.

Colorado-Specific Regulations and 2026 Rule Updates

Several regulatory changes affect Colorado movers in 2026:

- Rules 1 and 5 amendments, effective July 15, 2026, update general definitions, claims adjusting requirements, and EDI reporting standards tied to the CoComp modernization

- Employer reporting requirement: under Rule 5, employers must report work-related injuries to their insurer within 10 days of notice or knowledge — a window that matters, because a fast, documented report is exactly what a same-day urgent-care record supports

- 2026–2027 Maximum Benefits Order, effective July 1, 2026: sets the maximum compensation benefit rate at $1,464.12 per week

- DOWC surcharges: carriers pay 1.43%; self-insureds pay 1.40%

Higher benefit caps raise the cost of severe claims, which pushes carriers to price manual rates higher even as overall loss costs decline — another reason keeping individual claims small is where the leverage actually is.

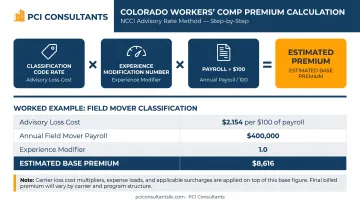

How Workers' Comp Premiums Are Calculated in Colorado

Colorado is an NCCI state. NCCI collects claims data, analyzes trends, and recommends base loss costs to the Colorado Department of Insurance. Carriers then apply their own loss-cost multipliers, schedule credits or debits, and your EMR to reach a final premium.

The standard formula:

Classification Code Rate × Experience Modification Number × (Payroll ÷ $100) = Estimated Premium

Concrete example for a mid-size Colorado mover:

| Input | Value |

|---|---|

| Advisory loss cost (moving operations code) | $2.154 per $100 payroll |

| Annual payroll for field movers | $400,000 |

| Experience modifier | 1.0 (neutral) |

| Estimated base premium | $8,616 |

That $8,616 is a starting point. Add carrier multipliers, schedule rating, and the DOWC surcharge, and your actual invoice lands above it — often materially so. And notice what the formula doesn't contain: any variable for how well your claims are managed. Two identical movers with the same payroll and the same codes can pay wildly different premiums three years out, purely because of what happened to the EMR term after one back injury was handled well and the other was left to run.

Annual payroll audits are where Colorado movers get caught off guard. Premium is set at inception on estimated payroll, then reconciled against actuals at year-end. If your crew grew mid-year, you brought on seasonal workers, or you used subcontractors, the audited premium can run well above your estimate. Moving companies face this audit exposure more than most, given the seasonal swings and variable crew sizes that define the business.

How to Reduce Your Moving Company's Workers' Comp Costs in Colorado

Three levers move the needle most reliably:

Lower your EMR through fewer, properly closed claims. The single biggest driver is claim size, and claim size is decided by how the claim is handled. Right-sizing reserves and closing claims through documented medical records and light-duty return compounds — a clean year today lowers your mod for three renewal cycles. See our approach to loss control.

Reclassify employee roles accurately. Separating clerical, dispatch, and supervisory staff from field movers can save tens of thousands annually when you're on codes with $2–$3+ advisory loss costs. It's often the fastest fix because the work is documentary — you're correcting the math, not waiting for claims to run off.

Restructure into a high-deductible program — for qualifying businesses. For movers paying $100,000 or more in annual WC premium with a large enough workforce, a high-deductible structure is worth exploring. Not every business qualifies.

How High-Deductible Programs Work for Moving Companies

In a high-deductible program, the employer takes on a defined first layer of each claim — say the first $200,000 of a $500,000 policy — and the carrier covers the rest. Because the carrier's projected loss outlay drops, the underwriting premium can roughly halve at inception — an operation paying $100,000 might land near $50,000. The catch that makes it work: those retained claims aren't a lump-sum liability. They're funded incrementally, often around $3,000 a month, and the payments stop when the condition resolves. That only pencils out if someone is actively administering the claims — which is the whole point.

This is not a product you buy and walk away from, and it isn't right for everyone. PCI Consultants administers the program day to day: we handle the claim directly for the life of the policy, build the day-one medical record, drive light-duty return-to-work, contest exaggerated claims, and pay legitimate ones without dispute. We're compensated by commission from the insurer, not by your claims volume — so we're not incentivized to let a claim run. For a mover, the program bundles high-deductible placement, EMR reduction through loss-run audits and reserve right-sizing, in-house claims management, return-to-work design using light-duty moving roles (dispatch, inventory, packing supervision), and class-code reclassification. Individual results vary, and not every business qualifies.

Common Mistakes Colorado Moving Companies Make with Workers' Comp

Three mistakes show up repeatedly — and each costs more than it should:

Chasing the lowest quote while ignoring claims. A cheap first-year premium escalates fast if claims aren't controlled, and because premium stickiness means rates rarely fall back once they rise, the damage outlives the discount. The quote is the least important number on the page.

Letting the insurer run your claims. Without an advocate, a strained-back claim gets reserved at its inflated attorney number and paid near face value, and that reserve drives your mod for three years. Handling the claim directly — same-day urgent care, honest documentation, light-duty return — is what keeps the real cost near the real injury.

Running a single payroll file across all job functions. Field movers, drivers, warehouse workers, and office staff carry different codes and rates. When payroll isn't segregated, the auditor defaults to the highest applicable rate for anything ambiguous — a preventable overcharge.

The Concrete Next Step

If you want to know what you're actually overpaying, we don't need a long questionnaire. Send us two things: a copy of your current WC policy and your five-year loss runs. That's enough for us to review your classifications, read your EMR, and flag the open claims that are inflating it — and to tell you honestly whether a high-deductible structure fits your operation. It starts with a no-cost consultation.

Frequently Asked Questions

How much does workers' comp cost in Colorado?

Colorado ranks 28th of 51 jurisdictions at an index rate of $1.05 per $100 payroll — slightly below the $1.09 national median. For moving companies, rates run far higher because of physical injury risk, and your total annual cost depends less on the state environment than on your payroll, class codes, EMR, and how well your claims are managed.

How is workers' comp calculated in Colorado?

Colorado uses the NCCI formula: Classification Code Rate × Experience Modification Number × (Payroll ÷ $100) = Estimated Premium. Carriers can apply up to 25% in schedule credits or debits on top of filed rates, plus the DOWC surcharge of 1.43% for carriers. What the formula hides is that your experience modifier is set by how each claim was handled — which is where the multi-year cost is really decided.

Why do exaggerated claims cost my moving company so much?

Because reserves feed your EMR. When an attorney attaches a $250,000 figure to a strained back, the carrier reserves against it, and that reserve inflates your modifier for three policy years even if the claim never pays near that amount. The real medical spend on such an injury is often closer to $30,000, paid incrementally at roughly $1,500 to $2,000 a month. Documenting the true injury early — same-day urgent care — and contesting the inflated portion is what keeps your cost tied to reality. Individual results vary.

Do moving companies need workers' comp insurance in Colorado?

Yes. Colorado law requires all employers with one or more employees to carry workers' compensation — regardless of part-time status or hours worked. Moving companies, whose crews perform regular high-risk physical labor, are squarely subject to the requirement.

What class code do moving companies use for workers' compensation in Colorado?

Common NCCI codes include 7219 (local trucking), 8293/9519 for field movers, 8292 for warehouse workers, and 8810 for clerical staff. Verify exact phraseology in NCCI's Class Look-Up tool before finalizing — misclassification is one of the most frequent sources of overpayment, and correcting it is often the fastest way to cut a mover's premium.

How can a Colorado moving company lower its workers' comp premiums?

The highest-leverage steps: manage claims actively so your EMR stays low, correctly classify every role so you're not paying field-mover rates on clerical payroll, and — for qualifying businesses paying $100K+ annually — explore a high-deductible structure. PCI Consultants handles claims directly for the life of the policy, drives light-duty return-to-work, and right-sizes reserves; to start, send your current policy and five-year loss runs. Not every business qualifies, and individual results vary.