Most of those surprises aren't fraud. They come from avoidable mistakes in how payroll gets reported, how roles get classified, and how thin your documentation is when the auditor asks a hard question. For a healthcare employer with 100-plus staff and a six-figure comp spend, a single classification error or a missing certificate can turn a clean audit into a five-figure bill. Here's what the insurance company won't volunteer: the auditor's default is to resolve every ambiguity in the carrier's favor. This article breaks down where that happens and how to stop it.

TL;DR: Avoiding Costly Workers' Comp Audit Mistakes

- Misclassifying employees or reporting the wrong payroll basis are the most expensive audit errors, and both are fixable before the auditor arrives.

- Missing certificates of insurance for staffing agencies and 1099 contractors get their payroll added straight to yours.

- Your audit doesn't just set this year's bill. The audited payroll and your loss runs feed the experience mod that raises premiums for years, and those premiums rarely come back down.

- The best defense is a clean policy and clean loss history year-round, which is exactly what active claims management protects.

Common Causes of Workers' Comp Audit Mistakes

Most audit overcharges trace back to a short list of recurring errors. The good news: nearly all of them are documentation and classification problems you can control. Understanding where auditors look first is how you keep the final bill from ballooning.

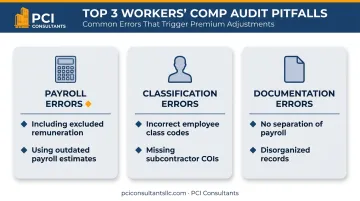

Payroll and Remuneration Errors

Your premium is built on payroll, so the payroll figure you hand the auditor is the single biggest lever on your bill. Reporting the wrong number, or the right number without records to back it up, costs real money.

The most common error is leaving excluded pay inside your reported payroll. Several forms of remuneration are exempt from premium calculation, but only if your records prove the split. Rules vary by state, but commonly excludable items include:

- The premium portion of overtime pay (the extra half of time-and-a-half)

- Severance or dismissal payments

- Tips and other gratuities

In a nursing home or home-health operation running heavy overtime to cover shifts, the overtime premium portion alone can be a large exclusion. If your payroll register doesn't separate it out, you lose it and pay premium on wages you never owed.

The second common error is riding on stale estimates. Your upfront premium is based on projected payroll. If you added a wing, opened a location, or grew headcount mid-year and never told your carrier, the audit finds the gap all at once and bills it in a lump. A broker who manages the policy actively updates that estimate as you grow so there's no year-end shock.

Beyond what you pay, who you pay and how they're coded matters just as much.

Classification and Personnel Errors

Every role carries a class code that reflects its actual injury risk, and this is where the costliest audit mistakes hide, in both directions. A ward clerk or scheduler sitting at a desk is low-risk and low-rate. A CNA lifting and transferring residents all shift is high-risk and high-rate. Lump them under one blended code and you either underpay (and get caught at audit) or, more often for healthcare employers, you overpay all year on clerical staff who were never bedside.

This is where careful risk classification earns its keep. The insurer has no incentive to volunteer that half your "nursing" payroll is actually administrative and belongs in a cheaper code. Segmenting the workforce by what people actually do, clerical versus high-risk hands-on, keeps you from overpaying on the low-risk roles, and it makes the audit a confirmation instead of a fight.

Staffing agencies and 1099 contractors are the other classic trap. If you bring in agency nurses or contract aides, you need a valid Certificate of Insurance (COI) proving they carry their own workers' comp. Without it, the auditor adds their entire payroll to yours as if they were your employees. As the North Carolina Rate Bureau explains, the hiring business is responsible for uninsured subs, and that cost lands on your bill. If you lean on staffing agencies to cover shifts, COI discipline isn't optional.

Both payroll and classification errors usually share one root cause: incomplete records.

Documentation and Process Errors

Poor record-keeping is what turns a defensible number into a lost argument. If your payroll register doesn't cleanly separate regular wages from overtime, you forfeit the overtime-premium exclusion. If you can't produce time records showing an employee split their week between the front desk and the floor, you lose the split.

"Separation of payroll" is the rule that lets you assign one employee's wages across two class codes when they genuinely perform two jobs, half in the office, half hands-on. It's valuable, but it demands strict, verifiable time-tracking. Without it, the New York State Insurance Fund notes the employee's entire payroll gets assigned to the highest-rated classification. In a hospital or senior-care setting, that's the difference between paying the clerical rate and the patient-care rate on the same paycheck.

What Happens If Audit Mistakes Are Ignored?

An audit adjustment isn't a one-time bill. It compounds.

The immediate hit is financial: a bill for additional premium that can run thousands to tens of thousands of dollars, dropped on your desk with little warning. For a 100-plus-employee employer that's a real cash-flow event.

But the lasting damage is in the machinery behind the bill:

- Higher upfront premium next term. Your carrier rolls the audited payroll into the estimate for the following year, so you start the next term paying more.

- A higher experience mod. Audited payroll and your claim history feed the experience modification factor that rating bureaus calculate, and a worse mod raises premiums across every policy year it touches.

And here's the part carriers rarely spell out: once a claim or an audit pushes your premium up, it almost never comes back down on its own, even after the underlying issue is resolved. Premium is sticky. That's why the cleanest audit strategy starts long before the auditor calls, with the loss history that feeds your mod in the first place.

Loss History Is Half of Your Audit

Your audited premium is a function of two things: payroll and losses. You can report payroll perfectly and still watch your premium climb because your loss runs are ugly, and loss runs get ugly when claims are left to run at face value. This is the difference active claims management makes.

When a worker is hurt, an advocate evaluates the incident immediately, often sending the injured worker to urgent care that same day to create an accurate, timely medical record. That record is what separates a genuine injury from an exaggerated one later. Left alone, an insurer's default is to pay a claim at or near the number a claimant's attorney floats, a "$250,000 claim," and call closing it a win. In practice the real medical spend on that same injury is often closer to $30,000, paid incrementally at roughly $1,500 to $2,000 a month, not as a lump sum. Every dollar of inflated claim cost flows into the loss runs that drive your experience mod, and through it, your future audited premium. Legitimate injuries get paid without dispute; exaggerated or fraudulent claims get investigated and contested. That's how you keep the loss history clean that your audit ultimately grades. Individual results vary.

At the far end, intentionally miscoding high-risk staff into clerical codes to shave premium isn't just an audit adjustment, it can be treated as insurance fraud, with fines and penalties attached. The goal is to pay the correct premium, not a fictional one in either direction.

How to Prevent Costly Audit Surprises

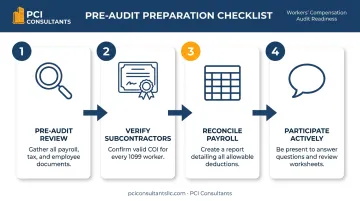

A smooth audit is the product of preparation, not luck. Instead of scrambling when the notice lands, work this checklist.

Conduct a Pre-Audit Review

Gather and organize everything the auditor will ask for before they schedule. Having it ready makes the audit faster and keeps the auditor from filling gaps with assumptions. Core documents:

- Payroll summaries: detailed journals or registers, with overtime broken out.

- Tax reports: quarterly 941s and state unemployment (SUTA) filings.

- Subcontractor and agency files: COIs for every 1099 worker and staffing agency.

- Employee detail: a roster with accurate, specific job descriptions, so clerical and patient-care roles are distinguishable.

Verify Every Subcontractor and Agency

Go through the policy period and confirm a valid COI for every contractor and staffing agency you paid. Each COI must:

- Show active workers' compensation coverage, and

- Cover the exact dates the work was performed.

Find a gap, chase the document now. Don't let the auditor find it first and bill you for it.

Reconcile Your Payroll

Build an "audit-ready" payroll report. Start from gross payroll on your 941s, then list every allowable deduction with the specific dollar amount, overtime premium portion, severance, tips, with records behind each line. The result is your true auditable payroll, fully defensible.

Be an Active Participant in the Audit

Don't hand over a box and walk away. Be present. Answer the auditor's questions in real time and explain what each role actually does, so a scheduler doesn't get coded as a floor nurse. Before the audit closes, ask to review the worksheets. That's your chance to catch a misclassification or a missed exclusion before the bill is finalized. If you disagree, your broker can dispute the finding with documentation rather than paying and hoping.

Tips for Long-Term Audit Preparedness and Control

The way to kill audit stress is to make preparedness a year-round habit, not a fire drill.

- Formalize subcontractor and agency compliance. No COI on file, no work begins. Make it a hard rule in onboarding, especially for agency staff covering shifts.

- Automate payroll separation. Configure payroll to split regular, overtime, and double-time automatically, and to tag clerical versus patient-care hours. Audit reporting then takes minutes.

- Get your class codes and program structure right. For complex or high-premium operations, the structure of the policy itself is the biggest lever. A high-deductible program lets a qualifying employer take on a defined first layer of risk (say the first $200K of a $500K program) while the insurer covers the rest, which can roughly halve annual premium (for example $100K down to $50K). Claim payments run monthly, around $3,000 a month, and stop when the condition resolves, and the whole thing is actively administered rather than left on autopilot. Not every business qualifies, but for those that do it changes what the audit even measures.

Multi-location owners have another lever. Several nursing homes under one owner can often be consolidated into a single master policy for better terms than each location negotiating alone, and one policy is far simpler to keep audit-ready than five.

This is where a specialist earns its fee. PCI Consultants has spent 30-plus years reviewing class codes, correcting the audit basis, and, critically, managing the claims that feed your loss runs. We're paid by commission from the insurer, not tied to your claims volume, so we're not incentivized to let your losses run. The point is to get your premium to the correct number and keep it there.

Frequently Asked Questions

What is the main purpose of a workers' comp audit?

The audit lets your insurer reconcile the payroll and operations it estimated when it wrote your policy against what actually happened during the year, then set your final premium accordingly. Because it's a reconciliation, the number can move in your favor too, if your records are clean and your class codes are right.

What records do I need for a workers' comp audit?

Payroll journals with overtime broken out, quarterly 941s, state unemployment filings, certificates of insurance for every subcontractor and staffing agency, and a roster with specific job descriptions so clerical and patient-care roles are distinguishable. The clearer the job detail, the harder it is for an auditor to default your staff into the highest-rated code.

Can I be charged for uninsured subcontractors or agency staff in an audit?

Yes. If you can't produce a valid COI showing a subcontractor or staffing agency carries its own workers' comp, the auditor adds their payroll to yours as if they were your employees. For healthcare employers leaning on agency nurses to cover shifts, this is one of the most common and expensive surprises.

Why did my premium go up after the audit even though I fixed the problem?

Because premium is sticky. Audited payroll and your loss history feed the experience mod, and once that mod climbs it rarely falls back on its own, even after the underlying claim or classification is resolved. That's why the real work is keeping payroll accurate and loss runs clean year-round, not just cleaning up at audit time.

What should I do if I disagree with the audit results?

Start by having your broker review the auditor's worksheets for misclassifications and missed exclusions, then file a formal dispute with the carrier backed by documentation. An advocate who manages your policy will contest a bad finding rather than pay it and move on, which is often the difference between the estimate and the real number.

How does my claims handling affect my audit?

More than most owners realize. Half your audited premium is driven by losses, so a claim allowed to settle at an inflated "lawyer number" instead of its real cost inflates the loss runs that set your future premium. Handling claims directly, documenting injuries the day they happen and moving workers to light duty quickly, keeps the loss history that your audit grades from working against you. Individual results vary.

Ready to get your class codes and audit basis reviewed before the next audit? Send us your current workers' comp policy and your five-year loss runs and we'll tell you where you stand.