Workers' compensation is one of the largest overhead lines in construction — and a lot of contractors overpay not because their crews get hurt more, but because their payroll is sitting in the wrong class code. Under California's dual wage system, a single documentation failure can shift an entire crew into a higher-rated code and inflate your premium retroactively, after the policy year has already closed.

Here's the part the insurance company won't volunteer: classification is only the front end of what actually drives your comp cost. The rate you pay per $100 of payroll matters, but so does what happens the day a worker gets hurt, how the claim is valued, and whether anyone is contesting the inflated numbers on your behalf. Most carriers, left to their own devices, pay claims at or near face value, call it a win, and let your premium ride up. This guide covers dual wage thresholds in full — and then connects them to the cost levers that compound the savings.

California is the primary state using this system, administered by the WCIRB (Workers' Compensation Insurance Rating Bureau). For contractors running significant payroll across multiple trades, getting this right is worth tens of thousands of dollars a year.

Key Takeaways

- Dual wage classifications split certain California construction trades into high wage and low wage tiers, each carrying a different workers' comp rate.

- Workers earning at or above the hourly threshold qualify for the lower-cost high wage code.

- Thresholds are reviewed annually by the WCIRB, effective September 1 — they don't move every year.

- Employers must keep original timecards with start/stop times and matching paystubs to substantiate high wage classification at audit; without them, auditors default workers to the higher-rated low wage code.

- Correct classification is the base layer. Active claims handling, faster return-to-work, and — for qualifying businesses — high-deductible structures are what multiply the savings on top of it. Individual results vary.

What Are Construction Dual Wage Thresholds?

The Basic Concept

California's dual wage system splits specific construction classifications into two tiers: a high wage code and a low wage code. Which one applies depends entirely on whether a worker's regular hourly rate meets or exceeds a defined dollar-per-hour threshold set by the WCIRB.

Same trade. Same duties. Different insurance rate — based solely on the worker's hourly pay.

Here's how that plays out:

- Carpenter earning $43/hour (threshold: $41/hour) → high wage code → lower premium rate

- Carpenter earning $38/hour (threshold: $41/hour) → low wage code → higher premium rate

The work is identical. Only the pay rate changes the classification.

Why This System Exists

The Dual Classification by Wage Level Program was adopted in 1986 after a WCIRB study found significant premium inequities driven by wage variation inside construction trades. The logic is actuarial: higher-paid skilled tradespeople tend to have more experience, better safety training, and steadier employers, and the data shows they produce fewer and less severe injury claims per $100 of payroll than lower-paid workers in the same trade.

According to the WCIRB's threshold review report, a classification qualifies for the program only when two conditions hold:

- Significant wage variation exists across employers in that trade

- A measurable disparity in claim costs per $100 of payroll exists between wage levels

Not every construction classification qualifies. Only trades where WCIRB data shows statistically credible wage-level differentiation are included.

This is the same principle that should govern your whole policy: segment the workforce by actual risk. A brokerage that classifies your crews correctly makes sure you're not paying high-risk rates on clerical, estimating, or supervisory payroll that belongs in a lower-risk code — the same way it makes sure your skilled field crews land in the high wage tier they've earned.

How Dual Wage Classification Directly Affects Your Premiums

The Rate Differential in Dollars

Workers' comp premiums follow a simple formula:

(Payroll ÷ $100) × Classification Rate × Experience Modifier

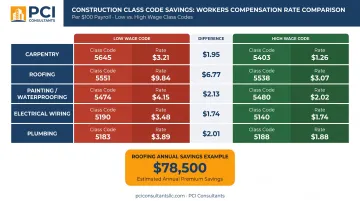

Because high wage and low wage codes carry different advisory pure premium rates, the same payroll dollars produce very different premium costs. Here is what the WCIRB's September 1, 2025 Pure Premium Rate Filing shows for common trades:

| Trade | Low Wage Code | Rate/$100 | High Wage Code | Rate/$100 | Difference |

|---|---|---|---|---|---|

| Carpentry | 5403 | $11.61 | 5432 | $5.54 | $6.07 |

| Roofing | 5552 | $21.80 | 5553 | $13.95 | $7.85 |

| Painting/Waterproofing | 5474 | $8.68 | 5482 | $4.68 | $4.00 |

| Electrical Wiring | 5190 | $3.95 | 5140 | $1.98 | $1.97 |

| Plumbing/Heating/Refrigeration | 5183 | $5.61 | 5187 | $2.91 | $2.70 |

On roofing alone, an employer with $1 million in roofing payroll pays roughly $78,500 more per year under the low wage code than the high wage code — for the same crew doing the same work.

The Experience Modifier Connection

The impact compounds beyond the base rate. Your experience modification factor (X-Mod) is calculated from expected losses tied to your class codes. Assign workers correctly to high wage codes — which carry lower expected loss rates — and your X-Mod improves over time as claim frequency drops. Lower base rates immediately, a better X-Mod at renewal: the dollar impact stacks year over year.

And here's what makes claims discipline so important on top of classification: once a claim drives your premium up, it rarely comes back down, even after the claim resolves. That premium stickiness is a multi-year cost. Correct classification sets a good baseline; keeping claims from inflating in the first place is what protects it.

The Audit Default Risk

Misclassification cuts both ways. If your records can't substantiate high wage classification at audit, every worker with incomplete documentation gets defaulted to the low wage (higher-rate) code — retroactively, for the entire policy period. That true-up shows up as an unexpected invoice after the year closes. The WCIRB's own guidance documents this exact scenario: electrical workers reassigned from Classification 5140 (high wage) to 5190 (low wage) because timecards lacked required start and end times.

Which Construction Classifications Have Dual Wage Thresholds?

The following thresholds are effective September 1, 2025, per the WCIRB's published threshold table. Always verify against your policy's effective date before renewal.

| Trade | Low Wage Code | High Wage Code | Threshold |

|---|---|---|---|

| Masonry | 5027 | 5028 | $35/hr |

| Electrical Wiring | 5190 | 5140 | $36/hr |

| Plumbing/Heating/Refrigeration | 5183 | 5187 | $32/hr |

| Automatic Sprinkler Installation | 5185 | 5186 | $33/hr |

| Concrete Work | 5201 | 5205 | $33/hr |

| Carpentry | 5403 | 5432 | $41/hr |

| Wallboard Installation | 5446 | 5447 | $41/hr |

| Glaziers | 5467 | 5470 | $39/hr |

| Painting/Waterproofing | 5474 | 5482 | $32/hr |

| Plastering/Stucco | 5484 | 5485 | $38/hr |

| Sheet Metal | 5538 | 5542 | $33/hr |

| Roofing | 5552 | 5553 | $31/hr |

| Steel Framing | 5632 | 5633 | $41/hr |

| Excavation/Grading | 6218 | 6220 | $40/hr |

| Sewer Construction | 6307 | 6308 | $40/hr |

| Water/Gas Mains | 6315 | 6316 | $40/hr |

What "Regular Hourly Wage" Means

The threshold applies to a worker's regular hourly wage — not total compensation, overtime pay, or annualized salary. Under the WCIRB's Uniform Statistical Reporting Plan, the regular hourly wage determination must be supported by original time cards, time book entries, or a valid collective bargaining agreement.

For workers paid on piece rates or salary who perform dual wage operations, review the USRP directly — or have a workers' comp specialist do it — before finalizing any classification. Misclassification in either direction creates audit exposure.

How to Identify Dual Wage Codes on Your Policy

- Review the Schedule of Classifications in your policy documents for every active class code

- Cross-reference each code using the WCIRB's Classification Search tool, filtering for dual wage classifications

- Confirm with your broker or WC consultant which operations fall under dual wage pairs — and whether any current assignments can be challenged and moved to the high wage code

How Dual Wage Thresholds Are Set and Updated

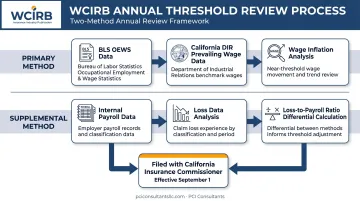

The Annual Review Process

The WCIRB reviews thresholds annually using two methods:

- Primary Method: Analyzes Bureau of Labor Statistics OEWS wage data and California Department of Industrial Relations prevailing wage data to measure wage inflation near current thresholds

- Supplemental Method: Validates threshold placement using internal unit statistical payroll and loss data to maximize the loss-to-payroll ratio differential between wage tiers

Proposed changes are filed with the California Insurance Commissioner under Insurance Code section 11734, and approved changes take effect September 1 each year.

Thresholds Don't Always Move

Updates are data-driven, not automatic. The 2023–2024 cycle brought increases across most trades (carpentry $39 → $41, roofing $29 → $31, masonry $32 → $35). The 2024–2025 cycle held every threshold steady. The practical takeaway: check the WCIRB's published threshold table before each renewal, not just at audit time. The thresholds in effect at your policy's start date govern the entire policy year.

Payroll Recordkeeping and Audit Preparation

What the WCIRB Requires

High wage classification isn't self-certifying. Under the WCIRB's Uniform Statistical Reporting Plan (Part 3, Section IV, Rule 2a), you must keep records that let an auditor independently verify each worker's regular hourly wage:

- Original timecards showing operations performed, total hours worked each day, and the exact start and stop times for each work period

- Paystubs that reconcile to those timecards so auditors can calculate the regular hourly wage

- For union employees, a valid collective bargaining agreement may substitute for individual timecards

Recording meal-period start/stop times isn't required if all operations uniformly cease during the break. If records can't verify the hourly wage, the USRP is clear: payroll goes to the higher-rated low wage companion code. Incomplete records have the same outcome as no records at all.

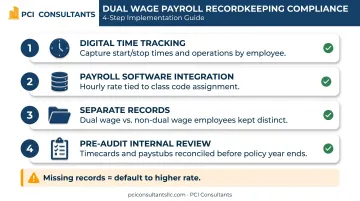

Practical Recordkeeping Steps

- Implement digital time-tracking that captures start and stop times by employee and records the operations performed. Paper timecards showing only total daily hours won't satisfy the requirement.

- Ensure payroll software captures hourly rate by classification so wage records tie directly to the class code on your policy.

- Maintain separate records for dual wage and non-dual wage employees so payroll isn't swept into the wrong classification pool.

- Run an internal pre-audit review before your policy year ends, confirming every dual wage employee's timecards and paystubs reconcile and would hold up under scrutiny.

When the auditor arrives, organized records close the case fast. Default classifications happen because auditors found gaps — not because the wage didn't qualify. A brokerage that actively manages your policy runs that pre-audit for you and defends the classifications at the audit table, rather than leaving you to explain a retroactive invoice after the fact.

How to Optimize Classification and Lower Workers' Comp Costs

Treat Classification as an Annual Exercise

Dual wage review shouldn't wait for an audit notice. Contractors who treat it as a proactive annual exercise — with their broker before each renewal — capture the savings reliably instead of discovering costly misclassifications after the fact.

Classification Is the Base Layer — Claims Handling Multiplies It

Here's what a broker who only touches your file at renewal will never tell you: correct class codes lower the base your premium is built on, but the biggest swings in construction comp come from how claims are handled after someone gets hurt. This is where PCI Consultants works differently. When a worker is injured, the contractor calls us, not the carrier. We evaluate the incident immediately and, where appropriate, send the injured worker straight to urgent care to create an accurate, timely medical record. That day-one record is what protects you against exaggeration weeks later — a genuine strain doesn't quietly become a disputed "permanent" back injury when the file was documented correctly from the start.

From there, the pattern typically looks like this:

- The "lawyer number" gets corrected. A claim posted as a $250,000 reserve often carries only ~$30,000 of real medical spend — paid incrementally, on the order of ~$1,500–$2,000 a month, not as a lump sum. Left unmanaged, the inflated reserve is what damages your loss runs and your X-Mod.

- Return-to-work happens in weeks, not months. A field worker who can't do full-duty framing can often move into a light-duty role — yard, tool room, safety spotter, or office support — within weeks, which sharply cuts the real cost of the claim. See our approach to a construction return-to-work program.

- Genuine claims are paid; exaggerated ones are contested. Legitimate injuries get paid without dispute. Exaggerated or fraudulent claims get investigated and challenged — which protects your loss history and your future premiums, since premiums rarely come back down once a claim pushes them up.

We're paid by commission from the insurer, not from your claim payments, so we're not incentivized by claims volume — our interest is in keeping your real cost, and your premium, as low as the facts allow. Individual results vary.

For Qualifying Businesses: High-Deductible Structures

Once classification is right and claims are under active management, a high-deductible program can roughly halve annual premium for the right contractor — for example, taking the first $200K of a $500K exposure while the carrier covers the rest, and moving a $100K premium toward $50K. Claim payments are structured monthly (on the order of ~$3,000/mo) and stop when the condition resolves, and the whole layer is actively administered rather than left to run. This isn't for everyone — not every business qualifies — but for contractors with the loss history and cash-flow profile to support it, it's a major lever. Learn more about large-deductible workers' comp.

The Full Cost-Control Picture

For construction employers, the levers stack:

- Accurate dual wage class codes reduce the premium base directly

- Risk-based classification across the workforce keeps low-risk payroll off high-risk rates

- Active claims handling and light-duty return-to-work hold down real claim cost and protect the X-Mod

- High-deductible structures, for qualifying businesses, apply on top of the baseline you've already built

One caution: national consultants frequently produce reclassification work that doesn't translate to California, because WCIRB's credibility weighting differs from the NCCI standards used in most other states. PCI Consultants has 30-plus years placing and actively managing construction workers' comp under WCIRB's system — including claims management for the life of the policy, not just placement.

The Concrete Next Step

If you're a contractor with significant California payroll — and especially if you're carrying $100K+ in annual comp — the fastest way to find out where you're overpaying is simple. Send us (1) a copy of your current workers' comp policy and (2) your five-year loss runs. From those two documents we can see your dual wage classifications, your X-Mod drivers, and the claims sitting at inflated reserves — and tell you specifically where the money is. Roofers can also review our roofing contractor coverage for trade-specific detail.

Frequently Asked Questions

What is the difference between a high wage and low wage construction classification?

Both codes cover the same type of construction work. The distinction is whether a worker's regular hourly wage meets or exceeds the WCIRB threshold. High wage carries a lower rate because, statistically, higher-paid workers produce fewer and less severe claims per $100 of payroll. Getting each worker into the tier their pay supports is the first thing we check when we review a construction policy.

How often are California's dual wage thresholds updated?

The WCIRB reviews thresholds annually for wage inflation, with approved changes typically effective September 1 — but they don't always move. The 2024–2025 cycle saw no increases; 2023–2024 brought increases across most trades. Because the thresholds in effect at your policy's start date govern the whole year, we check them at renewal, not just at audit.

What payroll records do I need to prove high wage classification?

At minimum: original timecards showing start and stop times for each work period, and paystubs that reconcile to those timecards. Together they let an auditor verify each worker's regular hourly wage against the threshold. We run a pre-audit review of these for the clients we manage so the classifications hold up before the auditor ever arrives.

What happens if I don't have proper records during a workers' comp audit?

If records can't verify the high wage rate, auditors default that worker's payroll to the low wage (higher-rate) code — retroactively, regardless of what the worker was actually paid — which can land as a significant surprise invoice after the year closes. Active audit defense is exactly the kind of thing a carrier won't do for you but a claims-managing broker will.

Does the dual wage classification system apply outside California?

The dual wage program as described is specific to California and administered by the WCIRB. Other states run their own classification mechanisms under NCCI or independent bureaus, and the rules vary significantly. Check your state's rating bureau — and be careful with national reclassification advice, which often doesn't translate to California's credibility weighting.

How do I find out which class codes on my policy are dual wage classifications?

Review the Schedule of Classifications in your policy documents, use the WCIRB's online Classification Search filtered for dual wage codes, or ask your broker or WC consultant to flag them. If you send us your current policy and five-year loss runs, we'll mark the dual wage pairs, flag any that can be challenged, and tell you what it's worth. Individual results vary.