That single omission can turn a routine project into a financial and legal problem that lands on you. Hiring a contractor without workers' comp doesn't just save them money — it quietly moves all of their on-the-job injury risk onto the business that hired them. Here's the exposure you take on, and the exact steps to keep it off your books.

Key Takeaways

- Non-compliance can trigger six-figure fines and Stop-Work Orders.

- Demand a Certificate of Insurance (COI) and verify the policy is active by calling the carrier.

- An uninsured sub's injury can hit your own loss runs — and premiums rarely fall back down.

Why Businesses Hire Uninsured Contractors (The Temptation)

The choice to hire an uninsured contractor rarely comes from bad intent. It usually comes from a few powerful — and deeply flawed — assumptions that hide the real cost.

The Lure of Lower Costs

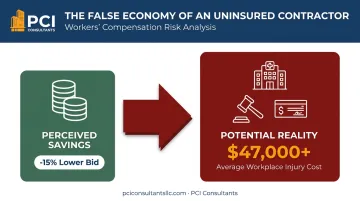

The most common reason is simple: a lower price. Workers' comp is a real operating expense for any contractor, so dropping it lets them slash overhead and undercut their insured competitors by a wide margin.

That creates a strong incentive to look the other way. It's also a textbook false economy. The few thousand dollars you save on the contract are nothing next to the cost of a single injury claim. The National Safety Council reports the average work injury cost $47,316 in 2022-2023.

Here's what the insurance company won't tell you: that number is the sticker price, not the settled price. Left unmanaged, a claim often gets paid at or near face value because that's the path of least resistance for the insurer. A brokerage that handles the claim directly can frequently resolve a genuine injury for a fraction of the headline figure — more on that below.

Misunderstanding of Liability and State Laws

Many owners believe they aren't responsible for injuries to independent contractors — that the liability stays with the contractor as a separate business.

That assumption is wrong in most states. Workers' comp statutes are written to make sure an injured worker gets paid by someone. If the subcontractor is uninsured, the law usually reassigns liability up the chain to the general contractor or property owner who hired them. In practice, you become the insurer of last resort.

The Assumption of Independence

The line between a true independent contractor and an employee can be blurry, and getting it wrong is expensive. A business may treat a worker as a 1099 without applying the legal tests. If you control how the work gets done, a regulator or auditor can reclassify that worker as your employee. Red flags include:

- Dictating their work hours

- Providing their primary tools and equipment

- Controlling how the work is performed

For a deeper look at where the line sits, see our breakdown of why independent contractors are generally not covered under your policy — until an auditor decides they are.

The High Cost of Ignoring Workers' Comp (The Reality)

Hiring an uninsured contractor is a gamble where the losses are lopsided. When an accident happens, the consequences hit fast and from several directions at once.

Direct Financial Liability for Injuries

If an uninsured contractor is hurt on your job site, you're on the hook. You effectively become their insurance company — without any of the infrastructure to manage the cost. That means paying for:

- All medical expenses: ER visits, surgery, rehab, and long-term care.

- Lost wages: their income while they can't work.

- Disability payments: potentially for years if the injury is permanent.

With the total cost of a medically consulted injury averaging $48,000, a single fall from a ladder can erase any initial savings and threaten your stability.

This is exactly where having someone manage the claim changes the math. Take what we call the "lawyer number." An attorney or an unmanaged file might frame a serious injury as a $250,000 claim*. When the incident is evaluated immediately — the worker sent to urgent care that same day so there's an accurate, timely medical record — the real medical spend often lands closer to *$30,000, paid incrementally at roughly $1,500 to $2,000 a month rather than as a lump sum. That day-one record is what protects you against later exaggeration. Individual results vary, but the gap between the story and the settled cost is usually enormous.

Severe Legal and Regulatory Penalties

State workers' comp boards enforce compliance aggressively, and the penalties are built to hurt.

- In California, fines can reach $100,000 for hiring an uninsured worker.

- New York can levy penalties as high as $2,000 for every 10-day period of non-compliance.

- Florida can issue a Stop-Work Order that halts all operations immediately, plus a penalty equal to twice the premium that should have been paid.

These fines stack on top of your liability for the injury itself.

Exposure to Lawsuits

Workers' comp provides a critical protection called "exclusive remedy." When an employer has coverage, an injured worker gets guaranteed benefits but gives up the right to sue for negligence.

With no insurance, that protection vanishes. The injured worker is free to file a personal injury lawsuit against you for pain and suffering, emotional distress, and damages that dwarf standard comp benefits. These suits can easily run into hundreds of thousands — or millions.

The Hit to Your Own Insurance (What the Insurer Won't Tell You)

You might assume your General Liability policy will catch this. That's a risky bet — many GL policies exclude injuries to uninsured subcontractors. Worse, this exposure loops back into your workers' comp program in two ways most owners never see coming:

- Audit charge-back. At your annual workers' comp audit, auditors treat an uninsured sub's payroll as your payroll and charge additional premium for it. You end up paying for coverage the contractor was supposed to carry.

- Premium stickiness. If that sub's injury lands on your loss history, it inflates your experience rating — and here's the part insurers gloss over: once premiums go up after a claim, they rarely come back down, even years after the claim is closed. One uninsured sub can quietly cost you across multiple renewal cycles.

That's the difference between an insurer, whose default is to pay a claim at face value and call it a win, and an advocate whose job is to keep your loss runs — and therefore your future premiums — as low as honestly possible.

A Step-by-Step Guide to Vetting Contractors

Protecting yourself is straightforward, but it takes discipline. Run this on every contractor and subcontractor you hire.

Step 1: Require Proof of Insurance Upfront

Make workers' comp a non-negotiable line in your bid request. If a contractor can't provide proof of coverage, they're disqualified — before the low bid ever tempts you.

Step 2: Scrutinize and Verify the Certificate of Insurance (COI)

A Certificate of Insurance proves active coverage. Don't just file it. Confirm:

- The contractor's business name matches exactly.

- The policy effective dates cover the entire duration of your project.

- The coverage limits meet your requirements.

- The carrier's name and contact information are clearly listed.

Then verify it's active. Call the insurance carrier directly — using the number from their official website, not the one printed on the certificate. Provide the policy number and confirm coverage is in good standing. This one step is your best defense against a forged or canceled certificate.

Step 3: Use a Written Contract

Never rely on a handshake. A written contract is your most important layer of legal protection. It should state plainly that the contractor must carry and maintain their own workers' comp for the life of the project.

Include an indemnification clause (a "hold harmless" agreement) that legally obligates the contractor to cover any losses, claims, or legal fees you incur from their work, errors, or lack of insurance.

Step 4: Understand Worker Classification

Classify 1099 workers correctly under IRS guidelines, which weigh behavioral control, financial control, and the nature of the relationship. In general, a worker is an employee if you can control what will be done and how it will be done. If you set their hours, supply their primary tools, and direct the details of the work, they may legally be your employee — making their comp coverage your responsibility. When in doubt, get advice before the auditor makes the call for you.

Long-Term Strategies for Contractor Risk Management

If you hire subcontractors regularly, a one-off check isn't enough. You need a system — and, above the right size, a partner who actively manages the exposure rather than just filing certificates.

- Establish a formal pre-qualification process. Require every contractor to complete a standard application, provide references, and submit a valid COI before they bid.

- Create a centralized tracking system. Keep a digital file of every active COI and set reminders 30 days before each policy expires so you never have a coverage gap.

- Classify your own workforce by real risk. Not every role carries the same injury exposure. Segmenting clerical staff from high-risk hands-on crews — so you're not overpaying premium on low-risk payroll — is one of the fastest ways to stop leaking money.

- Get claims handled directly. For qualifying employers, the biggest lever isn't paperwork — it's who answers the phone when an injury happens. When you call the brokerage instead of the insurer, the incident gets evaluated immediately, a genuine injury gets paid without a fight, an exaggerated or fraudulent one gets investigated and contested, and light-duty return-to-work often moves an injured worker into a modified role within weeks — sharply cutting the real cost of the claim.

For businesses with high workers' comp spend or heavy contractor exposure, working with a specialist buys a level of protection an internal spreadsheet can't. For larger, qualifying employers there are also structural options — like high-deductible programs where you take a defined first layer of loss and the insurer covers the rest, which can roughly halve annual premium and pay claims in managed monthly increments that stop when the condition resolves. It doesn't fit every business, but where it fits, it's a different economic model entirely.

One more thing worth knowing: our team at PCI Consultants is paid by commission from the insurer, not from your claims. We aren't incentivized by how many claims you file — we're incentivized to keep your program clean and your costs down. Get expert oversight on your contractor compliance and your policy is administered, not just sold.

Conclusion

The low bid is tempting, but the savings from an uninsured contractor are an illusion — they hide catastrophic liabilities that land squarely on you, and they can quietly ride on your loss runs and premiums for years. Due diligence isn't optional; it's the basic cost of operating safely. Verify insurance, use real contracts, classify workers correctly — and for anything above a simple project, put an active claims manager between you and the insurer's default of paying every claim at face value.

Frequently Asked Questions

What if a contractor does not have workers' comp?

The party that hired them — a general contractor or property owner — typically inherits the full legal and financial liability for any workplace injury. That means medical bills, lost wages, disability, and potential state fines. And if that injury attaches to your policy, an auditor may also bill you additional premium for the uninsured sub's payroll at your next audit.

Do independent contractors need their own workers' comp?

Rules vary by state, but it's a critical protection for the contractor and a non-negotiable requirement for anyone hiring them. Without it, the hiring party absorbs the entire risk of an on-the-job injury — including a lawsuit, since "exclusive remedy" doesn't apply when there's no coverage.

Can I be sued if an uninsured contractor gets hurt on my property?

Yes. Without workers' comp, the "exclusive remedy" protection that normally caps lawsuits disappears. You can be sued directly for negligence, pain and suffering, and other damages. This is also where the "lawyer number" shows up — an inflated demand that a directly managed claim, backed by an accurate day-one medical record, can often bring back toward the true cost.

What is a Certificate of Insurance (COI) and what should I look for?

A COI is documentation of active coverage. Check that the business name matches exactly, the policy dates cover your entire project timeline, the limits meet your requirements, and the carrier's name and contact details are listed. Then verify it — a certificate on its own can be forged or out of date.

How can I verify if a contractor's workers' comp policy is active?

Call the carrier directly using the phone number from their official website, not the number printed on the certificate. Give them the policy number and ask them to confirm the policy is active and hasn't been canceled. It's five minutes that can save you six figures.

How does an uninsured contractor's injury affect my own premiums?

More than most owners expect. If the claim lands on your loss history, it raises your experience rating — and once premiums rise after a claim, they rarely come back down, even after the claim closes. That's why keeping uninsured subs off your job sites, and getting real claims managed directly when injuries do happen, protects your costs for years, not just the current policy term. Individual results vary.