Here's what the insurance company won't tell you: left to its own devices, a carrier will often pay a claim at or near its face value and call that a win. Fighting an inflated claim costs the insurer time and legal spend, so the path of least resistance is to write the check — and let your renewal premium absorb it. That's the gap an active broker closes.

At PCI Consultants, we handle the claim directly for the life of the policy — your team calls us, not the insurer. Genuine injuries get paid without a fight. Exaggerated and fraudulent ones get investigated and contested. This article covers what qualifies as fraud under Florida law, how investigations actually work, what investigators can and cannot legally do, the red flags that trigger scrutiny, and how proactive claims handling keeps a suspicious claim from becoming a multi-year premium problem.

Key Takeaways

- Florida Statute §440.105 makes workers' comp fraud a felony for claimants, employers, and providers alike

- The state's Bureau of Workers' Compensation Fraud received 1,055 fraud referrals in FY 2023–2024, resulting in 166 arrests

- The most common claimant fraud isn't a fabricated injury — it's an exaggerated one, where the worker was genuinely hurt but overstates the limitation

- Florida's all-party consent law means recorded conversations must be authorized by all parties; violations can get your evidence thrown out and expose you to liability

- A single inflated lost-time claim compounds across three renewal cycles through the experience mod — and once your premium rises, it rarely comes back down

What Counts as Workers' Compensation Fraud Under Florida Law

Florida Statute §440.105 defines workers' comp fraud broadly: any intentional false statement, misrepresentation, or omission made to obtain, deny, or reduce a benefit or payment. It applies to every party — claimants, employers, and medical providers.

One clarification worth making up front, because it drives how we handle claims: most of what inflates a Florida employer's cost isn't outright criminal fraud. It's exaggeration — the "lawyer number." A claim gets framed as a $250,000 injury when the real, defensible medical spend is closer to $30,000. That's not always prosecutable, but it's exactly the gap a broker who manages the claim directly is there to close.

Claimant Fraud

The most common forms include:

- Faking or exaggerating an injury

- Claiming a non-work injury as work-related

- Collecting disability benefits while secretly working

- Failing to disclose pre-existing conditions that contributed to the claimed injury

In a skilled nursing or home-health setting, the classic pattern is a lifting or slip injury with no witnesses, reported days after it supposedly happened. That delay is exactly why we push for an immediate, accurate medical record — more on that below.

Employer Fraud

Employers aren't exempt. §440.105 specifically covers:

- Misclassifying employees as independent contractors to avoid coverage

- Under-reporting payroll to reduce premium

- Manipulating payroll records submitted to insurers

- Failing to carry required workers' comp coverage altogether

Provider Fraud

Medical providers face prosecution under §440.105 for:

- Billing for services not rendered

- Inflating treatment costs beyond actual charges

- Referring claimants to affiliated providers for kickbacks

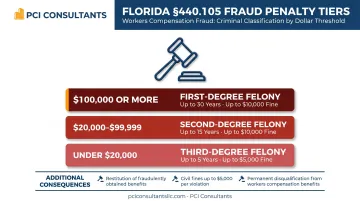

Penalties

Penalty tiers under §440.105 are tied to dollar amounts:

| Fraud Amount | Offense Level |

|---|---|

| Under $20,000 | Third-degree felony |

| $20,000–$99,999 | Second-degree felony |

| $100,000 or more | First-degree felony |

Beyond criminal prosecution, convicted parties face restitution orders, civil fines, and permanent disqualification from receiving workers' comp benefits.

Most Common Types of Workers' Comp Fraud Investigated in Florida

The state's FY 2023–2024 joint report from the Bureau of Workers' Compensation Fraud gives a clear picture of what investigators actually see:

- Employee claimant fraud: 516 referrals

- Employer premium fraud: 154 referrals

- Working without coverage: 136 referrals

- Provider fraud: 20 referrals

That year produced 166 arrests, 163 successful prosecutions, and $13.7 million in restitution ordered.

Exaggerated Injuries

The most frequently investigated form of claimant fraud isn't a fabricated injury — it's an exaggerated one. The worker was genuinely hurt but overstates functional limitations to extend benefits or avoid returning to work. This is the single biggest driver of the "lawyer number" problem, and it's where hands-on claims handling earns its keep. We don't dispute the real injury; we dispute the inflation on top of it.

Working While Collecting

A claimant receives total or partial disability benefits while performing paid work — often off the books. Investigators look for this through physical surveillance and employment record checks. A structured return-to-work program also closes the door on this: a worker offered light duty who refuses it, then turns up working elsewhere, tells you everything you need to know.

Employer Payroll Fraud

Deliberate misclassification and payroll under-reporting are the primary employer-side concerns. Both distort the experience modification rating (EMR) and, when caught, carry felony exposure. In March 2026, Florida's CFO announced an arrest in a case involving an alleged $1,090,504 in premium avoidance. Proper risk classification — segmenting clerical staff from high-risk hands-on roles — is the legitimate way to avoid overpaying, and it holds up under audit.

Provider Fraud

The Division of Criminal Investigations pursues provider fraud involving unnecessary procedures, falsified diagnoses, and kickback referral arrangements. With only 20 provider-fraud referrals in FY 2023–2024, these are a smaller share of volume, but the dollar amounts per case run substantially higher — which is one reason we route injured workers to a documented, authorized provider from day one.

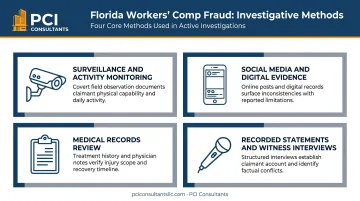

How Workers' Comp Fraud Investigations Are Conducted in Florida

Surveillance and Activity Monitoring

Licensed private investigators — or insurer in-house investigators — conduct physical surveillance in public spaces, documenting daily activities through video and photographs. Under Florida law, surveillance conducted reasonably and non-intrusively in public can be used as evidence. Investigators then cross-reference observed activity against the claimant's stated medical restrictions.

When indicators cross into criminal territory, the Bureau of Workers' Compensation Fraud deploys its own state detectives. The bureau operates with 21 detectives, 2 intelligence analysts, 4 supervisors, a Captain, and a Bureau Chief — handling 1,055 referrals and initiating 234 cases in FY 2023–2024.

Investigators typically look for discrepancies across several activity types:

- Physical tasks the claimant performs that exceed their reported restrictions

- Travel, recreation, or employment not disclosed to the insurer

- Witness accounts that conflict with the claim

- Patterns of activity — not isolated incidents — that build a credible record

Social Media and Digital Evidence

Investigators review public posts, photos, location tags, and content other users tag the claimant in. A photo at a family cookout, a check-in at a sporting event, a comment about feeling great — any of these can contradict claimed physical limitations.

Social media evidence in Florida must be properly authenticated under §90.901 to be admissible. It's not self-authenticating, and investigators who skip the chain of custody risk having valuable evidence excluded.

Medical Records and the Day-One Record

Investigators analyze medical records for consistency across the accident report, diagnosis, and treatment plan, and review prior injury history to identify pre-existing conditions under §440.13.

This is where an active broker changes the outcome before an investigation is ever needed. When one of your workers is hurt, they call us, not the insurer. We evaluate the incident immediately and, when warranted, send the worker to urgent care right away. That creates an accurate, timely, contemporaneous medical record — the single best protection against a claim that gets exaggerated weeks later. A vague, late-reported "my back has been hurting" is far harder to inflate when there's a same-day exam on file describing exactly what happened. Our medical management team keeps that record consistent through treatment.

Common red flags in the record review:

- Gaps in treatment or missed appointments

- Care sought outside the authorized provider network

- Diagnoses that don't align with the reported injury mechanism

- Treatment duration inconsistent with the documented injury

Recorded Statements and Witness Interviews

Investigators compare statements made to the employer, insurer, and treating physicians, looking for inconsistencies in timeline, injury mechanism, or symptom description. Witness interviews typically draw from coworkers and supervisors, neighbors, and family members whose accounts may contradict the claimant's stated limitations. Any discrepancy across these statements becomes part of the investigative record.

What Florida Workers' Comp Investigators Can and Cannot Do

Understanding these boundaries matters — both for managing an investigation and for making sure the evidence holds up.

Investigators may:

- Conduct surveillance in public places

- Review publicly available social media

- Interview witnesses

- Examine records obtained through legal means

Investigators may not:

- Trespass on private property

- Record someone inside their home

- Make false statements to obtain information

- Record private conversations without all-party consent

Florida Statute §934.03 requires all-party consent for recording private conversations. Florida is a two-party consent state — an investigator cannot record a phone call or private conversation without every participant's knowledge. Unauthorized recording is a third-degree felony.

Cross those lines and the exposure lands on the employer, not just the investigator:

- Illegally obtained evidence can be ruled inadmissible under §934.06

- The investigator and employer can face civil damages under §934.10, including statutory minimums, punitive damages, and attorney fees

- Criminal liability is possible in egregious cases

The practical takeaway: this is not a DIY exercise. When a case genuinely warrants a fraud investigation, it should run through approved, licensed vendors inside a disciplined process — so the evidence is clean and the case survives a challenge. If it escalates to a criminal matter, state detectives can pursue a court warrant to authorize phone surveillance; without one, the recording restrictions apply fully.

Red Flags That Trigger a Workers' Comp Fraud Investigation

No official Florida DFS checklist exists, but these patterns consistently trigger scrutiny — drawn from DFS fraud guidance and NCCI claims data.

Claim-level red flags:

- Claim filed right after a layoff announcement or disciplinary action

- Injury with no witnesses and a vague or inconsistent description

- Resistance to medical evaluations or return-to-work offers

- Prior claims history showing similar injuries across multiple employers

- Delayed reporting beyond the 30-day employee notification window under §440.185

- Symptom progression that doesn't match the reported injury

Employer-side red flags (per DFS fraud guidance):

- Under-reported payroll or workers paid in cash with no records

- Employees classified as contractors in roles that don't support it

- Improper loss experience factors submitted to the insurer

- Operating without required coverage

Florida requires employees to notify their employer within 30 days of an injury, and employers to report to their carrier within 7 days. The point of active claims handling is to see these flags on day one — not at renewal, when the cost is already baked in. If you're weighing whether to dispute a questionable claim, that decision is far stronger when the record was built correctly from the start.

Predictive analytics are now standard among Florida insurers, which flag claims automatically when treatment costs run high for the injury type or the pattern falls outside the norm.

How Workers' Comp Fraud Affects Florida Employer Premiums

Fraud's financial damage comes through two channels: the direct cost of the claim, and the downstream hit to your experience modification rating (EMR).

The EMR, as explained by NCCI, compares your actual losses against expected losses for similarly classified employers. A debit mod above 1.000 means worse-than-average experience — and higher premium. The rating period spans roughly three years of claims history, so one inflated claim rides along for three consecutive renewals.

And here's the part that stings: once your premium goes up after a claim, it rarely comes back down, even after the claim resolves. A lost-time claim that settles at an inflated $150,000 doesn't just cost $150,000 — its EMR impact across three policy years can compound to well over $100,000 in additional renewal premium. That's why the difference between paying the $250,000 "lawyer number" and defending the claim down to its real $30,000 value isn't a one-year saving. It's a multi-year one.

There's also a better way to pay the legitimate portion. A real injury doesn't have to be settled as a single inflated lump sum. When we handle a claim directly, defensible medical costs are paid incrementally as care is delivered — often on the order of $1,500–$2,000 a month — and payments stop when the condition resolves. Pair that with a fast, documented light-duty transition — moving an injured nurse into a receptionist-type role within weeks instead of leaving her out on total disability for months — and the real claim cost drops sharply, which is exactly what protects the EMR.

For Florida operators in high-injury sectors — skilled nursing, home health, hospitals — the stakes are highest. High base rates plus a deteriorating mod make coverage genuinely hard to manage. For qualifying employers, structuring the program differently — for example, a high-deductible or loss-sensitive plan where you take a defined first layer of risk and the insurer covers the rest — can roughly halve annual premium and put day-to-day claim administration in the hands of an advocate who is actually motivated to minimize each claim. Not every business qualifies, and the right structure depends on your loss history.

Proactive Claims Management as the Best Defense

The most effective protection is catching a suspicious claim early — before costs escalate and inflated reserves lock in. That takes a structured process, not case-by-case reaction. PCI Consultants' in-house team runs a five-step process:

- Software screening flags claims early on prior history, attorney-representation timing, treating-provider patterns, and return-to-work refusals

- AOE/COE investigation determines whether the injury arose out of and in the course of employment — the foundational compensability question

- Coordinated surveillance through approved, licensed vendors when the indicators warrant it

- IME coordination for an independent medical assessment of claim validity

- Disposition: pay the legitimate claim, settle at a supportable value, or defend fully

Because we're paid by commission from the insurer — not tied to your claims volume — we're not incentivized to let a claim run high. Our interest is the same as yours: pay what's real, contest what's inflated, and keep your loss history clean. This approach suppresses both the direct claim cost and the multi-year EMR penalty that would otherwise compound. Individual results vary. Florida employers in healthcare and home care with $100K+ in annual workers' comp premium can start with a no-cost consultation.

How to Report Workers' Compensation Fraud in Florida

Florida Statute §440.1051 established a dedicated toll-free hotline operated by the Bureau of Workers' Compensation Insurance Fraud. Anyone — employers, coworkers, providers, or the public — can report suspected fraud.

| Method | Contact |

|---|---|

| Phone | 1-800-378-0445 |

| Online | FraudFreeFlorida.com |

What to include:

- The claimant's or employer's name and contact information

- The nature of the suspected fraud

- Supporting documentation (photos, videos, records)

- Any witness information

Good-faith reporters are protected from civil liability and retaliation under §440.1051 — as long as the report is honest. A knowingly false fraud report is itself a third-degree felony.

Frequently Asked Questions

Are private investigators used to monitor workers' comp claimants in Florida?

Yes. Carriers and brokers frequently retain licensed private investigators for surveillance in Florida workers' comp cases. It's legal when conducted in public and non-intrusively, and the footage can support a claim dispute or criminal proceeding. The key is running it through a disciplined process so the evidence is clean — we only deploy surveillance when the indicators genuinely warrant it, never as a fishing expedition against a legitimate injury.

How do I report workers' comp fraud in Florida?

Call the Bureau of Workers' Compensation Insurance Fraud at 1-800-378-0445 or visit FraudFreeFlorida.com, as authorized under §440.1051. Reporters acting in good faith are protected from civil liability under that same statute.

What is the most common type of workers' comp fraud in Florida?

Exaggerating injury severity is the most frequently investigated claimant fraud — the worker was really hurt but overstates the limitation. On the employer side, payroll misclassification and under-reporting are most common. Both quietly raise premiums for every Florida employer carrying coverage, which is why we separate the genuine injury (paid without dispute) from the inflated one (investigated and contested).

What are the penalties for workers' compensation fraud in Florida?

Under §440.105, penalties range from third-degree felonies (under $20,000) to first-degree felonies ($100,000 or more), plus court-ordered restitution, fines, and potential loss of workers' comp eligibility.

How long does a workers' comp fraud investigation take in Florida?

Anywhere from a few days to several months, depending on complexity, how much surveillance is needed, and whether it escalates to state criminal investigators. No statutory time limit governs the duration — which is another reason early, active claims handling matters: the sooner an issue is caught, the less reserve and premium damage it does.

Can an employer be investigated for workers' compensation fraud in Florida?

Yes. §440.105 applies to employers who misclassify employees, under-report payroll, or fail to carry required coverage. Violations carry the same felony tiers — up to first-degree charges over $100,000 — as claimant fraud. Accurate risk classification and clean payroll reporting are the legitimate way to keep premium down without exposure.