At PCI Consultants, risk management is not safety posters and incident binders. Over 30+ years we've built a program where we place the coverage and then actively manage the claim for the life of the policy — the injured worker (or the employer) calls us, not the carrier. That single structural change is what separates employers whose premiums stay flat from those who watch them climb and never come back down.

This guide walks through the strategies that actually move the number: risk assessment and classification, injury prevention, day-one claims handling, return-to-work, data monitoring, and structuring the insurance program so you pay for your real risk instead of the carrier's worst-case guess.

Key Takeaways

- The insurer's default is to pay claims near face value; without an advocate managing the file, you overpay on nearly every incident.

- The "lawyer number" is not the real number — a claim reserved at $250,000 often costs closer to $30,000 in actual medical spend, paid incrementally (roughly $1,500–$2,000/month), not as a lump sum.

- A fast, documented day-one medical record — sometimes an immediate urgent-care visit — is your best protection against later exaggeration.

- Return-to-work in weeks (light duty), not months, is the single biggest lever on real claim cost.

- Premiums are sticky: once they rise after a claim, they rarely fall back — so the time to control cost is during the claim, not after.

- High-deductible structures can roughly halve annual premium for qualifying businesses — not every business qualifies, and the program has to be actively administered.

What Is Risk Management in Workers' Compensation?

Workers' comp risk management is the systematic work of identifying, evaluating, and reducing what you actually pay in losses — both how often claims happen and how much each one really costs. It runs on two tracks:

- Loss prevention — stopping injuries before they happen through hazard controls, training, and correct risk classification.

- Claims management — controlling the cost and outcome of each claim once an injury occurs.

Here's the part the insurance company won't volunteer: the second track is where most of the money is left on the table. Prevention lowers frequency, but an actively managed claim is what keeps a legitimate $30,000 injury from being reserved, and eventually paid, as a $250,000 loss that follows you for years. We handle the claim directly — evaluating the incident the moment it's reported, directing care, and paying genuine costs incrementally as they're actually incurred.

Why Every Claim Has a Lasting Financial Impact

Your premium isn't priced off this year's injuries alone. The experience modification rate (e-mod) rolls three years of loss data into a multiplier on your base premium. A 1.25 e-mod on a $100,000 base premium produces a $125,000 modified premium — and that modifier stays in the math for three full policy years.

Now layer on premium stickiness: once a bad loss year pushes your rate up, carriers are slow to bring it back down even after the claim resolves. So an inflated claim isn't a one-year problem — it's a multi-year surcharge. That's why getting the number right in month one, before it hardens into your loss history, is one of the highest-return things an employer can do. Individual results vary, but the pattern is consistent: controlled claims cost, controlled premium.

Conduct a Thorough Workplace Risk Assessment

A risk assessment maps every way your organization is exposed to loss — physical hazards, operational risk, compliance gaps, and how your payroll is classified. Without that baseline, prevention is scattered and you're almost certainly overpaying somewhere.

Start with Historical Claims Data

Pull the last three to five years of loss runs and read them like a map of where the next claim will come from:

- Which units generate the most claims — med-surg floors, transfers and lifts, the parking lot?

- Which job classifications show up again and again?

- Are injuries clustered around specific tasks, shifts, or times of year?

Past claims are the clearest signal you have. (They're also exactly what we ask for when we take over a program — your current policy plus five years of loss runs tells us in an afternoon where your money is going.)

Walk the Floor and Talk to Employees

Front-line staff see hazards management doesn't. In a nursing home that's the resident who reliably resists transfers, the med cart with the sticky wheel, the understaffed night shift where lifts happen solo. Regular walkthroughs plus direct employee input surface the near-misses — injuries that haven't happened yet.

Get Job Classifications Right — Don't Overpay on Low-Risk Roles

This is where employers quietly bleed money. Workers' comp rates apply per $100 of payroll by class code, and a hands-on caregiver carries a very different rate than a scheduler or a billing clerk. Lump everyone into the high-risk code and you overpay on every low-risk paycheck, every renewal. We segment your workforce by actual risk — clerical and administrative roles priced as clerical, hands-on care priced as care — so you're not subsidizing risk you don't run. Correcting classification before an audit, not after, is one of the cleanest premium wins available.

Reassess Continuously

Exposure shifts every time conditions change on the ground. Trigger an immediate reassessment on any of these:

- New equipment, lifts, or clinical procedures

- A new location, a wing added, or a layout change

- Seasonal staffing ramps or new job classifications

- A spike in claims or near-misses in any unit

For multi-site owners — say, several nursing homes under one entity — reassessment is also the moment to ask whether consolidating locations onto a single master policy would earn better terms than carrying each facility separately. It often does.

Prevention Strategies That Reduce Workers' Comp Claims

Implement Rigorous Safety Protocols

Identified hazards need controls, ranked from most to least effective by the CDC/NIOSH Hierarchy of Controls:

- Elimination — remove the hazard entirely

- Substitution — replace it with something less hazardous

- Engineering controls — physical changes (ceiling lifts, ergonomic equipment, guarding)

- Administrative controls — procedures, staffing ratios, rotation

- PPE — last line of defense, not first

Protocols have to be role-specific. In healthcare the exposures split sharply — a floor nurse doing manual transfers faces a different injury profile than a home health aide driving between clients or an administrator at a desk. A one-size manual leaves the highest-risk roles under-protected.

Train Employees Effectively

Training sticks when it's specific and hands-on. A nurse who has physically practiced a two-person transfer with a gait belt retains it; one who watched a slideshow does not. Effective programs include:

- Safety-specific onboarding from day one for every new hire

- Role-specific content — transfer mechanics for caregivers, driving safety for mobile staff

- Regular refreshers, not an annual afterthought

- A clear, retaliation-free way to report hazards and near-misses

When staff feel safe raising concerns, small problems get caught before they become claims — and before they become the injury we have to manage.

Conduct Regular Safety Audits

Audits confirm protocols are actually being followed and that they still fit the operation. Run them with a dedicated safety officer, on a set schedule (quarterly at minimum in high-risk facilities), and document everything. Carriers weigh loss-control documentation heavily at renewal — a clean audit record is one of the more underused levers for holding premium down, and it's part of what earns access to the better program structures later in this guide.

Build an Efficient Claims Reporting and Investigation Process

This is the section the insurance company hopes you skim — because it's where their default behavior costs you the most, and where handling the claim yourself (or through an advocate) changes the outcome entirely.

Prioritize Prompt Injury Reporting

Delayed reporting is one of the most preventable cost drivers there is. NCCI research found median costs for sprain/strain injuries reported in week four ran 70% higher than those reported in week one, with attorney involvement climbing as the lag grows. Every day between the incident and the record is a day the story can drift.

Make reporting immediate: keep the process simple, train supervisors to act within minutes, and route every incident to your claims advocate the same day. In our model the call comes to us — we evaluate the incident on the spot and decide the next move.

Document and Investigate Thoroughly — Starting with a Day-One Medical Record

Here's a move most employers never make: when the incident warrants it, we send the injured worker to urgent care immediately. Not to be adversarial — to create an accurate, contemporaneous medical record while the facts are fresh.

That day-one record is your single best protection against later exaggeration. A back strain documented the afternoon it happened is very hard to reframe, months later, as a career-ending injury. The supervisor's job in those first hours is straightforward:

- Complete the incident report with specific facts, not vague descriptions

- Gather witness statements while memories are fresh

- Photograph the scene before anything changes

- Get the worker an appropriate, documented medical evaluation right away

Keep the investigation focused on facts and cause, never on blame. A worker who feels accused is a worker who calls a lawyer.

Lead the Claims Process — and Correct the "Lawyer Number"

Once a claim is reserved at a scary figure, everyone starts treating that figure as reality. It usually isn't. A claim carried on the books at $250,000 frequently reflects perhaps ~$30,000 in actual medical spend — and even that is paid incrementally as treatment happens, often on the order of $1,500–$2,000 a month, not written as a lump-sum check. Left unmanaged, the carrier prices to the scary number; managed properly, you pay the real one.

This is also where we draw a hard line between two very different claims. Genuine injuries get paid — promptly and without a fight. That's the job, and disputing a real injury is both wrong and expensive. But exaggerated or fraudulent claims get investigated and contested, because every inflated dollar hardens into your loss history and your future premium. Knowing which is which — and having the day-one record to prove it — is the whole game. (See our approach to fraud prevention and independent medical exams.)

Workers rarely lawyer up because they want a fight. They do it because they're scared — of losing their job, of being denied care, of a system they've never navigated. Early, genuine contact closes that gap: a supervisor check-in within 24 hours, help with appointment logistics, a get-well note. Done consistently, those small steps head off the attorney call before it's ever made. And because we're paid by commission from the insurer — not by how many claims you file or how much they cost — our incentive is simply to get the number right, not to churn.

Support Injured Workers and Accelerate Return to Work

Return-to-work is the highest-ROI tool an employer has, full stop. The moment an injured employee is back in a modified role, indemnity payments stop, the claim clock slows, and the worker stays connected to the job instead of drifting toward a lawyer.

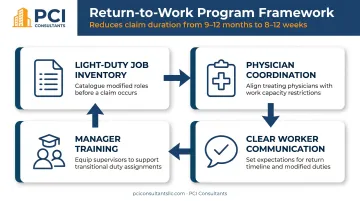

From Months to Weeks

A claim left to run its natural course can stretch nine to twelve months of lost time. A real return-to-work program compresses that to weeks. Take an injured nurse who can't safely lift or transfer: rather than sit home for months collecting wage replacement, she moves within weeks into a light-duty, receptionist-type role — greeting families, handling phones, coordinating schedules — while she recovers. The work is genuine, the paycheck continues, and the real claim cost drops sharply because you're no longer funding total lost time. Individual results vary, but the direction is reliable.

Key Elements of a Formal Program

- A documented light-duty inventory — specific, realistic modified roles by department, mapped in advance

- Physician coordination — match available duties to documented restrictions; don't guess

- Manager training — supervisors need to accommodate returning workers without creating new exposure

- Early, clear communication — lay out options before the worker assumes the worst

Modified duty doesn't have to mirror the original job — reception, scheduling, training-observer, chart audits, and phone-based coordination all count. For employers in high-deductible or loss-sensitive programs, every day of shortened duration is a dollar saved inside your own retained layer, so RTW design and claims cost are two sides of the same coin. We build these programs around each client's actual injury mix — nursing homes, home health and CDPAP agencies, hospitals.

Leverage Technology and Data to Monitor and Reduce Claims

Real-time claims oversight used to live only inside big carrier operations. Now it's how a competent advocate keeps a whole program honest — because the cost control is in the pattern, not the single file.

Active monitoring across your program surfaces what an individual examiner misses:

- Open claim count, status, and whether each reserve is realistic — or padded toward a "lawyer number" that hasn't been challenged

- Which units and classifications are generating frequency

- Early exaggeration and fraud signals: attorney-timing, treating-provider patterns, injury-mechanism inconsistencies, refusal of reasonable light duty

- Medical-only vs. lost-time conversion risk — a critical line, since medical-only claims carry far less weight in your e-mod

The point of watching is to act. A file flagged early for litigation risk or a runaway reserve gets redirected — more hands-on medical management, proactive employer contact, an independent medical exam, or a return-to-work push — while intervention still changes the outcome. Early visibility is also what gives carriers the confidence to extend the high-deductible structures that produce the biggest savings, because they can see the claims are being actively administered rather than left to run.

Structure Your Workers' Comp Insurance Program to Control Premium Costs

Even a spotless safety record can be structurally overpaying — because the kind of program you're in matters as much as your loss history.

Standard Guaranteed-Cost vs. High-Deductible Programs

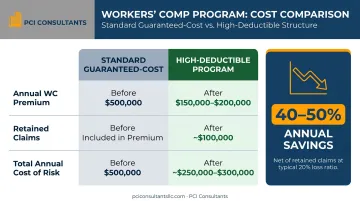

Under a standard guaranteed-cost policy, you pay a fully loaded premium upfront and the carrier absorbs every claim — including its margin, overhead, and worst-case assumptions, all baked into the rate whether or not the losses ever materialize. If your actual losses are low, that's a large, invisible overpayment.

A high-deductible program flips it: you retain a defined first layer of loss and the carrier covers everything above it. Because the carrier's projected outlay drops, so does your premium — often by roughly half. This is powerful, but it is not for everyone: not every business qualifies, and the structure only works when the retained layer is actively administered by someone managing every claim inside it.

How the Math Works

Say you're carrying a $500,000 guaranteed-cost premium and your real losses run modestly against it. Move to a high-deductible program where you take the first layer of each claim and the carrier covers the excess:

| Component | Guaranteed-Cost | High-Deductible |

|---|---|---|

| Annual WC Premium | $100,000 | ~$50,000 |

| Retained Claims (paid incrementally, e.g. ~$3,000/mo) | Included in premium | Paid only as claims occur, stop when the condition resolves |

| Who administers the claims | Carrier, at face value | Your brokerage, actively |

The key is that retained claims are paid as they happen, monthly, and stop the moment the condition resolves — you're funding real, current cost, not pre-paying the carrier for a worst case that may never arrive. For a qualifying employer with 100+ employees and $100,000+ in annual WC spend, this structure is worth modeling against your current premium. It has to be actively managed to work — which is precisely the claims-handling discipline described throughout this guide. Individual results vary.

Not sure you qualify, or whether the numbers work for your operation? That's exactly what a no-cost policy review is for.

Take the Next Step

If any of this describes your situation — climbing premiums, claims you suspect are inflated, or a nagging sense the carrier is running the show — the fastest way to find out what you're really paying is to let us look. To quote or take over your coverage we need two things: a copy of your current workers' comp policy and your five-year loss runs. From those we can show you where your money is going, what your real claim costs look like versus the reserved numbers, and whether a restructured program would cut your premium.

Send those over and we'll come back to you within 24 hours.

Frequently Asked Questions

What is risk management in workers' compensation?

It's the proactive work of preventing injuries and then actively managing every claim that does occur — so you control both how often claims happen and what each one really costs. The difference-maker is who handles the claim: left to the insurer, files tend to get paid near face value and closed. When your brokerage handles the claim directly, evaluating the incident on day one and paying genuine costs incrementally, the real number stays far below the reserved one — and your e-mod and premium follow.

What are the key risk management strategies for workers' comp claims?

Assess and correctly classify your workforce risk; put role-specific prevention and training in place; report and document injuries the day they happen (including an immediate medical record); manage each claim actively rather than handing it to the carrier; run a real return-to-work program; and structure the insurance program — up to and including a high-deductible layer for qualifying businesses — so you pay for your actual risk.

How does a day-one medical record protect my business?

When we evaluate an incident immediately and, where warranted, send the worker to urgent care right away, we create an accurate, contemporaneous record of the actual injury. That timely documentation is your strongest defense against a modest strain being reframed months later as something far larger — and it's the evidence that lets us pay genuine claims fast while contesting exaggerated ones.

What is the "lawyer number" and why does it matter?

It's the inflated figure a claim gets reserved or demanded at — say $250,000 — that rarely reflects reality. Actual medical spend on that same injury might be closer to $30,000, paid incrementally at roughly $1,500–$2,000 a month rather than as a lump sum. If no one challenges the inflated number, the carrier prices to it and it hardens into your loss history. Correcting it early is central to controlling long-term premium. Individual results vary.

What is a return-to-work program and how does it cut claim costs?

It brings an injured employee back in a modified, light-duty role during recovery — for example, an injured nurse moving into a receptionist-type position within weeks. Wage-replacement payments stop, the claim resolves faster, and the real cost drops sharply compared with months of total lost time. It also keeps the worker connected to the job, which meaningfully reduces the odds of litigation.

How do high-deductible workers' comp policies reduce premiums?

You retain a defined first layer of loss and the carrier covers the excess, which can roughly halve annual premium because the carrier's projected payout falls. Retained claims are paid incrementally as they occur and stop when the condition resolves, so you fund real cost instead of pre-paying a worst case. It only works when actively administered, and not every business qualifies — sweet spot is 100+ employees and $100,000+ in annual WC spend.