This matters most to mid-to-large healthcare employers: nursing homes, home health and CDPAP agencies, assisted living operators, and hospitals. These are the highest-injury-risk workplaces in the country, and their operators often suspect they're overpaying — because their real claim experience is better than what a standard rate assumes. A retro plan, in theory, rewards that performance directly.

Here's what the insurance company won't lead with: on a retro plan, your loss run is your premium. The formula is real, but it's not what decides whether you save money. How each claim gets handled does. This article covers how the plan actually works, what it costs, who genuinely benefits, and why the answer to "should we do this?" almost always comes down to who is managing your claims.

Key Takeaways

- You pay an estimated premium upfront, then settle a final premium based on the actual claims from that policy period.

- Minimum and maximum thresholds are guardrails that cap how far your cost can rise or fall.

- Incurred Loss Retro is more common and cheaper to set up; Paid Loss Retro improves cash flow but adds complexity.

- Every dollar booked into a claim flows straight into your final premium — so an inflated reserve or a slow return-to-work is a direct, calculable cost to you, not the insurer.

- Retro rewards stable, well-managed loss histories and punishes passive claims handling. Without an advocate fighting each claim, the structure works against you.

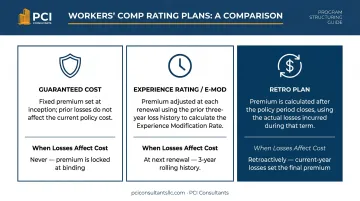

What Is a Retrospective Workers' Compensation Plan?

A retrospective (retro) workers' comp plan is a loss-sensitive rating program where your final premium is tied directly to the losses incurred during the current policy period. The premium isn't fixed at the start — it's calculated after the fact, once real claim data comes in.

How It Differs From Other Rating Approaches

Two comparisons show where a retro plan sits:

| Plan Type | How Premium Is Set | When Losses Affect Cost |

|---|---|---|

| Guaranteed cost | Fixed at inception; doesn't change | Never — same premium regardless of claims |

| Experience rating (E-Mod) | Adjusted each renewal on the prior 3 years of loss data | Future periods only |

| Retro plan | Calculated after the policy period ends | Current period — immediately |

A retro plan uses current-period losses to adjust the current-period premium. The cost consequence is immediate — not deferred to next year's renewal like an experience rating modification.

The Core Intent

The design logic is simple: align what you pay with the risk you actually represent. Clean year, premium drops. Bad year, you pay more. That direct link is supposed to reward good operators.

But here's the catch most brokers skip. Once a claim inflates your loss run, that number is sticky. Premiums that rise after a bad year rarely come all the way back down, even after the claim resolves — the elevated cost trails you across multiple years. So on a retro plan, letting a single exaggerated claim settle at face value isn't a one-time expense. It's a multi-year tax. That's exactly why direct, aggressive claims handling isn't a nice-to-have here — it's the whole game.

How a Retro Workers' Comp Plan Works

A retro plan runs in three phases: pay an estimated premium upfront, manage claims through the policy period, then recalculate what you actually owe on real loss data. Understanding each phase shows employers how much financial risk they're taking on — and where the savings actually live.

Step 1: Setting the Initial Standard Premium

At inception, the insurer sets a standard premium from estimated payroll, class codes, and projected losses. This is a working estimate, not the final number. One thing worth checking before you ever get here: how your payroll is classified. A nursing home that lumps clerical and billing staff into the same high-risk class code as hands-on floor nurses is overpaying on its lowest-risk people before a single claim is filed. Segmenting the workforce by actual risk is the first place we look, because it lowers the base the entire retro formula builds on.

Step 2: Calculating the Retro Premium

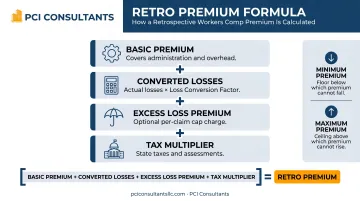

The retro premium formula, as supported by NJCRIB's rating manual, is:

(Basic Premium + Converted Losses + Excess Loss Premium + Retrospective Development Premium) × Tax Multiplier

A simplified version — (Basic Premium + Converted Losses) × Tax Multiplier — shows up often in practice, but the full formula can include optional elements depending on structure. Each piece does a specific job:

- Basic Premium — covers the insurer's administrative costs, loss control, and overhead; calculated by multiplying standard premium by a Basic Premium Factor.

- Converted Losses — your actual incurred losses multiplied by a Loss Conversion Factor to account for claim-adjusting expenses.

- Excess Loss Premium — an optional charge for a per-claim loss limitation, which caps your exposure on any single large claim.

- Tax Multiplier — covers state premium taxes and assessments.

Look at where the leverage sits: Converted Losses. That's your loss run, multiplied. Basic Premium and the Tax Multiplier are largely fixed once the plan is written. The one number you can actually move during the year is what gets booked into your claims — and that number is set less by what happened to the worker and more by how the claim is handled.

No matter what the formula produces, the final retro premium can't fall below the minimum (protecting the insurer) or exceed the maximum (protecting you). These contractually set thresholds define the exact boundaries of your financial exposure before the policy begins.

Step 3: The Adjustment Process

Retro adjustments don't happen once. According to NYCIRB, the first calculation uses loss data valued in the sixth month after policy expiration, with follow-up calculations at 12-month intervals after that.

The process continues until you and the carrier agree the calculation is final — which can take years if claims stay open. This is the part that quietly costs employers the most: a single claim carrying a $250,000 open reserve keeps re-entering your retro calculation, year after year, at that inflated "lawyer number" — even when the real medical spend is closer to $30,000, paid incrementally at roughly $1,500 to $2,000 a month. Left uncontested, that reserve doesn't just cost you once. It compounds across every adjustment cycle until someone forces it down to the supportable value.

Types of Retro Workers' Comp Plans

Incurred Loss Retro Plan

The most widely used type. Adjustments are based on total incurred losses — claims already paid plus open reserves on pending claims. IRMI defines it as a risk-financing plan where the insured pays a premium based on actual loss experience during the policy period.

Because open reserves count, this plan is uniquely sensitive to reserve accuracy. An adjuster's conservative $200,000 reserve on a soft-tissue back claim hits your premium the same as $200,000 actually paid out — until it's challenged and corrected.

Key characteristics:

- Lower cost to set up than paid loss plans.

- Aimed at employers with substantial premiums; NCCI's assigned-risk Loss Sensitive Rating Plan, for instance, applies at $250,000 or more in standard premium.

- Common in the voluntary market as well.

Paid Loss Retro Plan

Adjustments are based only on claims actually paid out — not reserves. You hold loss reserves in your own accounts until claims settle.

IRMI describes this as a cash-flow plan that lets the insured keep loss reserves until claims are actually paid. Working capital stays on your balance sheet longer instead of being pre-funded to the carrier.

Key characteristics:

- Cash-flow advantage: retained reserves stay with you until claims pay out.

- More complex and costlier to establish than incurred loss plans.

- Generally reserved for larger accounts with the administrative capacity to manage open reserves.

Both types are loss-sensitive cousins of the other alternatives to guaranteed-cost coverage, and the tradeoff between them is the starting point for evaluating which structure fits your risk profile.

The Pros and Cons of a Retro Workers' Comp Plan

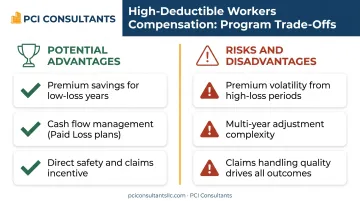

Potential Advantages

- Premium savings for well-managed employers. When actual claims land well below projected losses, the retro adjustment produces a refund or credit. Washington L&I confirms that retro participants can earn a partial refund by reducing injuries and lowering claim losses. How much you save depends on your loss experience relative to your minimum premium — and individual results vary.

- Cash flow management. Paid Loss plans let you keep reserves in-house until claims settle, preserving working capital that would otherwise sit with the carrier.

- A real, calculable safety and claims incentive. Every claim during the period has an immediate dollar impact on your final premium. That's what makes injury prevention and fast return-to-work programs financially consequential here — not just good practice.

Those upsides come with real exposure. Before committing, weigh three core risks.

Risks and Disadvantages

- Premium volatility. A period with higher-than-expected losses can produce a retro premium well above the initial estimate. This is the central financial risk of the structure — it's built into the formula, not a remote scenario.

- Complexity and long-tail obligations. Adjustments continue for years after the period ends. Finance teams unfamiliar with the mechanics get blindsided by billings that arrive on claims they thought were closed.

- Claims handling quality drives the entire outcome. Under a guaranteed-cost policy, a badly handled claim is the insurer's problem. Under a retro plan, it's yours. And here's what the insurer won't tell you: left to their own defaults, carriers tend to pay claims at or near face value and call it a "win." They're not incentivized to grind a $250,000 reserve down to its real $30,000 value — but on your retro plan, that gap is your money. Inflated reserves, slow return-to-work, and uncontested exaggeration compound across every adjustment cycle.

Who Is the Right Fit for a Retro Workers' Comp Plan?

The Ideal Retro Plan Candidate

Drawing on guidance from Sentry, retro plans work best for employers with:

- Large workers' comp premiums (our healthcare sweet spot starts around 100-plus employees and $100K-plus in annual spend) and a stable financial position.

- Consistent historical claims data that supports accurate loss projections.

- Better-than-average loss experience relative to industry peers.

- Active claims management — the resource that actually converts the structure into savings.

Industries That Commonly Benefit

Nursing homes, home health and CDPAP providers, assisted living operators, and staffing agencies placing nurses and aides routinely hit the conditions where retro can perform: high state-mandated premiums paired with operations that outperform actuarial projections. CDPAP fiscal intermediaries in particular pay steep premiums on a large Personal Assistant workforce while running low actual claim rates — exactly the spread a loss-sensitive structure can capture. Multi-location operators (say, several nursing homes under one owner) are often better served consolidating into a single master program for stronger terms before layering a retro or loss-sensitive structure on top.

When a Retro Plan Is the Wrong Choice

- Businesses with historically high or unpredictable claim frequency.

- Employers with no one actively managing claims — the structure will magnify every mishandled file.

- Newer operations without enough loss history for reliable projections (these are usually better grown into a loss-sensitive program over time).

- Employers who can't absorb a significant retrospective premium call.

The Claims Management Requirement — Where Retro Plans Are Won or Lost

Under a retro plan, claims management isn't optional — it's the mechanism that turns the structure into savings. This is where PCI Consultants' model differs from a traditional broker who sells you the policy and disappears. With 30-plus years doing this, we handle the claim directly for the life of the policy. When a worker is hurt, the call comes to us, not the insurer, and we go to work the same day:

- Day-one medical record. We evaluate the incident immediately and, where appropriate, send the injured worker straight to urgent care. That creates an accurate, timely medical record — the single best protection against a minor strain being exaggerated into a six-figure claim weeks later.

- Legitimate injuries paid without a fight. A genuinely injured aide or nurse gets their benefits, promptly. That's not just fair — it keeps claims from escalating into litigation. Individual results vary, but paid-fairly claims close faster and cheaper than contested ones.

- Exaggeration and fraud contested. When the injury mechanism doesn't match the medical picture, or an attorney and a $250,000 demand appear on day two, we investigate — fraud detection and prevention, AOE/COE work, surveillance, and Independent Medical Examinations — and drive the file toward denial or settlement at a supportable value.

- Return to work in weeks, not months. We move recovering staff into light-duty roles fast — an injured floor nurse into a receptionist-style or intake role within weeks — which cuts the real cost of the claim sharply and keeps the loss run clean.

- Reserve challenges before the cycle locks. We review reserve adequacy throughout each open claim and file documented challenges to inflated reserves before an adjustment period locks the number into your retro calculation.

And because we're paid by commission from the insurer — not tied to your claims volume — we're not incentivized to let a claim ride. Our whole reason to exist on your account is to drive that Converted Losses number down. See how our claims specialists work a file, and how we keep exaggerated claims from ever inflating your loss run.

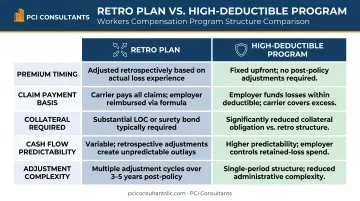

Comparing to High-Deductible Programs

Retro isn't the only loss-sensitive structure worth modeling. A high-deductible workers' comp program offers a similar incentive — cost tied to real loss performance — without the multi-year retrospective adjustment complexity.

| Dimension | Retro Plan | High-Deductible Program |

|---|---|---|

| Premium timing | Standard premium upfront; adjusted retrospectively | Significant reduction at day one |

| Claim payment basis | Retro premium calls tied to loss development | Paid monthly as claims run; payments stop when the condition resolves |

| Cash flow | Less predictable; calls can arrive years later | Retained dollars stay on your balance sheet |

| Adjustment complexity | Multi-year adjustment cycles | No retrospective adjustment process |

| Administration | Requires active in-house or brokered claims management | Actively administered by the brokerage |

Under a high-deductible program, the employer takes on a defined first layer — for example, the first $200,000 of a $500,000 tower — and the insurer covers the rest. For qualifying businesses, that structure can roughly halve the annual premium (say, from $100,000 to $50,000), with claim payments structured monthly (on the order of $3,000 a month) that stop once the condition resolves. It is not a fit for everyone — not every business qualifies — and it depends entirely on the brokerage actively administering the claims. But for a healthcare operator with strong safety practices and the cash position to hold a first layer, it can deliver the same reward as retro with far less multi-year uncertainty.

Your Next Step

Whether a retro plan, a high-deductible program, or a straight guaranteed-cost policy is right for you comes down to your actual numbers — and we can't tell from the outside which structure leaves money on the table. To model it, we need two things: a copy of your current workers' comp policy and your five-year loss runs. From those, our team reviews how your claims have really developed, where reserves are inflated, and what a directly-managed alternative would look like. Send those over and we'll come back within 24 hours with a straight read. Individual results vary, but the review costs you nothing.

Frequently Asked Questions

What is a retrospective workers' compensation policy?

It's a rating plan where your final premium is adjusted after the policy period to reflect your actual losses, rather than a fixed price set at inception. Unlike a guaranteed-cost policy, where the premium never changes no matter what claims come in, a retro policy creates a direct financial link between your loss experience and what you ultimately pay — which is why how each claim is handled matters so much.

Can you retroactively apply for workers' comp?

That's a different concept. A retroactive workers' comp claim is an injured worker filing for benefits after a delay, governed by state statutes of limitations (two years in New York and New Jersey; one year in Texas). It has nothing to do with the retrospective premium rating structure that affects your cost as the employer.

What's the difference between an incurred loss and paid loss retro plan?

Incurred loss plans adjust premiums on total losses including open reserves — so an inflated reserve costs you even before a dollar is paid. Paid loss plans count only claims actually paid out, which is friendlier to cash flow but more complex, and typically reserved for larger accounts. Either way, contesting reserves and closing claims quickly is what protects the final number.

How often is a retro workers' comp premium adjusted?

The first adjustment usually lands six months after policy expiration, with annual adjustments after that. The process continues until you and the carrier agree the calculation is final — which can stretch several years when claims stay open. That long tail is exactly why an inflated reserve, left uncorrected, compounds across cycle after cycle.

What are the minimum and maximum premiums in a retrospective rating plan?

They're contractually set thresholds defining the floor and ceiling of what you can be charged. Your retro premium can't drop below the minimum no matter how few claims occur, nor exceed the maximum no matter how many — protecting both sides from extreme outcomes. Knowing exactly where your maximum sits is essential before you sign.

Is a retro workers' comp plan the same as a high-deductible plan?

No. A retro plan adjusts your overall premium after the period ends based on aggregate loss experience. A high-deductible plan has you take on a defined per-claim or first-layer amount, with the insurer covering losses above it. They differ in cash-flow timing, collateral, and administrative complexity — and for qualifying businesses a directly-administered high-deductible program can capture similar savings with far less multi-year uncertainty. Not every business qualifies, so the right structure depends on your specific loss history and finances.