Introduction

Every New York employer subject to workers' compensation has their premium shaped by the NYCIRB Experience Rating Plan — yet most owners of nursing homes, home-health agencies, and hospital groups can't explain how the number is built or what they can actually do about it. The insurance company is not in a hurry to explain it to you either.

The experience modification factor (mod) is not an abstract stamp on your policy. It's a direct multiplier against your base premium. A mod of 1.25 adds 25% to your workers' comp cost. A mod of 0.80 saves you 20%. For a healthcare employer with 100-plus staff paying $300,000 or more a year, that spread is six figures — every year it stays there.

And here's the part that stings: in New York, once your premium climbs after a bad claim year, it rarely comes all the way back down, even after the claim resolves. So the mod isn't a one-year problem. It's a multi-year cost that follows you into every renewal. What follows breaks down exactly how the NYCIRB plan works, which factors move your mod, and where an actively managed claims process quietly changes the math.

Key Takeaways

- Your mod multiplies directly against manual premium — a debit mod above 1.0 raises cost, a credit mod below 1.0 lowers it

- The current formula is New Mod = (AP + EE) ÷ E: actual primary losses plus expected excess losses, divided by total expected losses

- Claim frequency hits your mod harder than one large loss — every claim contributes its full primary amount

- Open claims inflate your mod at their reserved value, which is often far more than the claim ends up costing to close

- New York left the NCCI interstate system on October 1, 2022 and now runs its own independent plan through NYCIRB

- The mod is won or lost at the claim level — how fast you report, treat, and close each injury

What Is the NYCIRB Experience Rating Plan?

The New York Compensation Insurance Rating Board (NYCIRB) is a non-profit association of carriers that files with the New York State Department of Financial Services. It's New York's independent rating organization, developing and administering the workers' comp rating plans for the state.

New York is not an NCCI state. Effective October 1, 2022, New York withdrew from the NCCI interstate experience rating system and implemented its own revised plan under the 2022 NYCIRB Experience Rating Plan Manual. For employers this matters: mod-reduction tactics built on NCCI methodology often don't translate to NYCIRB's rules.

What the Plan Actually Does

The plan adjusts your premium based on your actual loss performance versus what's expected for a company your size and industry. Strong loss history pays less; poor loss history pays more. Manual premium treats every nursing home in the same class code identically — the mod is what individualizes it. Two assisted-living operators with the same payroll and class code pay very different premiums if their three-year claims histories diverge.

Under NYCIRB's current rules:

- Who qualifies: all employers with New York exposure during the experience period are eligible for rating

- What it measures: actual losses vs. expected losses for the employer's size and class code

- What it produces: an experience mod applied directly to manual premium

- Time window: a three-year claims history, excluding the most recent policy year

The number is not destiny. It's a scoreboard — and the score is set by how each claim is handled long before the worksheet is calculated.

How the NYCIRB Experience Modification Factor Is Calculated

The Premium Formula

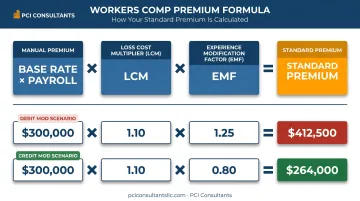

The standard premium formula is:

Manual Premium × Loss Cost Multiplier (LCM) × Experience Modification Factor (EMF) = Standard Premium

The LCM is set by the insurer. The EMF is calculated by NYCIRB. Both are multipliers, so a debit mod compounds: a 1.20 mod stacked on an already high LCM drives the standard premium sharply higher.

The Current Mod Formula (Post-October 1, 2022)

NYCIRB calculates the EMF using a specific formula. The revised version, effective October 1, 2022, is:

New Mod = (AP + EE) ÷ E

Where:

- AP = Actual Primary Losses (incurred losses up to the split point per claim)

- EE = Expected Excess Losses (total expected losses minus expected primary losses)

- E = Total Expected Losses (ELR × payroll ÷ 100 for payroll-based classifications)

The old formula's ballast, weighting values, and ratable excess didn't vanish — they're now baked into NYCIRB's published rating factors (tables of ELRs, split points, and D-ratios) instead of the formula itself. The single most controllable input is AP — actual primary losses — and that's exactly where hands-on claims work lives.

The Variable Split Point

The split point is the dollar threshold that divides each claim into a primary component (below the split) and an excess component (above it). Primary losses enter at full weight; excess losses are dampened. Under the current plan the split point scales with employer size based on expected losses, per NYCIRB's Table II. A small agency may sit at a few thousand dollars; a large multi-facility operator's split point is much higher.

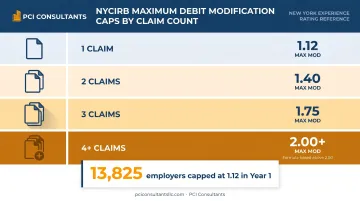

Maximum Debit Modification Caps

To stop a handful of claims from producing a runaway mod, NYCIRB caps the maximum debit by claim count:

| Claims in Experience Period | Maximum Debit Mod |

|---|---|

| 1 claim | 1.12 |

| 2 claims | 1.40 |

| 3 claims | 1.75 |

| 4 or more claims | 2 + (0.000003 × Expected Losses) |

These caps are real protection. NYCIRB's December 2024 Experience Rating Program Statistics report shows that in the first year under the revised plan, 13,825 employers with a single claim were capped at 1.12 — thousands of New York employers shielded from a worse outcome.

The Experience Period

NYCIRB uses three years of audited payrolls and reported losses. Officially, policies are included if their effective dates fall not less than 21 months and not more than 57 months before the rating effective date, with a maximum 45-month experience period. Add 3 months to the mod effective date, then capture policies effective in the resulting range (roughly 2 to 5 years back). NYCIRB refreshes ELRs, split points, and D-ratios annually, so always confirm you're on the current year's tables. This is exactly why we ask for five years of loss runs — it lets us see what's rolling on, what's rolling off, and which reserves are stale.

Key Factors That Drive Your Experience Mod Up or Down

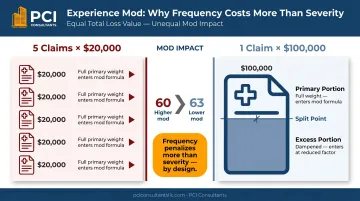

Frequency Beats Severity

This is the most counterintuitive feature of experience rating, and it has real consequences in healthcare, where lifting and transfer injuries are frequent. Because only the primary portion of each claim enters at full weight, one catastrophic claim contributes only its primary slice — the rest goes to excess. But multiple smaller claims each contribute their full primary amount. A home-health agency with five $20,000 strains is penalized more than one with a single $100,000 claim of the same total value. The plan weights frequency on purpose, to push prevention. The takeaway is blunt: every claim counts, and preventing even one small lost-time claim matters more than it looks.

Classification Codes and Expected Losses

NYCIRB assigns an Expected Loss Rate (ELR) to each class code; expected losses are ELR × payroll across the experience period. This is where risk classification pays off. Your clerical and administrative staff carry a fraction of the injury risk of your hands-on caregivers, and they should not be rated as if they were on the floor. When front-desk or billing payroll is misallocated to a nursing or aide code, or supervisors aren't separated from labor, the calculation inflates before a single claim is even filed — and you overpay on your lowest-risk people. Segmenting the workforce by actual risk is one of the first things we check.

Open Claims and Reserved Losses

NYCIRB defines actual incurred losses as paid losses plus outstanding reserves. An open claim enters the mod at its current reserved value — not what it finally costs. Here's the trap the insurer won't volunteer: a claim reserved at $80,000 that eventually settles for around $30,000 drags your mod at that inflated $80,000 for every year it sits open.

This is the "lawyer number" problem. A claim gets stamped as a "$250,000 claim," everyone treats that figure as gospel, and the mod is built on it — when the real medical spend might be closer to $30,000, paid out incrementally at roughly $1,500 to $2,000 a month, not as a lump sum. Left unmanaged, an insurer will often carry the fat reserve, pay near face value, and call it a win. The timing of claim closures matters as much as the final cost. Getting reserves right-sized and claims closed is a direct premium lever — and it's the core of our claims management work.

Industrial Code Rule 59

New York employers with annual payroll over $800,000 and a mod greater than 1.20 must participate in a formal safety and loss-prevention program under Industrial Code Rule 59. Requirements include:

- A DOL-certified consultant evaluation within 30 days of notice

- Completing the consultation within 75 days

- Submitting and completing a remedial action plan within 6 months

Non-compliance carries a 5% surcharge on manual premium, rising another 5% each subsequent year. Employers who treat Rule 59 as a framework rather than a fine tend to exit with documented loss-control controls that carry measurable mod impact at the next renewal.

How to Improve Your NYCIRB Experience Mod

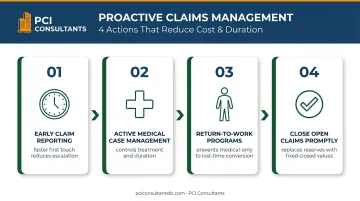

Proactive Claims Management

This is the highest-leverage work, and it's where a broker who actually handles the claim beats one who just places the policy. At PCI Consultants, the injured worker's employer calls us, not the insurer, for the life of the policy. When an incident happens, we evaluate it immediately — and often send the worker to urgent care that same day to create an accurate, timely medical record. That day-one record is what protects you later against an exaggerated version of events.

Specific actions that reduce actual primary losses (AP):

- Day-one reporting and evaluation — a fast, documented first touch reduces escalation and settlement values

- Active medical management — directs treatment and controls claim duration

- Return-to-work in weeks, not months — an injured nurse moved into a light-duty receptionist-type role keeps a claim from converting from medical-only to lost-time, which sharply cuts the real cost and the mod impact

- Closing open claims promptly — replaces an accruing reserve with a fixed, usually lower, closed value

For New York healthcare employers — nursing homes, home care, hospitals — this is where the mod is won or lost. Legitimate injuries get paid without a fight; that's not in question. Individual results vary, but the pattern is consistent: managed claims close smaller and faster.

Contest and Audit Questionable Claims

Genuine claims are paid without dispute. Exaggerated or fraudulent ones are a different story — and if nobody challenges them, they enter your experience period and inflate the mod unjustifiably. The tools include:

- AOE/COE investigation — disputes whether the injury arose out of and in the course of employment at all

- IME coordination — an independent medical exam challenging duration, severity, or disability rating

- Surveillance — for claims with return-to-work refusal or activity inconsistent with the claimed disability

- Reserve challenges — pushing the carrier to right-size reserves as claims age, so your mod isn't built on the lawyer number

Because we're paid by commission from the insurer and not by your claims volume, we're not incentivized to let a claim run. One inflated lost-time claim can carry downstream premium impact well beyond the claim cost across three renewal cycles — and remember, once premiums rise they rarely come back down. That's why early contestation and fraud prevention decisions are so consequential.

Review Your Experience Rating Worksheet

Errors in payroll, class codes, or reported losses can wrongly raise your mod — and NYCIRB allows corrections. Common errors:

- Clerical payroll misallocated to a higher-rated caregiver code

- Claims booked under the wrong classification

- Incorrect primary-loss split-point calculations

- Loss valuation errors using wrong reserve figures or dates

Request your worksheet from NYCIRB annually and verify every input. A single corrected error can lower the mod for all three years that figure stays in the experience period.

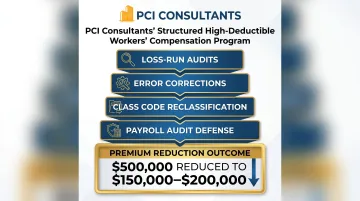

Structured Program Support

For larger New York employers, mod reduction and program restructuring amplify each other. PCI Consultants brings 30-plus years of NYCIRB-specific experience and, for qualifying businesses, structures high-deductible programs where the employer takes a defined first layer of risk and the insurer covers the rest. Set up well, that structure can roughly halve annual premium — think a $100,000 program moved toward $50,000 — with claim payments administered monthly (often around $3,000 a month) that stop when the condition resolves. Not every business qualifies, and we say so up front. Alongside it we run:

- Loss-run audits and open-claim closures

- Rating bureau error corrections

- Class-code reclassification by actual risk

- Payroll-audit defense

- Master-policy consolidation for owners running several facilities under one umbrella

Mod reduction is the slowest-moving lever, but it compounds the longest — an improvement stays embedded in the NYCIRB calculation for three consecutive policy years. Individual results vary.

Common Misconceptions About the NYCIRB Experience Rating Plan

"One large claim permanently destroys my mod."

Not accurate. The maximum debit caps (1.12 for one claim, 1.40 for two) limit how far a single severe claim can push the mod, and the claim rolls off the experience period after roughly three to four years. The caps exist precisely to keep an isolated incident from being catastrophic.

"My mod will improve automatically over time."

Only if new claims don't replace old ones. The rolling three-year window means a bad year stays in the math for up to four years before fully falling off — and if new claims land in the interim, the mod doesn't recover. Real improvement takes genuine frequency reduction and active management of open claims, not the passage of time.

"A 1.0 mod means we're doing fine."

A 1.0 mod is the statistical average for your industry — a baseline, not an achievement. NYCIRB's own data shows that of 450,389 mods issued in the first year under the revised plan, 400,254 were credit mods below 1.0. Most New York employers are already beating average. If you're sitting at 1.0, there's room — and pushing into the 0.70–0.90 range compounds year over year.

Frequently Asked Questions

What is the New York Compensation Insurance Rating Board (NYCIRB)?

NYCIRB is the independent rating organization authorized by the New York State Department of Financial Services to develop and administer workers' comp rating plans for New York. It calculates experience mods for eligible employers and operates separately from the NCCI system used by most other states.

What does a NYCIRB experience rating mean?

The experience rating (or mod) is a multiplier applied to your manual premium to reflect your actual claims history relative to expected losses for your size and industry. Above 1.0 increases premium; below 1.0 reduces it. Because it's built partly on open-claim reserves, how you manage claims in real time directly moves it.

What is a good NYCIRB workers' comp experience rating?

Any mod below 1.0 is a credit mod — better than average. A 1.0 is average. Employers with active claims management and disciplined loss control regularly land in the 0.70–0.90 range, which reduces standard premium by roughly 10–30%. Individual results vary.

How do I find my NYCIRB experience rating?

You can pull your experience rating worksheet from NYCIRB directly, or request it through your carrier or broker. It shows your payroll data, loss history, and the calculated mod used for your current policy. If you send us that worksheet along with your five-year loss runs, we'll audit every input for errors.

How does the NYCIRB experience rating affect my workers' comp premium?

It's a direct multiplier: Manual Premium × LCM × EMF = Standard Premium. A 1.25 mod raises standard premium 25% above base; a 0.85 mod cuts it 15%. On a $500,000 manual premium, a 0.10 mod improvement is about $50,000 a year — and because New York premiums rarely fall back once they rise, keeping the mod low protects you for years, not one renewal.

How long does it take to improve a bad NYCIRB experience modification factor?

Meaningful improvement usually takes two to three years of lower claims activity, since the mod draws on a rolling three-year window. But closing open claims, right-sizing over-reserved values off the lawyer number, contesting inflated losses, and correcting worksheet errors can start shifting the mod at the very next annual calculation. Individual results vary.

Your Next Step

If you run a New York healthcare operation paying six figures in workers' comp, the fastest way to know what your mod is really costing you is a review — not a sales pitch. Send us two things: a copy of your current workers' comp policy and your five-year loss runs. From there we'll check your worksheet for errors, flag any open claims sitting on inflated reserves, and tell you honestly whether a no-cost consultation leads to a high-deductible restructure, a mod-reduction plan, or both. Not every business qualifies for every program, and we'll tell you which fits yours.