Why Hospitality Businesses Pay More for Workers' Comp

Workers' compensation is one of the largest controllable operating costs a restaurant group, hotel, or event venue carries - and most operators are overpaying for coverage priced to their worst-case fears instead of their actual, managed risk.

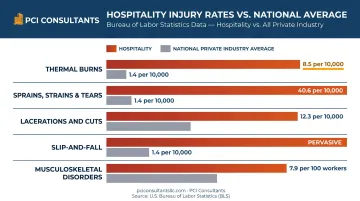

According to BLS data, accommodation and food services recorded 2.6 injury and illness cases per 100 full-time workers in 2024, above the all-private-industry rate of 2.3. Special food services hit 3.1 per 100 workers - well above the national benchmark.

Here's what the insurance company won't tell you: left on autopilot, a standard carrier tends to pay claims at or near face value, close the file, and call it a win. It isn't the carrier's job to talk a $250,000 reserve down to the roughly $30,000 the injury actually costs. That's the gap a hands-on brokerage lives in - and in a high-frequency industry like hospitality, that gap is enormous.

Structured programs - PEO arrangements and actively managed high-deductible arrangements - give operators a way out of the pricing trap through group-negotiated rates, direct claims handling, and premiums tied to real performance instead of a nervous underwriter's guess.

Key Takeaways

- Hospitality injury rates run above the national private-industry average, making workers' comp one of the sector's biggest and most controllable cost levers.

- High turnover compounds the problem - first-year employees account for 46% of all small-business injuries and 42% of claim costs.

- Who handles the claim matters more than the premium quote. When you call your broker instead of the carrier, incidents get evaluated the same day and inflated figures get corrected to real cost.

- Premiums are sticky: once a claim pushes your mod up, the higher premium rarely comes back down after the claim closes - it's a multi-year cost, which is why early claims control pays off.

- For qualifying multi-unit operators paying $100K+ in annual premium, a high-deductible program can roughly halve annual premium, with retained claims paid monthly as they age rather than pre-funded upfront.

The Unique Workers' Comp Challenges in Hospitality

An Injury Profile Unlike Other Industries

Hospitality workers face a specific, recurring set of injury exposures that drive claim frequency well above most other sectors:

- Thermal burns - BLS data shows special food services burn rates at 8.5 per 10,000 workers, more than four times the private-industry average of 1.4.

- Sprains, strains, and tears - 40.6 per 10,000 workers in special food services, driven by lifting, repetitive prep work, and housekeeping.

- Lacerations and cuts - 12.3 per 10,000 workers from knives and kitchen equipment.

- Slip-and-fall injuries - pervasive across wet kitchen floors, lobby areas, and banquet facilities, and the single most-abused category for exaggerated claims.

- Musculoskeletal disorders - hotel housekeepers had the highest injury rate among traveler-accommodation workers at 7.9 per 100 workers, with 77-91% reporting physical pain in the lower back, upper back, and shoulders.

Frequency matters as much as severity. A high volume of moderate claims drives the Experience Modification Rate (EMR) upward - and because premiums are sticky, an elevated mod compounds costs across the next three renewal cycles even after the underlying claims close.

The Turnover Problem

Accommodation and food services consistently post some of the highest separation rates in the U.S. economy, and that creates a compounding comp problem: newer employees are statistically more injury-prone, and constant churn prevents you from ever building a favorable mod. The cycle feeds itself:

- High turnover pushes claim frequency up.

- Elevated frequency inflates the mod.

- A higher mod raises renewal premiums - and they don't come back down.

- Higher premiums shrink the budget for the safety and light-duty programs that would break the cycle.

We cover this dynamic in depth in our breakdown of high-turnover restaurant staffing and premiums.

Tipped Employees and Payroll Complexity

Workers' comp premium is calculated on gross payroll. In most states tips are excluded from the remuneration base - but carrier auditors routinely mishandle tip income, overtime premium, and variable-hour math. End-of-year audit adjustments then blindside operators with premium they never owed. Overtime is a specific pain point: most states require only the straight-time equivalent of overtime hours in the payroll base, and auditors regularly fail to apply that cap. Part of managing a hospitality program is defending the audit so those inflated charges don't go unchallenged.

Seasonal and Multi-Location Complexity

Hotels, resorts, and venues staff up hard for peak season, spiking payroll in ways a standard annual policy handles badly. When audited payroll beats the up-front estimate, you owe more - sometimes a lot more.

Large operations also run many classifications - kitchen, housekeeping, front desk, security, maintenance - each with a different manual rate. This is where risk classification earns its keep. Your front-desk and administrative staff should not be rated like your line cooks and banquet crew. Misclassification quietly inflates premium for years, and correcting it - moving genuinely low-risk clerical roles off high-risk codes - often frees up real money before any claims work even starts. Owners running several properties can frequently consolidate multiple locations under one master program for better terms than each site could negotiate alone.

How PEO Workers' Compensation Works for Hospitality Employers

The Co-Employment Model

Under a PEO arrangement, you keep full operational control of your staff while the PEO takes on employer-of-record duties for payroll, compliance, and comp coverage. You access the PEO's master policy instead of maintaining a standalone one, which means group-negotiated rates and consolidated claims administration.

NAPEO reports roughly 500 PEOs operate in the U.S., serving more than 200,000 businesses and covering 4.5 million employees; about 14% of employers with 20-499 employees currently use one.

For operators, the model offers three concrete benefits: no standalone policy to renew independently, premium calculated on actual wages rather than a single annual estimate, and claims handled through the program rather than left to a standalone carrier examiner who has no reason to fight your corner.

Pay-As-You-Go Billing

Standard annual policies want a large upfront deposit based on estimated payroll - a rough guess for anyone with seasonal staff or variable hours. Pay-as-you-go ties premium to each payroll cycle on actual wages paid. For hospitality that kills two pain points at once: no year-end true-up shock when real payroll exceeds the estimate, and no big deposit tying up cash you need for the next season.

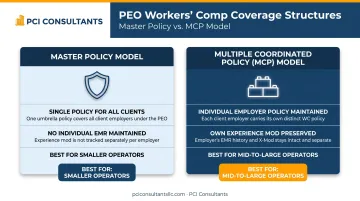

Types of Coverage Structures Available

Master Policy Model - all client employees sit under the PEO's single policy. Simpler to administer, but your own experience modifier isn't maintained or transferred. Generally better for smaller or newer operators who don't yet have a favorable mod to protect - the kind of business we grow into a stronger, standalone footing over time.

Multiple Coordinated Policy (MCP) Model - each employer keeps its own policy and experience mod under the PEO umbrella. Better for mid-sized and larger operators who've invested in safety and want to preserve and build a competitive mod.

High-Deductible Programs: The Advanced Option

For qualifying multi-unit operators, a high-deductible program is usually the biggest premium reduction on the table. The carrier issues a standard policy with a defined first layer you retain - for example, you take the first $200,000 of a $500,000 program and the insurer covers the rest. Because the carrier's projected outlay drops, underwriting premium falls sharply at inception; an operator paying roughly $100,000 can often move to something closer to $50,000.

The part most brokers gloss over is how the retained layer is actually paid. You do not hand over a lump sum. Claims are paid incrementally as they age - often on the order of a few thousand dollars a month per open claim - and those payments stop when the condition resolves. That structure only works if someone is actively administering each claim, which is exactly the point of the arrangement. Not every business qualifies, and individual results vary, but for the right operator the cash-flow improvement rivals the premium savings. See our deeper explainer on large-deductible workers' comp.

This model rewards operators who invest in active claims control, and it fits hospitality's high-frequency, moderate-severity profile especially well, because most individual claims fall well below the retained deductible layer.

Key Benefits of PEO Workers' Comp for Hospitality Businesses

Direct Claims Handling - You Call Us, Not the Carrier

This is the difference that shows up in your loss runs. When a line cook burns a hand or a housekeeper reports a back strain, you call us, not the insurer. We evaluate the incident immediately and, when it's warranted, send the worker to urgent care that same day to create an accurate, timely medical record. That record is what protects you weeks later when a modest injury gets described as something far worse.

We pay genuine injuries without dispute - that's the job, and legitimate workers get taken care of. But we correct the "lawyer number." A claim positioned as $250,000 frequently carries something like $30,000 of real medical cost, paid incrementally rather than as a lump sum. Left to a standalone carrier, the reserve tends to stand and the premium impact with it. Our revenue comes from commission paid by the insurer, not from your claim volume, so we're not incentivized to let claims run.

Faster Return to Work

Every week an injured employee sits fully out of work is real claim cost accumulating against your mod. Light-duty transitions move people back into modified roles within weeks - a kitchen worker on a lifting restriction into a host or expediter role, for instance - which sharply cuts the real cost of the claim. A structured return-to-work program is one of the highest-leverage tools in hospitality, where the injuries are frequent but most are recoverable.

A+ Rated Carrier Coverage

Quality programs place coverage with top-rated insurers. Travelers, for example, carries an AM Best Financial Strength Rating of A++ (Superior). For a regional restaurant group or hotel operator, accessing that carrier paper independently would require scale and underwriting relationships most mid-sized operators simply don't have.

Fraud and Exaggeration Detection

Slip-and-fall is hospitality's most-abused claim type, and workers' comp fraud feeds a roughly $30 billion annual insurance fraud problem. A single exaggerated lost-time claim settling at $150,000 can carry a downstream mod impact exceeding $100,000 in renewal premium over three years, on top of the direct cost - and remember, that premium is sticky. Genuine claims get paid; exaggerated or fraudulent ones get investigated and contested using surveillance coordination, AOE/COE investigation, and IME-driven disposition. Our fraud prevention work is about protecting your loss history and your future premiums, not fighting hurt employees.

Compliance Across Jurisdictions

Multi-location operators face different rules in every state. A well-run program handles state-specific coverage, correct class codes, audit documentation, and filings, coordinating with the independent rating bureaus - NYCIRB (New York), WCIRB (California), NJCRIB (New Jersey), PCRB (Pennsylvania) - where class-code differentials and credibility weighting vary significantly from NCCI states.

Safety and Loss Control at the Source

The most effective loss control in hospitality is operational: find where and why injuries actually happen - the un-matted prep station, the overloaded linen cart - and fix the condition, rather than delivering generic OSHA slides. Cutting frequency at the source is what moves the mod in the right direction over the following three policy years.

How to Evaluate and Choose the Right Program

Key Questions to Ask Any Provider

- When there's an incident, do I call the program or the carrier - and who decides on urgent care, reserves, and disputes?

- Will I retain and build my own experience modifier, or is it absorbed into a master policy?

- Is claims management handled directly, or outsourced to a third-party examiner pool with no stake in my outcome?

- Does the program actively investigate exaggerated and fraudulent claims - surveillance, AOE/COE, IME coordination?

- Are high-deductible options available that match my risk profile and cash flow, and how is the retained layer paid?

- Can the program handle hospitality class codes, tip income, overtime, and seasonal payroll at audit?

Provider Experience in Hospitality Matters

Generic programs miss the industry-specific injury patterns that actually drive cost in restaurants and hotels. PCI Consultants has administered workers' comp programs for 30+ years, with a hospitality program built for multi-unit restaurant operators, hotel and resort operators, management companies, and franchisees. The service stack runs from high-deductible placement on A+ rated paper to direct claims handling with triage tuned to hospitality injuries, class-code reclassification and payroll audit defense, mod-reduction work, and return-to-work design across multiple locations.

Understand the Full Program Economics

The premium line isn't the only number. Before you commit, review how the deductible is structured and funded, whether retained claims are paid over time on a "paid" basis or pre-funded upfront, cash-flow impact across the full term, and any collateral or letter-of-credit requirements. The best programs keep retained claim dollars on your balance sheet until actual disbursements are due - on thin hospitality margins, that cash-flow gain is often as valuable as the premium cut. The typical qualifying threshold is 100+ combined employees and $100,000+ in annual premium; not every business qualifies, and individual results vary.

The Concrete Next Step

We don't need a long questionnaire to tell you whether a switch makes sense. Send us two things: a copy of your current workers' comp policy and your five-year loss runs. That's enough for us to read your actual claims history, spot misclassified payroll and inflated reserves, and model whether a PEO, a high-deductible structure, or a re-rated standard program fits your operation. We respond within 24 hours.

Frequently Asked Questions

What services do professional employer organizations provide?

PEOs handle payroll processing, tax filings, benefits administration, workers' comp insurance and claims management, HR compliance, and safety programs through a co-employment arrangement where the PEO takes on employer-of-record duties while you keep operational control. The piece worth scrutinizing is claims: whether they're actively managed on your behalf or simply passed to a carrier examiner.

What companies are exempt from workers' compensation?

Exemption rules vary by state. Most employers with even one employee must carry coverage. Common exemptions may reach sole proprietors, certain independent contractors, or very small employers in specific states - but hospitality businesses with staff are almost always required to carry workers' comp regardless of size.

Can a PEO reduce workers' compensation costs for hospitality businesses?

Yes, through group-negotiated rates, active claims management, fraud and exaggeration detection, and safety programs. The largest savings come from actively managed high-deductible structures for qualifying operators with below-average, well-managed loss histories. Not every business qualifies, and individual results vary - the real driver is who controls the claim, because insurers left alone tend to pay near face value and move on.

What are the most common workers' comp injuries in hospitality?

Slip-and-fall accidents, musculoskeletal injuries from lifting and repetitive motion, kitchen burns and lacerations, and back-of-house equipment injuries lead the list. Housekeeping and banquet operations carry particularly elevated rates from room turns, heavy linen handling, and event setup. Most are genuine and recoverable, which is exactly why fast urgent-care documentation and light-duty return-to-work matter so much.

How does high employee turnover in hospitality affect premiums?

High turnover raises claim frequency because newer employees are statistically more injury-prone, and it prevents you from building a favorable mod - both compound into premium increases across three consecutive renewals. And because premiums are sticky, those increases don't reverse when the claims close, so controlling frequency early is what protects the number.

What should hospitality employers look for in a program?

Prioritize direct claims handling where you call the program and not the carrier; active fraud and exaggeration detection; A+ rated carrier coverage; hospitality class-code expertise with tip and overtime audit defense; and flexible structures such as high-deductible options matched to your cash flow. To get a real read, send your current policy and five-year loss runs for review.