The honest answer is that it depends on two things: whether you have anyone working under you, and what the companies you contract with demand. But there is a second question the insurance company will never raise, and it matters just as much: if you do get hurt, who is going to manage that claim so it protects you instead of quietly draining you for years?

This guide breaks down the legal rules, the situations where coverage is effectively mandatory to win work, and the real financial mechanics of a policy for a one-person business, including the parts most articles skip.

TL;DR: Do Sole Proprietors Need Workers' Comp?

- Legally, often no if you have zero employees, most states do not require you to buy workers' comp for yourself.

- Practically, often yes. Many clients, agencies, and general contractors require it in writing before you can start work.

- Hiring even one person (part-time, full-time, or temporary) almost always triggers a legal requirement to carry coverage.

- A policy protects your personal finances if you are injured, but only if it is structured and managed correctly, not just purchased and filed away.

The Legal Requirement for Sole Proprietors: It Depends on Your Team

In most states, a sole proprietor with zero employees is not legally required to buy workers' compensation for themselves. The system was built to protect employees, not owners. That changes the moment you bring anyone else on.

If You Have Employees, the Answer Is Almost Always "Yes"

The moment you hire your first worker, whether full-time, part-time, or temporary, the rules flip. State law almost universally requires you to carry a policy covering them.

Failing to do so carries penalties that can end a small business:

- Hefty Fines: In California, going without workers' comp is a misdemeanor punishable by a fine of at least $10,000.

- Daily Penalties: Florida can issue a stop-work order and stack a $1,000 per day penalty on top.

- Criminal Charges: In New York, failing to secure coverage for more than five employees can be a felony, with fines from $5,000 to $50,000.

The Gray Area: Independent Contractors vs. Employees

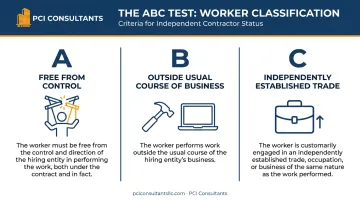

Some owners try to sidestep this by paying workers as 1099 independent contractors instead of W-2 employees. This is a dangerous gray area. States apply strict criteria, like California's ABC test, to determine a worker's true status, and the 1099 does not settle the question.

To be a genuine independent contractor, a worker generally must be free from your control, perform work outside the usual course of your business, and be independently established in their trade. If you misclassify an employee as a contractor and they get hurt, regulators will likely treat them as your employee, leaving you on the hook for the injury and the non-compliance penalties. If contractors are a regular part of how you operate, it is worth reading more on why independent contractors are generally not covered and how employers get disputes wrong.

When Workers' Comp Is Optional But Highly Recommended

Even with no employees and no legal mandate, you will often find you need a policy to operate and grow. Here are the most common scenarios.

Your Client, Agency, or General Contractor Requires It

This is the number one reason sole proprietors without employees buy workers' comp. Agencies, facilities, and general contractors almost always require proof of insurance before they hand you a contract.

They do it to protect themselves from the "liability chain." If you, an uninsured contractor, get hurt on their site or in their client's home, that liability can roll up to them and their policy, and their premium is what takes the hit. To avoid that risk and the premium increases that follow, they push the insurance requirement down to everyone working under them.

Actionable advice: Always review contracts for insurance clauses before you sign, and do not wait until the week you start to go looking for a policy.

You Work in a High-Risk Field

If your work is physical, the risk of a serious injury is real, and for a one-person operation a single accident can be financially devastating. Home health and personal care is a clear example: aides and independent caregivers lift, transfer, and reposition clients all day, and a back or shoulder injury can put you out of work for weeks.

The healthcare and social assistance sector reports some of the highest musculoskeletal injury rates of any industry, per the U.S. Bureau of Labor Statistics. Other high-risk fields where a sole proprietor should think hard about coverage include:

- Home health, personal care, and CDPAP-style caregiving

- Construction and the trades (plumbing, electrical, roofing)

- Trucking and transportation

- Landscaping and tree service

- Auto repair and warehousing

Without coverage, you are personally responsible for 100% of your medical bills and left with no income while you recover. With the right coverage, the story is very different, and the difference is mostly in how the claim gets handled, which we will come back to.

Your State Requires It for Professional Licensing

In some states you cannot get or keep a professional license without proof of workers' comp, even as a one-person shop. The California Contractors State License Board (CSLB), for example, requires licensed contractors to keep a policy on file. This is becoming more common. Before you apply or renew, check your state's licensing board so a lapse does not cost you the license.

What a Policy Actually Does, and What the Insurer Will Not Tell You

Thinking of workers' comp as just another bill is a mistake. For a sole proprietor it is a safety net around your single most valuable asset: your ability to earn. Here is what a properly structured policy does.

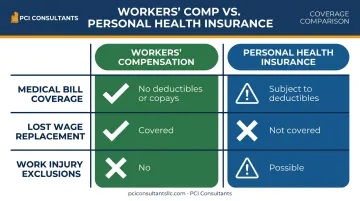

- Covers medical expenses in full. If you are hurt on the job, workers' comp pays the ambulance, the ER, surgery, prescriptions, and physical therapy, typically with no deductible or co-pay for a work-related injury.

- Replaces lost wages. This is the benefit personal health insurance never provides. If an injury keeps you out for weeks, workers' comp replaces a portion of your income so you can still cover your living costs.

Now the part the insurance company will not volunteer. When you file a claim, the carrier's default move is to open it with a reserve set at a worst-case "lawyer number." We routinely see a soft-tissue injury reserved at something like $250,000 when the real, properly managed medical spend is closer to $30,000, and it is paid incrementally, often around $1,500 to $2,000 a month, not as one lump sum. Left to run on autopilot, an insurer will frequently pay at or near that inflated figure and call it a win, because it is not their premium that goes up afterward. It is yours. And once a claim inflates your rating and pushes your premium up, that increase rarely comes back down after the claim closes. You can pay for a single mishandled injury for years.

That is the whole argument for active claims management over just holding a policy. When claims are handled directly, the injured person, you, gets to urgent care immediately so there is an accurate, timely medical record from day one, and light-duty options get lined up so you are back to safe, productive work in weeks rather than months. Individual results vary, but the pattern is consistent.

How to Secure Workers' Comp as a Sole Proprietor

As the owner, you have to take specific steps so your policy actually covers you, not just future hires.

Electing for Self-Coverage

A workers' comp policy bought by a sole proprietor is often set up by default to cover only future employees. You must specifically "elect" to include yourself, the owner, on the policy. Skip that step and the policy may satisfy a contract requirement while paying nothing for your own medical bills or lost wages if you get hurt.

This is the key difference from a "ghost policy", a minimum-premium plan bought only to produce a certificate of insurance for a general contractor or agency. Ghost policies are written on the understanding that there are no employees and explicitly exclude the owner. They are cheap, and they offer you zero personal injury protection. If your goal is real protection, elect yourself in and read the fine print.

Finding the Right Partner, Not Just the Right Price

Anyone can sell you a policy. What actually determines your cost over time is how your work is classified and how claims get managed. A specialist will segment your work by actual risk, so if you split your time between hands-on care and clerical or scheduling work, you are not rated as if every hour is high-risk. That alone can pull real dollars out of your premium.

More importantly, the right partner handles the claim directly for the life of the policy: you call them, not the insurer. Legitimate injuries get paid without a fight; exaggerated or fraudulent ones get investigated and contested. That distinction protects your loss history, which is what your future premiums are built on.

Navigate Complex Workers' Comp Needs with an Expert Partner

For sole proprietors in high-risk or niche fields, like CDPAP and other home health care work, juggling state mandates, agency requirements, and pricing can be overwhelming. Standard policies often carry premiums that do not reflect your actual risk or claims history, quietly draining cash flow.

This is where an experienced consultant changes the math. At PCI Consultants, with 30-plus years in workers' compensation, we do two things most brokers do not:

- We manage the claim, not just the policy. When you are hurt, you call us. We evaluate the incident right away, build the medical record early, and push for a fast, safe return to work. Because we are paid by commission from the insurer and not by how many claims run through, we are not incentivized to let your claim balloon.

- We structure programs to fit your real exposure. For qualifying businesses, that can include higher-deductible and alternative arrangements where you take on a defined first layer of risk and the insurer covers the rest, actively administered by us. Not every business qualifies, and individual results vary, but for the ones that do it can meaningfully lower annual premium. You can also grow into better terms over time as your business scales.

The concrete next step is simple. Send us two things: a copy of your current workers' comp policy and your five-year loss runs. We will review how you are classified, whether your premium reflects your real risk, and whether any open claim is being managed or just paid, and get back to you within 24 hours.

Frequently Asked Questions

Do sole proprietors need workers' comp insurance?

Legally, you generally only need it once you have employees. In practice you will often need a policy anyway to win contracts with larger companies and agencies, to hold a professional license, or to protect your own finances if you are hurt while working. The better question is not just whether you are required to carry it, but whether the policy actually covers you and who will manage the claim if you get injured.

How much does workers' comp cost for a sole proprietor?

Cost depends on your state, your industry's risk classification code, and your declared payroll. But the sticker price is only half the picture, how your work is classified and how claims are handled drive your real long-term cost far more than the initial quote. A specialist can classify your roles accurately so you are not overpaying on low-risk hours, and give you a realistic number for your situation.

What happens if I am a sole proprietor without employees and get injured on the job?

Without a policy that specifically includes you, you are personally responsible for all your medical bills and have no way to replace lost income while you cannot work. With a policy that elects you in and is actively managed, you get to care quickly, an accurate medical record is built from day one, and you are guided back to safe, light-duty work sooner. Individual results vary.

Can I use my personal health insurance for a work-related injury?

It is a risky bet. Many personal health plans exclude work-related injuries outright, and none of them replace your lost wages. Workers' comp is the only coverage built specifically for on-the-job injuries, which is exactly why agencies and general contractors ask for it rather than accepting your health plan.

What is a workers' comp "ghost policy"?

A ghost policy is a low-cost workers' comp policy bought by a sole proprietor with no employees, used only to show proof of insurance for a contract. It provides no injury benefits for the owner. If you want actual protection for yourself, you have to elect owner coverage, which a ghost policy specifically excludes.

Why does one claim raise my premium for years?

Because premiums are built on your loss history, and once a claim inflates your experience rating, that increase rarely reverses after the claim resolves. The carrier's default is to reserve and pay claims near an inflated "lawyer number" rather than minimize them, since it is your premium, not theirs, that rises. That is why managing the claim from day one, paying legitimate injuries fairly while contesting exaggerated ones, matters more than the price on the policy. Individual results vary.

Not Sure Your Policy Actually Covers You? Let's Look.

The fastest way to know whether you are truly protected, whether your premium reflects your real risk, and whether any open claim is being managed or just paid, is a policy review. Send us a copy of your current workers' comp policy and your five-year loss runs. We will tell you where your exposure actually sits and what it would take to bring your cost down. Not every business qualifies for every program, and individual results vary, but the review itself costs you nothing but the paperwork.