Here is what the insurance company won't tell you: left to their own defaults, carriers tend to pay claims at or near face value and call it a "win." It's not their money that gets tied up in a nursing home's inflated loss run for the next three years — it's yours, in the form of premium that rarely comes back down. This article lays out how premium reduction actually converts into ROI, and why the biggest lever is not a cheaper quote but active, direct claims management.

TL;DR: How Premium Reduction Turns Into ROI

- The premium follows the claims. Lower, accurately-valued losses today lower your rate for years — not just this renewal.

- Handling beats shopping. A brokerage that takes the claim directly, builds a day-one medical record, and pushes fast return-to-work drives down real claim cost far more than swapping carriers.

- The "$250,000 claim" is usually a fiction. Real medical spend is often a fraction of the reserve, paid incrementally — but only if someone contests the inflated number.

- Structure is the second lever. For qualifying businesses, a high-deductible program can roughly halve annual premium and keep capital in your accounts.

Beyond the Bill: How High Premiums Quietly Erode Your Bottom Line

The obvious cost of workers' comp is the check you write at renewal. The real damage runs deeper, and it compounds.

- Premium stickiness. This is the one that hurts. Once a bad claim hits your loss run and your rate goes up, it rarely comes back down — even after the claim closes. A single exaggerated back injury at a nursing home can quietly ride your premium for three to five years. That means the ROI of getting a claim valued correctly the first time is a multi-year return, not a one-time saving.

- Stifled growth (opportunity cost). Every dollar overspent on comp is a dollar not spent on hiring nurses, opening a new location, or upgrading patient-lift equipment. For a healthcare employer running thin margins, tying up capital in an oversized premium is a real constraint on growth.

- Competitive disadvantage. High overhead forces you to accept thinner margins or raise rates, while a leaner competitor with a cleaner loss run underbids you on contracts and referral relationships.

The throughline: your premium is a lagging indicator of how your claims were handled. Fix the handling and the premium follows — which is exactly where the return comes from. If you want the deeper mechanics of why rates climb after an incident, see does workers' comp go up after a claim.

Connecting the Dots: How Premium Reduction Directly Boosts ROI

The return on your risk-management effort comes down to a simple relationship:

ROI = (Net Savings & Gains) / (Cost of Actively Managing Risk)

When you lower your comp cost the right way — by controlling claims rather than just re-shopping the policy — the savings show up in several places at once.

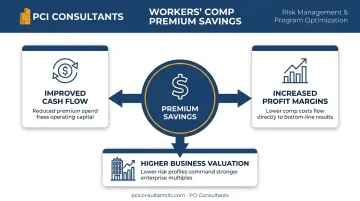

Improved Cash Flow

The money you no longer send to a carrier is instantly available for payroll, debt, or a time-sensitive opportunity. And when claims are structured to be paid incrementally — often around $1,500 to $2,000 a month for a typical injury rather than a lump sum — you keep working capital in your own accounts instead of pre-funding a reserve the insurer set too high. That financial flexibility is the most immediate piece of the return.

Increased Profit Margins

Workers' comp is a fixed-looking operating expense, so every dollar you cut drops straight to the bottom line. For a 300-bed senior care operator, shaving even 30% off a $200K premium is $60K of pure margin recovered without selling a single additional bed-day.

Higher Business Valuation

A healthcare operation with a controlled loss history and predictable comp costs reads as lower-risk to buyers and lenders. It signals strong internal controls and stable EBITDA. A safer, better-managed business isn't just cheaper to run — it's worth more when you sell or refinance.

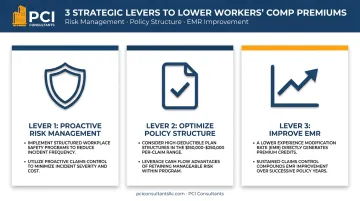

3 Strategic Levers to Lower Workers' Comp Premiums and Drive ROI

Reducing premium isn't about finding a cheaper plan. It's about becoming — and provably documenting that you are — a lower-cost risk. Here are the three levers that actually move the number.

Lever 1: Direct Claims Management (the biggest lever)

Most premium waste is decided in the first 48 hours of a claim, and most employers aren't in the room. With a self-service carrier, a caregiver reports a strained back, the adjuster opens a reserve at a worst-case number, and that number — the "lawyer number" — lands on your loss run whether or not the injury is that serious.

We do it the opposite way. At PCI Consultants, the injured worker's supervisor calls us, not the insurer, and we handle the claim directly for the life of the policy. That changes the economics in a few concrete ways:

- Day-one medical record. When an incident is reported, we may send the worker to urgent care immediately to create an accurate, timely, objective record of the actual injury. That record is what protects you when a minor strain gets described as a career-ending disability six weeks later.

- Correcting the "lawyer number." A claim presented as "$250,000" often carries maybe ~$30,000 in real medical spend, paid out incrementally at roughly $1,500–$2,000 a month — not as a lump sum. Left unchallenged, the inflated reserve is what your future premium gets priced against. Someone has to contest it.

- Genuine vs. exaggerated. Real injuries get paid promptly and without a fight — that's the point of coverage, and it keeps your staff whole and loyal. Exaggerated or fraudulent claims get investigated and contested, which protects your loss history and your future rate.

- Fast, light-duty return-to-work. Getting an injured nurse into a receptionist-style, light-duty role within weeks — instead of leaving them out on full indemnity — sharply cuts the real cost of the claim. A structured return-to-work program is one of the most reliable levers on the whole loss run.

Because we're paid by commission from the insurer — not by how many claims run or how much they cost — we're not incentivized to let a claim balloon. Our interest is a clean loss run, because that's what keeps your renewal defensible. If you want the full picture of what direct claims management covers, that's the engine behind every number on this page. Individual results vary.

Lever 2: Optimizing Your Policy Structure

Once your claims are being handled tightly, structure becomes the second lever. For a healthcare employer with a solid, actively-managed loss record, a high-deductible program can be a major win — though not every business qualifies.

The idea: you take on a defined first layer of loss — say the first $200,000 of a $500,000 program — and the carrier covers everything above it. In exchange, your annual premium can drop substantially, sometimes roughly in half (for example, from about $100K down to around $50K for a qualifying operator). Claims inside your layer are paid incrementally — often on the order of ~$3,000 a month — and those payments stop when the condition resolves, which is another reason active administration matters so much. We administer that layer for you; you don't self-adjust it.

This is powerful precisely because it's paired with Lever 1. A high deductible only makes sense when someone is aggressively managing what lands in your retained layer. You can go deeper on the mechanics in our guide to large-deductible workers' comp. Individual results vary, and qualification depends on your size, loss history, and cash position.

Lever 3: Getting Your Risk Classified — and Rated — Correctly

The third lever is making sure you're not overpaying on the payroll you already have. Your premium is driven by your experience rating and by how each role is classified.

- Risk classification. Your workforce should be segmented by actual risk. A billing clerk or receptionist at a nursing home is a clerical exposure and should be rated as one — not lumped in with hands-on caregivers who lift and transfer patients. Mis-classified clerical payroll is one of the most common ways employers quietly overpay.

- Experience rating. Your experience modification factor is essentially a credit score for your losses — below 1.0 earns a credit, above 1.0 a surcharge. Levers 1 and 2 are what move it over time, because a clean, accurately-valued loss run is what feeds the experience rating calculation.

- Consolidation and scaling. If you own several facilities — say a handful of nursing homes under one entity — consolidating them under a single master policy can unlock better terms than each buying separately. Smaller or newer operations can be grown into stronger programs over time.

Calculating the Full ROI of Managed Workers' Comp

The true financial impact goes well beyond the first renewal's savings. To see the real return, account for both direct and indirect gains — and remember the multi-year effect of premium stickiness.

Direct Savings

The straightforward part: your old premium minus your new premium, minus what you invest in active management.

Formula: (Old Premium − New Premium) − (Cost of Managed Risk Program) = Direct Savings

But because a corrected, lower loss run keeps your rate down for years — not just one cycle — the honest ROI multiplies that annual figure across the life the inflated claim would have haunted your renewals.

Indirect Financial Gains

The hidden value shows up as:

- Lower administrative burden — you call one number and we run the claim, instead of your HR staff fighting adjusters.

- Higher productivity — fast light-duty return-to-work means fewer lost caregiver-days on a floor that's already short-staffed.

- Avoided replacement costs — keeping an experienced nurse on light duty beats recruiting and training a replacement.

- Protected loss history — every exaggerated claim you don't let inflate is premium you don't pay for years.

Add the indirect gains and the multi-year premium effect to your direct savings, and the "true ROI" of managed comp is far larger than the number on this year's policy.

Partner With a Broker Who Actually Handles the Claim

Pulling these levers takes more than a good quote — it takes someone on your side of the table when the claim comes in. With 30+ years of experience, PCI Consultants doesn't just place your workers' comp; we manage it, taking the claim directly for the life of the policy so an inflated reserve never quietly prices your renewal.

- We build the day-one medical record, contest exaggerated claims, and pay legitimate ones without a fight.

- We design high-deductible programs for qualifying businesses and administer the retained layer for you.

- We make sure your clerical roles aren't rated like your caregivers, and we consolidate multi-location operators for better terms.

The concrete next step is simple. Send us (a) a copy of your current workers' comp policy and (b) your five-year loss runs. That's everything we need to show you where the premium is leaking and model the ROI of a managed program. If you'd rather start with a conversation, a no-cost consultation is the place to begin.

Frequently Asked Questions

What actually drives the ROI of reducing my workers' comp premium?

Mostly claims handling, not carrier shopping. Because premium tends to stay elevated for years after a bad claim, getting each claim valued accurately the first time — with a day-one medical record and fast return-to-work — lowers your rate across multiple renewals, not just one. That multi-year effect is where the real return lives. Individual results vary.

How is a workers' compensation premium calculated?

At a basic level: payroll divided by $100, multiplied by the classification-code rate for each role, then adjusted by your experience modification factor. Two things you can influence directly are making sure roles are classified correctly (clerical vs. hands-on care) and keeping your loss runs clean so your experience mod stays below 1.0.

Can I lower my premium even if I already have a history of claims?

Often, yes — but it's a multi-year project, not a switch you flip. By handling new claims tightly, contesting exaggerated reserves, and returning injured staff to light duty quickly, you improve your loss run and your experience rating over time. A demonstrated, documented commitment to managing risk is what makes carriers price you more favorably. Individual results vary.

Is a "$250,000 claim" really going to cost me $250,000?

Usually not. That headline figure — the "lawyer number" — is often a worst-case reserve. The real medical spend on many claims is a fraction of it, sometimes around $30,000, paid incrementally at roughly $1,500–$2,000 a month rather than as a lump sum. The catch: if no one contests the inflated number, that's what your future premium gets priced against.

What's the main benefit of a high-deductible workers' comp plan?

For qualifying businesses, a much lower upfront premium — sometimes roughly half — and better cash flow, since you retain capital instead of pre-funding an oversized reserve. Claims in your retained layer are paid monthly and stop when the condition resolves. It only works when the retained layer is actively administered, and not every business qualifies.

Why should I trust a broker to minimize my claims cost?

Because of how we're paid. PCI Consultants is compensated by commission from the insurer, not by how many claims you have or how large they run. We have no financial reason to let a claim balloon — in fact, a clean, accurately-valued loss run is exactly what keeps your renewal defensible and keeps you as a long-term client.