Here's what the insurance company won't tell you: your premium isn't really driven by how many of your caregivers get hurt. It's driven by how much each claim actually costs by the time it closes, and by who is managing that number month to month. Left alone, an insurer will pay a claim at or near face value, call it a win, and let your loss history absorb the hit for the next several years. This guide covers why the risk is elevated, what coverage actually pays, the policy structures available, and how a brokerage that handles the claim directly, the way PCI Consultants has for 30-plus years, keeps the real cost down.

Key Takeaways

- Senior living facilities have injury rates 2 to 3 times higher than the private-sector average, so the question isn't whether you'll have claims, it's how they get managed.

- The number an attorney or a claimant floats early (say a "$250,000 claim") is rarely the real cost. Actual medical spend on that same injury is often closer to $30,000, paid incrementally, not as a lump sum.

- Policy structure (guaranteed cost, large deductible, or retrospective rating) determines how much cost you retain and how much control you have over it.

- Getting an injured caregiver seen and documented on day one, then back on light duty within weeks, does more to lower cost than any policy feature.

- Your experience modification rate multiplies against your base premium, and once premiums rise after a bad claim, they rarely come all the way back down.

Why Senior Living Communities Face Elevated Workers' Comp Risk

The combination of physically demanding caregiving, a vulnerable resident population, and round-the-clock staffing creates a risk environment unlike most other industries.

The Primary Hazard Categories

Patient handling is the single greatest source of musculoskeletal disorders (MSDs) for healthcare workers, according to NIOSH. Lifting, repositioning, and transferring residents, often with inadequate staffing or equipment, produces back, shoulder, and knee injuries that frequently require surgery and carry long recovery timelines.

These are exactly the claims that get mispriced. A shoulder or lumbar injury can get framed as a six-figure exposure early on, but the real cost, if it's managed, is usually a fraction of that: an accurate medical record from day one, appropriate treatment, and a structured return to work. Left unmanaged, the same injury drags across multiple renewals and compounds against your mod.

Other significant hazards include:

- Slips and falls in wet kitchens, bathrooms, and hallways

- Biohazard and needlestick exposure, a nursing home study found 22.8% of nurses had experienced a needlestick injury during their career

- Workplace violence and resident aggression, staff working with residents experiencing dementia or behavioral health conditions face elevated physical and psychological injury risk. One study of urban nursing homes found 15.6% of residents directed aggression toward staff

The Staffing Shortage Multiplier

Each of those hazard categories becomes more dangerous when there aren't enough people on the floor. A 2024 AHCA/NCAL survey of 441 nursing home providers found 99% had open positions and 72% were operating below pre-pandemic workforce levels. When fewer staff cover the same resident load, fatigue increases and injury frequency follows.

A PubMed-indexed study of 445 nursing homes confirmed that lower nursing hours per resident day drives measurably higher injury rates (P=.0004), meaning the staffing crisis isn't just a care-quality problem, it's a workers' comp cost driver. When you can't cut frequency because you're short-staffed, the only lever left is controlling the cost of each claim that does happen.

What Workers' Comp Actually Pays for in Senior Living Facilities

Workers' compensation is a no-fault system that pays for medical treatment, lost wages, rehabilitation, and disability benefits when an employee is hurt on the job, regardless of who caused it. That much is standard. What operators rarely understand is how those dollars flow, and that's where the cost is either controlled or lost.

The "Lawyer Number" vs. the Real Number

Early in a claim, someone, often an attorney, floats a big figure: a nurse's back injury becomes a "$250,000 claim." That number is a negotiating anchor, not a fact. The actual medical spend on that same injury is frequently closer to $30,000, and it isn't written as one check. It's paid incrementally, typically around $1,500 to $2,000 a month, for as long as the condition genuinely requires treatment, and it stops when the worker recovers.

The insurer's default is to reserve against the scary number and, if pushed, settle near it. A brokerage that handles the claim directly works the real number: right-sizing reserves, paying legitimate treatment without drama, and refusing to hand over face value on a claim that doesn't warrant it.

Genuine Injuries vs. Exaggerated Ones

This is the distinction that protects your loss history. A caregiver who blows out a knee lifting a resident deserves to be taken care of, and a good claims management process pays that without dispute. But senior living also sees its share of exaggerated or opportunistic claims, and those get investigated and contested rather than rubber-stamped. Sorting the two is how you keep a clean loss run and protect next year's premium. If you suspect a pattern, that's where fraud prevention work earns its keep.

Employee Categories and Risk Profiles

Not every role on your payroll carries the same exposure, and you shouldn't be rated as if it does:

- Direct care staff (nurses, aides, orderlies), highest physical exposure and the source of most patient-handling claims

- Administrative and clerical staff, low physical risk; these payroll dollars should be classified separately so you're not overpaying on them

- Support roles (maintenance, housekeeping, drivers), exposure to equipment, hazardous cleaning agents, and vehicle incidents

Getting a clerk billed under a caregiver class code silently inflates your premium base. Correct risk classification makes sure the high-risk hands-on work is priced as such and the low-risk desk work isn't.

What Workers' Comp Does NOT Cover

Workers' comp excludes:

- Injuries occurring outside of job duties

- Self-inflicted injuries

- Injuries sustained while impaired by drugs or alcohol

- Injuries resulting from clear violation of company policy

- Independent contractors, California regulators cited a home care company more than $2.3 million in February 2025 for misclassifying caregivers as contractors, a gap that leaves senior living operators fully exposed to uninsured injury costs

Workers' Comp Policy Types for Senior Living Communities

Senior living operators typically choose from three workers' comp policy structures. Which one fits depends on your facility's size, claim history, and how much premium volatility you can absorb, but structure only matters if someone is actively managing the claims underneath it.

Guaranteed Cost Policy

The premium is fixed at policy inception and adjusted only at year-end via payroll audit. Claims activity during the policy period doesn't change what you owe that year.

Best for: smaller or newer facilities with limited loss history, or operators who need budget predictability. We often start a growing operator here and move them into a more cost-sensitive structure as their loss history and headcount build.

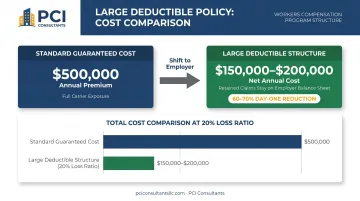

Large Deductible Policy

The facility takes on a defined first layer of each claim and the carrier covers losses above it, which lets the carrier cut the upfront premium substantially. The catch is that you're now paying inside that layer as claims develop, which is precisely why direct claims handling matters so much here.

How the mechanics play out in practice for a qualifying facility:

- The employer takes a defined retention (for example, the first $200,000 of a $500,000 claim) and the insurer covers the rest

- That structure can roughly halve annual premium, for instance moving a facility from around $100,000 a year to about $50,000

- Retained claims are paid on a monthly basis as treatment occurs, often on the order of $3,000 a month, and those payments stop when the condition resolves, rather than being pre-funded as a lump sum

- Because you're carrying the first layer, the claim has to be administered aggressively; that's the brokerage's job, not something you hand back to the insurer

This structure isn't right for everyone. Not every business qualifies, and we'll tell you plainly if the numbers don't support it. You can read a deeper breakdown in our guide to large-deductible workers' comp.

Watch for hidden fees: some carriers embed medical cost containment charges directly into loss-sensitive plan expenses. Before committing, ask whether managed care organization fees, bill review fees, or pharmacy benefit management markups are baked into claim costs.

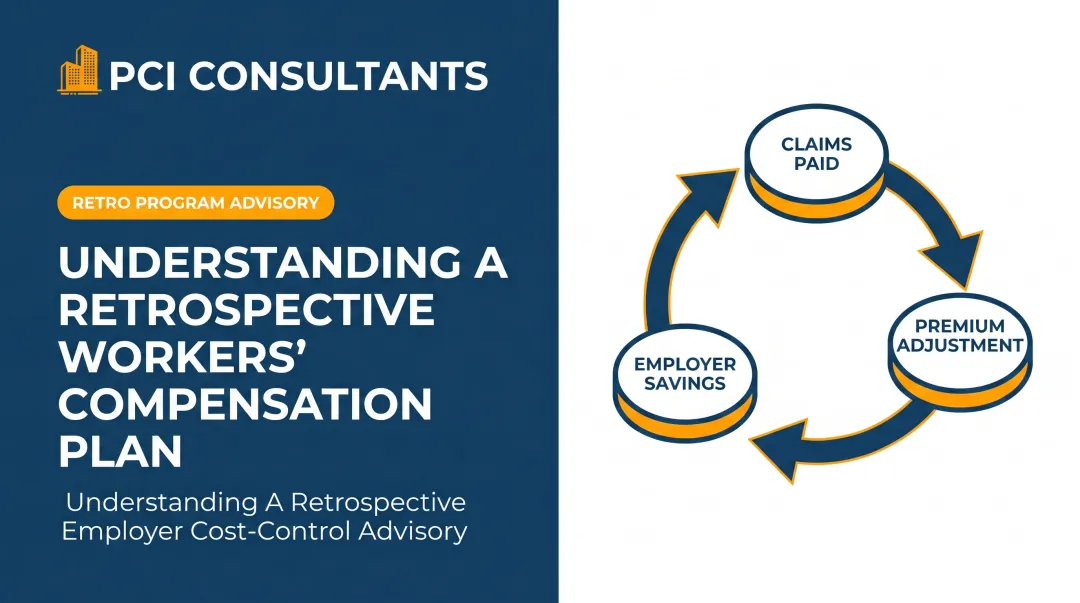

Retrospective Rating Policy

Premium is adjusted after the fact based on actual loss experience, subject to minimum and maximum limits. Low claims mean a refund; elevated claims mean an additional bill. Retro adjustments arrive as periodic lump-sum true-ups, typically at 6, 18, and 30 months after the policy period, which creates a very different cash-flow dynamic than the large-deductible model where the savings land at day one.

The common thread across all three: whichever structure you choose, the number that ultimately decides what you pay is how each claim was handled. Structure without active claims management just changes when you overpay, not whether you do.

Strategies to Reduce Workers' Comp Claim Cost in Senior Living Communities

Report and Evaluate the Incident on Day One

This is the single highest-impact thing a facility can do, and it's where our model differs from the standard broker. When a caregiver is hurt, you call us, not the insurer. We evaluate the incident immediately and, where appropriate, get the injured worker to urgent care that same day. That does two things: it makes sure a genuinely hurt employee is treated fast, and it creates an accurate, timestamped medical record that protects you against a claim that gets exaggerated weeks later.

The data backs the urgency. According to a Liberty Mutual claims analysis, claims reported 29 or more days after injury had:

- 52% higher average cost than claims reported within 3 days

- 152% higher litigation rates

- 33% higher likelihood of converting to indemnity claims

The window between injury and an accurate record directly determines whether a claim stays a $30,000 medical file or balloons into a litigated six-figure fight.

Implement Safe Patient Handling Programs

OSHA states that implementing safe patient handling practices directly reduces a facility's financial burden from workers' comp claims. Formal programs should include mandatory training on proper lift and transfer techniques, mechanical lift equipment and transfer belts, and team-based transfer protocols that remove solo lifting from routine care. Underwriters weigh these programs when pricing your risk, and they target the exact injury category, overexertion and MSDs, that drives the most cost in senior care. This is the frequency side of the equation; our loss control work lives here.

Get People Back to Work on Light Duty, Fast

An injured employee sitting at home is the most expensive version of a claim. Wages are running, reserves are climbing, and the file is drifting toward litigation. The fix is a genuine light-duty path. In practice we've moved an injured nurse who can't do direct patient care into a receptionist-style or intake role within weeks, which keeps her earning, keeps her connected to the workplace, and sharply cuts the real cost of the claim.

That matches what the carriers see. According to NCCI's 2024 insurer-perspectives research, one carrier cut average lost-time claim durations from 9 to 12 months down to 8 to 12 weeks through structured return-to-work programs, with roughly two-thirds of injured employees back within 30 days. Building the modified-duty roles ahead of time is what makes a fast transition possible; our take on return-to-work policies walks through how to set one up. Individual results vary by injury and by how quickly a light-duty role is available.

How to Control Workers' Comp Costs and Avoid Overpaying

Understand Your Experience Modification Rate, and Its Stickiness

The EMR (or "mod") is a multiplier applied to your base premium. A mod of 1.0 is average. Above 1.0, you pay more; below 1.0, you pay less. What operators underestimate is how durable the damage is. A single large claim can elevate your mod for three consecutive policy years before it rolls off the experience rating window, and here's the part that stings: once your premium steps up after a bad claim year, it rarely steps all the way back down even after the claim resolves. That's why controlling a claim's cost while it's open beats trying to recover after the fact.

EMR reduction requires multiple levers pulled together:

- Auditing open claims for inflated reserves (that "lawyer number" sitting on your file)

- Pushing long-tail open claims to close

- Splitting off medical-only claims, which carry reduced weight in the rating formula

- Correcting class-code misallocations so clerical payroll isn't rated as caregiving

- Filing formal recalculation requests when rating-bureau errors surface

We're Not Paid by Your Claims

One structural point worth understanding: a brokerage like PCI is paid by commission from the insurer, not out of your claim dollars and not tied to how many claims you file. So there's no incentive to let a claim run up. Our interest is aligned with yours, keeping your loss history clean and your premium low, which is the opposite of the insurer's default instinct to pay and move on.

Start Renewal Evaluation 60 to 90 Days Early

Waiting until renewal arrives forces you to accept whatever your carrier offers. Starting 60 to 90 days out creates time to clean up loss runs, correct mod errors, explore alternative structures, and market to multiple carriers. Because the mod formula runs on a one-year data lag, today's claims decisions are already writing next year's premium. See our broader playbook on lowering workers' comp costs.

Evaluate Whether a High-Deductible Program Makes Sense

High-deductible programs shift a defined first layer of risk back to the employer in exchange for a much lower premium, structured on strong carrier paper and administered actively so the retained layer doesn't get away from you. For a qualifying facility, that can mean roughly halving annual premium, with retained claims paid monthly (on the order of $3,000 a month for an active claim) and stopping when the condition resolves.

This works precisely because we administer the claims in-house rather than handing them to the insurer. It is not for every operator, and not every business qualifies. As a general guide, a facility usually needs:

- 100+ employees

- $100,000+ in annual WC premium

Whether the numbers work depends on your loss history and workforce mix. Multi-location owners, say several nursing homes under one operator, can sometimes consolidate into a single master policy for better terms as well. The way to find out is a review of your actual policy and losses, not a generic quote.

Legal and Compliance Requirements for Senior Living Facilities

Workers' compensation is legally mandated in nearly every U.S. state, though Texas lets private employers opt out. Coverage requirements, benefit structures, and penalties for non-compliance vary by state, and senior living facilities draw extra scrutiny given their high claim rates.

OSHA compliance is a parallel, independent obligation. OSHA's guidelines for nursing homes and personal care facilities set standards for ergonomics and safe patient handling, bloodborne pathogen exposure (29 CFR 1910.1030) covering needlestick and biohazard protocols, and workplace violence prevention.

Insurance classification rules also depend on where you operate. Facilities in independent rating-bureau states, such as New York, New Jersey, California, and Pennsylvania, follow different classification and rating rules than NCCI states. Operators there should confirm that any consultant or carrier understands the applicable state methodology; national firms defaulting to NCCI standards can produce incorrect class-code filings and overstated premiums.

Your Next Step: A Real Policy Review

A generic online quote won't tell you whether you're overpaying, because it doesn't see how your claims have actually been handled. A real review does. To evaluate your program and show you where the savings are, we need two things: a copy of your current workers' comp policy and your five-year loss runs. From there we can right-size your reserves, check your classifications, model whether a high-deductible structure fits, and tell you plainly what's realistic. Send those over and we'll respond within 24 hours. Individual results vary.

Frequently Asked Questions

What does workers' compensation insurance not cover?

Workers' comp excludes injuries outside job duties, self-inflicted injuries, impairment-related injuries, and injuries from clear policy violations. Independent contractors are generally not covered, though classification rules vary by state and misclassifying caregivers is an expensive mistake in senior living.

Is a workers' comp claim really as expensive as the first number I hear?

Usually not. The large figure quoted early, often by an attorney, is an anchor, not the real cost. A serious back or shoulder injury that gets framed as a "$250,000 claim" frequently carries actual medical spend closer to $30,000, paid incrementally at roughly $1,500 to $2,000 a month for as long as treatment is genuinely needed, and it stops when the worker recovers. The real number depends on how the claim is managed.

What are the most common workers' comp claims in senior living facilities?

The leading types are musculoskeletal injuries from resident lifting and transfer, slips and falls, workplace violence or resident aggression (especially in dementia and memory care), and needlestick or biohazard exposure. Musculoskeletal claims are the most frequent and the most expensive when they aren't actively managed.

How is workers' comp premium calculated for a senior living community?

Premium is based on payroll by employee classification code, the manual rate for each class, and your experience modification rate. Facilities with heavier claim histories carry a mod above 1.0 and pay proportionally more, which is why correct class codes and clean claims handling matter so much.

Can a high-deductible program really cut our premium in half?

For a qualifying facility, roughly halving premium is a realistic pattern, for example moving from about $100,000 a year to around $50,000, by taking on a defined first layer of each claim while the insurer covers the rest. Retained claims are paid monthly and stop when the condition resolves. It requires active in-house claims administration and generally 100+ employees and $100,000+ in annual WC premium. Not every business qualifies, and individual results vary.

What should a senior living facility do immediately after a workplace injury?

Call your claims advocate first, before the insurer, so the incident is evaluated the same day. Get the employee to urgent care right away if warranted, which both treats a genuine injury fast and creates an accurate, timestamped medical record. Document everything, and report the claim within the same business day, since delayed reporting sharply raises average cost and litigation risk.