For a nursing home, home health agency, or hospital—industries that carry some of the highest injury rates in the country—that's not a small worry. Workers' comp is often a six-figure line item, and the fear is that a single lifting injury quietly resets your cost base for the next three years.

Here's the part most insurers won't volunteer: whether your premium goes up—and by how much—depends far more on how the claim is managed than on the injury itself. Left alone, a carrier will usually pay a claim at or near its face value, close it, and frame that as a win. That "win" is exactly what your future premium gets priced on. This article breaks down how a claim moves your premium, why the real cost of a claim is almost always lower than the headline number, and what actually keeps your rates from climbing.

Key Takeaways

- Yes—a claim usually raises your premium, and through your Experience Modification Rate (EMR) it can follow you for up to three years.

- Premiums are sticky: once a claim pushes your rate up, it rarely drops all the way back down after the claim closes—so it's a multi-year cost, not a one-time penalty.

- Your premium is priced on what a claim actually pays out, not the alarming number a lawyer or adjuster first attaches to it.

- Handling the claim directly from day one—immediate medical evaluation, fast light-duty return, and contesting exaggeration—is what controls that payout.

- For qualifying employers, correct risk classification and high-deductible programs can cut premium substantially; individual results vary.

The Short Answer: Yes—And It Tends to Stay Up

Yes. Filing a workers' compensation claim will usually raise your premium. A claim adds to your company's loss history, and insurers price your future risk on that history through your Experience Modification Rate—your "mod." Higher losses mean a higher mod, which means a higher premium.

The part that stings more than the increase itself: once your premium steps up after a claim, it rarely steps all the way back down—even after the claim is closed and the employee is back to full duty. A mod increase is a multi-year cost. That's precisely why what you do during a claim matters more than anything you do after it.

This is where the default insurer relationship quietly works against you. Without someone actively managing the file, a carrier's path of least resistance is to pay the claim, resolve it, and move on. They aren't motivated to spend effort driving the cost of your claim down—so the number that lands on your loss run, and therefore your mod, is usually higher than it needed to be. A brokerage that manages the claim directly—where you call us, not the carrier, the day something happens—exists to close that gap.

Why a Claim Raises Your Premium: The Experience Mod

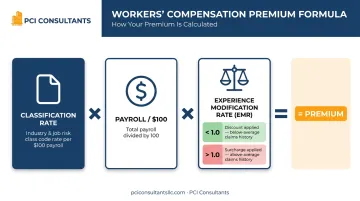

Your workers' comp premium isn't an arbitrary number. It's built from a formula, and understanding it tells you exactly which levers move your cost.

(Classification Rate x Payroll / $100) x EMR = Your Premium

- Classification Rate (Class Code): Assigned by a rating bureau like the NCCI, this reflects the inherent risk of each job. A floor nurse or a resident-transfer aide carries a far higher rate than a billing clerk. It's the baseline cost per $100 of payroll for that kind of work.

- Payroll: This scales the premium to the size of your operation.

- Experience Modification Rate (EMR): The variable you can actually influence. Your experience mod compares your claims history to the industry average, which is set at 1.0. A 0.85 mod earns a 15% discount; a 1.15 mod is a 15% surcharge. Put simply, the percentage swing in your premium roughly equals how far your mod sits from 1.0.

How a Claim Changes Your EMR

A new claim feeds directly into your mod, and the formula looks back over a three-year window—excluding your most recent policy year. That lookback is why a single claim can affect your premium for up to three years.

The formula also weighs frequency more heavily than severity. Six small strains over three years hit your mod harder than one serious injury of the same total dollar value, because frequent small claims look like a systemic safety problem, while a single large loss reads as an anomaly. For a nursing home, that means the steady drip of minor lifting and slip injuries can do more long-term premium damage than one dramatic incident.

The Number That Drives Your Premium Isn't the Injury—It's the Payout

This is the piece competitor articles skip entirely. Your mod isn't driven by how bad an injury sounds. It's driven by what the claim actually costs—the dollars that land on your loss run.

Those two numbers are often wildly different. A back injury can get thrown around as a "$250,000 claim" the moment an attorney attaches a demand to it. But the real medical spend on that same injury is frequently closer to $30,000—and it isn't paid as a lump sum. It's paid incrementally, often $1,500 to $2,000 a month until the worker's condition resolves. Manage the claim well and that $250,000 headline never becomes a $250,000 payout. Leave it unmanaged, and the inflated figure is what you get priced on. Two habits separate the headline from reality.

Get an accurate medical record on day one

The most valuable move after an incident is an immediate, accurate medical evaluation. When a brokerage handles the claim directly, the injured worker can be sent to urgent care right away—before the story has time to grow. That timely record establishes exactly what was injured and how badly, which protects you against exaggeration weeks or months later, when "a sore back" has a way of becoming a career-ending disability in a demand letter. Prompt medical management isn't about denying care—legitimate injuries get treated, fast. It's about pinning down the facts while they're still facts.

Pay real claims fast, contest inflated ones

A genuine injury gets paid without a fight—that's what the coverage is for, and dragging it out only makes the claim (and your mod) worse. But an exaggerated or fraudulent claim gets investigated and contested. Skilled-nursing and home-health settings see both: the aide with a real rotator-cuff tear, and the occasional claim that doesn't line up with the medical record. Paying the first quickly and challenging the second is what keeps your loss history—and next year's premium—honest.

Beyond the Premium: The Hidden Costs of a Claim

A premium increase is the most visible cost of an injury, but it's rarely the largest. The National Safety Council put total U.S. work-injury costs at $181.4 billion in 2024, and most of that never shows up on an insurance invoice. In a care setting the indirect costs bite especially hard:

- Coverage costs—backfilling an injured nurse's shifts with overtime or agency staff, often at a premium rate.

- Administrative drag—time spent managing the claim, fielding adjuster calls, and handling OSHA recordkeeping.

- Care continuity and morale—residents feel the churn of unfamiliar staff, and a serious injury raises anxiety across the floor.

These indirect costs routinely multiply the true impact of a claim well beyond the direct payout—which is all the more reason to keep the payout itself small.

The Fastest Way to Shrink a Claim: Get People Back to Work

A structured return-to-work program is the single most effective cost-control tool you have, because it attacks a claim's biggest driver: lost-time wage replacement.

The move is light duty. An injured floor nurse who can't lift or transfer residents can often step into a receptionist-style or scheduling role within weeks—checking in visitors, handling intake calls, updating charts. That transition does two things at once: it stops the lost-time wage payments that pile onto a claim, and in many states it keeps the claim in the "medical-only" category, which the mod formula discounts by 70%. A claim that never generates lost time barely moves your mod. (Timelines depend on the injury and the treating physician—individual results vary.)

The High-Deductible Option: Trade a Little Risk for a Lower Premium

For larger, financially stable employers, one of the most powerful ways to cut premium is a high-deductible program—and it's worth its own section because most brokers never bring it up.

The structure: you agree to absorb a defined first layer of any claim—say the first $200,000 of a $500,000 policy—and the insurer covers everything above it. In exchange, your annual premium can drop sharply, in some cases roughly in half (think $100,000 down to about $50,000). You don't pay that deductible up front; claim costs within your layer are paid out monthly as they're incurred—often on the order of $3,000 a month—and they stop the moment the claimant's condition resolves. Because you now have real money riding on every claim, the program only works when it's actively administered—claims managed, medical records tightened, return-to-work pushed—not run on autopilot.

The honest caveat: not every business qualifies. High-deductible programs suit employers with the cash flow and loss history to take on that first layer. It's a fit worth exploring for a 100+ employee facility spending six figures on comp—but it's not for everyone, and it's the kind of decision to model out before you commit. (See our deeper breakdown of large-deductible workers' comp.)

Stop Paying for Risk You Don't Carry: Classification

Part of controlling premium happens before a claim ever occurs—in how your payroll is classified. Your workforce should be segmented by actual risk. The administrator at the front desk shouldn't be rated like the aide lifting residents all day. When clerical and low-risk roles get swept into a high-risk class code, you overpay on every dollar of that payroll, year after year. A proper classification and loss-control review makes sure you're only paying for the risk you actually carry.

The same principle scales with you. A smaller home-care agency can be supported and grown over time; and an owner running several nursing homes under separate policies can often be consolidated onto a single master policy for better terms once the book is large enough.

What Actually Keeps Your Premium Down: The Playbook

Understanding how a claim moves your premium is one thing—actively holding it down is another. Five habits do most of the work:

- Handle the claim from minute one. The day an incident happens, get an accurate medical evaluation—urgent care immediately when warranted. The early record is your best protection against a claim inflating later.

- Run a real return-to-work program. Have light-duty roles mapped out before you need them so an injured worker can come back in weeks, not months. This is what keeps claims medical-only and your discounts intact.

- Pay legitimate claims fast, contest the rest. Genuine injuries get paid without friction; exaggerated ones get investigated. That balance protects your loss history without leaving hurt workers hanging.

- Audit your loss runs before every renewal. A loss run is your carrier's record of your claims. Closed claims still marked open, or reserves left too high, quietly inflate your mod—catch them before renewal, not after.

- Classify your workforce correctly—and ask whether you qualify for a high-deductible program. Both can move premium more than any single safety poster ever will.

Where a Claims-Managing Brokerage Fits

Most of the playbook above assumes someone is actually running your claims—and that's the difference between a broker who sells you a policy and one who manages it for the life of the coverage. At PCI Consultants, with over 30 years in workers' comp, clients call us when an injury happens, not the carrier. We evaluate the incident, direct the medical response, push return-to-work, and contest what doesn't add up.

One point worth being direct about: we're paid a commission by the insurer, not a cut of your claims—so we have no financial reason to let a claim run high. Our incentive is a clean loss history and a renewal you can live with. Savings vary by employer and loss history, and no one can promise a specific outcome—but actively managed claims consistently cost less than claims left to run themselves.

Ready to See What Your Claims Are Costing You?

If your premium climbed after a claim and never came back down, that's worth a second look. The fastest way to start is to send us a copy of your current workers' comp policy and your last five years of loss runs—that's all we need to review how your claims have been handled, where your mod is inflated, and what your program should actually cost. It's a no-cost review, not a sales pitch.

Frequently Asked Questions

Does workers' comp insurance go up after one claim?

Usually, yes. A single claim feeds your Experience Modification Rate, which raises your premium—but the size of the increase depends on what the claim actually pays out and whether it involved lost time. A small, well-managed medical-only claim may barely move your mod; a large lost-time claim can raise it for three years.

How much does workers' comp go up after a claim?

There's no fixed percentage. Roughly speaking, your premium moves in proportion to how far a claim pushes your mod above 1.0—a mod of 1.20 is about a 20% surcharge. The actual figure depends on the claim's real cost, your payroll, your industry class, and your prior loss history.

Does my premium come back down after the claim closes?

Not automatically, and often not fully. This is the part employers are most surprised by: premiums are sticky. Once a claim raises your mod, closing the claim helps future years but rarely reverses the increase completely. That's why minimizing a claim's cost while it's open matters far more than anything you can do after it closes.

Should I just pay a small claim out of pocket to protect my mod?

Sometimes it makes sense, sometimes it doesn't—and it depends on the numbers. Because frequency hurts your mod more than severity, keeping a genuinely minor incident off your loss run can help. But paying out of pocket without a medical record can backfire if the injury turns out to be worse than it looked. This is exactly the kind of call to make with a brokerage that manages the claim, not alone.

What's the difference between what a claim is "worth" and what it costs me?

A claim's headline value—especially once a lawyer is involved—is often several times its real cost. A back injury labeled a "$250,000 claim" may carry only ~$30,000 in actual medical spend, paid out monthly rather than in a lump sum. Your premium is priced on the real payout, so managing that number down directly protects your rate.

Do medical-only claims raise my premium as much as lost-time claims?

No. In most states, medical-only claims (no significant lost wages) are discounted by about 70% in the mod formula. That's why getting an injured worker back on light duty quickly—turning a would-be lost-time claim into a medical-only one—is one of the highest-impact things you can do.

What is a loss run?

A loss run is a report from your insurer listing your claims history—dates, amounts paid, reserves, and whether each claim is open or closed. Errors on it (a closed claim shown as open, or an inflated reserve) directly inflate your mod, so it should be reviewed before every renewal. It's also one of the two documents—along with your current policy—a broker needs to quote or take over your coverage.

What is a high-deductible workers' comp plan?

It's a program where you take on a defined first layer of each claim (for example, the first $200,000) while the insurer covers the rest, in exchange for a substantially lower premium. Claim costs in your layer are paid monthly as incurred and stop when the claimant recovers. It can roughly halve premium for qualifying businesses, but it requires active claims administration and isn't right for every employer.

Do I have to pay a workers' comp claim as a lump sum?

Generally, no. Medical and wage benefits on an open claim are paid incrementally over time—often monthly—as costs are actually incurred, and they stop when the worker's condition resolves or the claim settles. The large "total value" numbers attached to serious claims rarely reflect a single up-front payment.