That is why so many employers with strong safety cultures start looking for an alternative to the standard "guaranteed cost" policy. The good news is that real alternatives exist. The more important news is that no structure saves you money on its own. What saves money is how the claim gets handled the day it happens. This guide covers both.

Key Takeaways

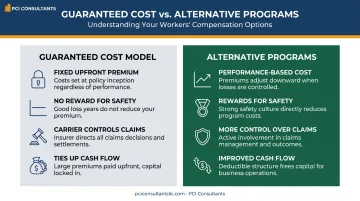

- Traditional "guaranteed cost" workers' comp has a fixed, upfront premium: predictable, but it rewards you nothing for a clean loss year.

- The bigger lever than the plan structure is active, direct claims management, where an advocate evaluates every incident and disputes the exaggerated ones.

- Real alternatives include High-Deductible Plans, Self-Insurance (individual or group), Captive Insurance, and Retrospective Rating plans, though not every business qualifies for each.

- Premiums that rise after a claim rarely come back down, so the cheapest claim is the one that is documented accurately and resolved fast.

First, What Is Traditional "Guaranteed Cost" Workers' Compensation?

The most common option is a "guaranteed cost" policy. You pay a fixed premium to an insurance carrier for the policy period, and that price is set no matter how many claims you have (or don't have) that year.

The premium is built from a standard formula:

- Industry classification codes for the type of work your employees do

- Total payroll in each class code

- Your Experience Modification Rate (e-mod), which compares your claims history to the industry average

It is the "set-it-and-forget-it" option, and the predictability is genuinely worth something. But it has two quiet flaws. First, a spotless year earns you nothing back. Second, and more expensive, the carrier controls the claim. When a maintenance worker or CNA gets hurt, the insurer processes the claim on its own timeline and its own risk appetite, and once your e-mod moves up after a bad year, that higher cost sticks with you long after the injury has healed.

Why Consider an Alternative to Traditional Workers' Comp?

The headline reason is cost. Healthcare employers with disciplined safety programs routinely overpay in the guaranteed-cost pool, effectively subsidizing agencies that don't manage risk at all.

But the deeper reason is control over the claim itself, because that is where the real dollars are won or lost. Consider how a claim actually plays out without an advocate. An aide reports a back injury. Weeks later, a demand letter shows up citing a "$250,000 claim." That is a lawyer number, not a cost. The actual medical spend on an injury like that is often closer to ~$30,000, and it isn't paid as a lump sum, it's paid incrementally, frequently around $1,500 to $2,000 a month. Left alone, an insurer will often reserve and negotiate against the inflated figure because minimizing it isn't their fight.

At PCI Consultants, with 30-plus years doing this, we handle the claim directly for the life of the policy. When an incident happens, you call us, not the insurer. We evaluate it immediately and, when it's warranted, send the injured worker to urgent care that same day so there is an accurate, timely medical record. That record is what protects you months later when a claim gets exaggerated. Genuine injuries get paid without a fight. Exaggerated or fraudulent ones get investigated and contested. Individual results vary, but the pattern is consistent: honest claims resolve cleanly, and inflated ones don't quietly become your loss history.

Two more motivators round it out:

- Faster return to work. A nurse who can't lift a patient can often do a receptionist-style light-duty role within weeks. Getting someone productive again sharply cuts the real cost of the claim, and it is one of the biggest levers most employers never pull. Our return-to-work programs are built around exactly this.

- Better cash flow. Guaranteed-cost policies tie up capital in a large upfront premium. Most alternatives let you fund claims as they occur instead.

Exploring the Main Alternatives to Workers' Compensation

These structures all share one idea: you take on a defined, calculated layer of risk in exchange for real savings. What makes them work is who administers the claims underneath them. Here are the most common options.

High-Deductible Plans

A high-deductible plan is the most accessible alternative for most mid-size and large healthcare employers. You still buy a policy from an A-rated carrier, but you take on a defined first layer of loss, for instance the first $200,000 of a $500,000 program, and the insurer covers everything above it.

The payoff is direct: taking on that first layer can roughly halve your annual premium, for example moving a program from about $100,000 to around $50,000 a year. And you don't write a check for the deductible up front. Claim payments are structured monthly, often in the range of ~$3,000 a month, and they stop when the condition resolves, so you are paying real cost over time rather than a padded reserve up front.

Key Strengths:

- Roughly half the premium for qualifying businesses, because the carrier is no longer pricing in the first layer of every claim.

- Pay-as-you-go claim cost. You fund the deductible layer as costs are actually incurred, and payments end when the worker recovers.

- Every dollar of claim savings is yours. That is exactly why active management matters so much here.

This is not a hands-off product, and not every business qualifies. It suits employers with 100-plus staff, a stable claims history, and $100K-plus in annual WC spend. It only pays off if someone is administering the claims aggressively: sending people to urgent care on day one, moving them to light duty, and disputing the inflated demands. That active administration is the whole game, and it is what we do in-house. Explore how we structure these in large-deductible workers' comp.

Self-Insurance and Group Self-Insurance

Self-insurance means you get state approval to pay your own claims directly instead of buying a traditional policy. It requires substantial financial reserves and a Third-Party Administrator (TPA) to process claims to state rules.

For smaller organizations, Group Self-Insurance pools several similar businesses, often several nursing homes or agencies, so they share the risk and administrative load. This is also where scale helps: a single owner running multiple locations can sometimes consolidate them under one master arrangement for better terms.

- Pros: Maximum control over the claims process, no carrier profit margin, and investment income on reserves.

- Cons: Real financial exposure, strict state-by-state rules, and a need for excess insurance to cap catastrophic losses.

It fits very large, financially stable organizations, or well-established groups of similar employers.

Captive Insurance Programs

A captive is a licensed insurance company you create and own to insure your own risks, either single-parent (one owner) or group (several). It formalizes self-insurance into a real entity, lets you profit from your own good underwriting, and gives direct access to reinsurance for catastrophic coverage. The trade-off is high setup and operating cost and a genuine multi-year commitment.

Retrospective Rating (Retro) Plans

A retrospective rating plan is a hybrid. You pay a standard premium up front, then the final cost is trued up after the policy year based on your actual losses, refunding you if losses were low or charging more (up to a pre-agreed cap) if they were high. It suits employers with fluctuating risk who want to move off guaranteed cost gradually while keeping carrier support.

How to Choose the Right Workers' Comp Alternative

Don't just chase the lowest premium. Find the structure that matches your finances, your risk appetite, and, above all, who will actually manage the claims.

Key Factors in Your Decision

- Financial stability. Self-insurance can demand serious capital. A rough rule: once annual premium clears $100,000-plus, it's worth pricing alternatives seriously.

- Risk classification. Before you pick any structure, make sure your workforce is segmented by real risk. Your clerical and administrative staff should not be rated like hands-on patient-care roles. Getting the class codes and experience rating right is often savings you can capture without taking on any new risk at all.

- Safety culture and claims history. These programs reward employers who genuinely manage injuries and punish those who don't.

- Administrative muscle. Self-insurance needs a TPA. High-deductible plans are simpler on paper but only work with a specialist administering each claim.

- Premium stickiness. Remember that a rate increase after a bad claim year tends not to reverse. That multi-year cost is the real argument for managing every claim tightly from day one, whatever structure you land on.

Common Pitfalls to Avoid When Choosing an Alternative

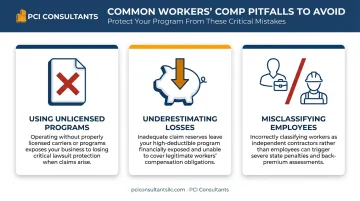

Pitfall #1: Using Non-Compliant or Unlicensed Programs

Be wary of "alternative" health plans or unlicensed carriers that claim to replace workers' comp. Real workers' comp provides an exclusive remedy, the legal protection that stops injured employees from suing you directly. Non-compliant plans don't, leaving you exposed to both lawsuits and state penalties.

Pitfall #2: Underestimating Potential Losses

Don't fixate on premium savings alone. You still have to reserve realistically for the claims inside your deductible or retention. The upside is that with active management those claims run at real cost, that ~$1,500 to $3,000 a month range that ends when the worker recovers, not the inflated numbers a demand letter throws out. Underfund the layer and one bad year hurts.

Pitfall #3: Misclassifying Employees as Independent Contractors

Trying to dodge workers' comp cost by calling employees independent contractors is illegal, and regulators are aggressive about it. According to the New York Workers' Compensation Board, misclassification can bring criminal charges and fines from $5,000 to $50,000, never worth the supposed savings.

Frequently Asked Questions

What is a "guaranteed cost" workers' compensation policy?

It's a fixed-premium policy where the carrier assumes 100% of the claims risk and controls how claims are handled. Costs are predictable, but a clean safety year earns you nothing back, and the carrier has little incentive to minimize any individual claim.

What's the difference between a high-deductible plan and being self-insured?

With a high-deductible plan a licensed carrier is still the insurer of record, while your business funds a defined first layer of loss, often paid monthly as costs occur. With self-insurance your business legally becomes the insurer, posting reserves and paying and managing claims directly through a TPA. High-deductible is the more common step for a healthcare employer moving off guaranteed cost, though not every business qualifies.

How much can a high-deductible plan actually save?

For qualifying businesses, taking on the first layer of loss can roughly halve the annual premium, for example from about $100,000 to $50,000. But the savings only materialize if the claims underneath are actively managed, since every dollar of claim cost now comes out of your pocket. Individual results vary.

Why does active claims management matter more than the plan I pick?

Because the plan sets your maximum exposure, but the handling sets your actual cost. Evaluating an incident immediately, creating a same-day urgent-care record, moving people to light duty within weeks, and contesting exaggerated demands is what turns a "$250,000" claim into a ~$30,000 one paid at a manageable monthly rate. Without that, a carrier tends to pay near face value and move on.

Can a smaller or newer business use an alternative?

Individual self-insurance is really for large, well-capitalized organizations, but smaller employers can often access group self-insurance trusts or group captives that pool similar businesses. We also grow smaller programs over time and, for owners with several locations, consolidate them into a single master policy for better terms.

How do we get started or switch our program?

The concrete first step is simple: send us a copy of your current workers' comp policy and your five-year loss runs. That lets us see your real claims history, check whether your class codes are right, and model which structure, from a claims-managed guaranteed-cost program to a high-deductible plan, would actually lower your cost. We're paid by commission from the insurer, not by your claims volume, so we're not incentivized to see you file more.