That gap is the entire reason PCI Consultants exists. For 30+ years we've placed and actively managed workers' comp for high-injury employers, and we handle the claim directly — when a guard gets hurt, your team calls us, not the carrier. This article covers what California security employers actually need: the legal mandate, the injuries that drive claims, how benefits and premiums work, and — the part most brokers skip — what actually reduces the cost instead of just insuring it.

Key Takeaways

- California Labor Code Section 3700 requires all employers with one or more employees to carry workers' comp — no exemptions for part-time, temporary, or subcontracted guards.

- WCIRB classification code 7721(2) applies to private security guard and patrol services — misclassifying clerical and dispatch staff into the field-guard code inflates premium on your lowest-risk payroll.

- Left to their own defaults, insurers pay security-guard claims at or near the reserved "lawyer number" and call it a win. An actively managed claim is often resolved for a fraction of the reserve.

- Premiums are sticky. Once a claim pushes your X-Mod up, that cost rides your renewals for years — which is why managing the claim on day one matters more than shopping the policy.

- High-deductible structures can roughly halve annual premium for qualifying security firms, with claim dollars paid monthly as conditions resolve rather than pre-funded in a lump sum.

California's Legal Requirement: Workers' Comp for Security Guard Employers

The Mandate and Its Scope

California Labor Code Section 3700 requires every California employer with one or more employees to secure workers' compensation coverage through an admitted insurer, approved self-insurance, or a certificate of consent to self-insure. Security guard companies are not exempt — this applies whether your guards are full-time, part-time, temporary, or seasonal.

California's system is no-fault. An injured guard does not have to prove your company was negligent. The moment the injury arises out of and in the course of employment, the employer owns the liability. No contract with the property owner you're guarding overrides that. What you can control is how the claim is handled once it happens — and that is a very different lever than most owners realize.

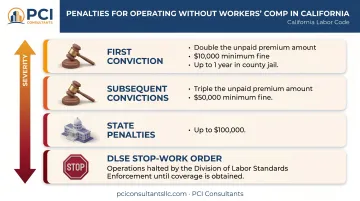

Penalties for Non-Compliance

The consequences of operating uninsured are severe. California Labor Code Section 3700.5 makes failure to secure compensation a criminal misdemeanor. Penalties include:

- First conviction: fine up to double the unpaid premium, minimum $10,000, or up to one year in county jail, or both

- Second or subsequent conviction: fine up to triple the premium, minimum $50,000

- State penalties against illegally uninsured employers: up to $100,000

- The Division of Labor Standards Enforcement (DLSE) can also issue stop-work orders

Coverage isn't only a compliance issue — it's a licensing one. BSIS-licensed Private Patrol Operators (PPOs) must also maintain general liability of at least $1,000,000 per occurrence under California's Private Security Services Act. A lapse in workers' comp puts your PPO license on the line on top of the criminal exposure above.

Exemptions (and Why They Rarely Apply)

California Labor Code Section 3352 excludes certain people from the employee definition — sole proprietors, corporate officers, and general partners or managing LLC members who sign documented waivers. But any security company with W-2 guards on payroll does not qualify. The exemption exists for the owner-operator working alone, not for a staffed patrol operation. If guards clock in for you, you need coverage.

Security Guard Workplace Hazards That Drive Workers' Comp Claims

Security work doesn't generate the highest injury frequency — BLS 2024 data puts investigation and security services at 1.5 recordable cases per 100 full-time workers, versus 2.3 for all private industry. What drives your premium is severity: a handful of serious, contested, long-tail claims. That distinction matters, because severity is exactly what disciplined claims handling can compress.

Four hazard categories account for most of that severity.

Assault and Confrontation Injuries

Guards are the first response to trespassers, theft, and violent individuals. Strikes, blunt-force trauma, and weapons injuries produce high-severity claims with long recovery windows and litigation risk. Nationally, 44 fatal occupational injuries were recorded for security guards and gambling surveillance officers in 2024, and homicides accounted for over a third of fatal injuries in protective-service occupations.

These are also the claims most vulnerable to reserve inflation — the "$250,000 claim" that, once the medical record is nailed down early, actually costs closer to $30,000 in real treatment. The difference isn't luck; it's whether someone documented the injury accurately on day one.

Slip, Trip, and Fall Injuries

Guards patrolling large facilities, parking structures, construction sites, and outdoor properties face real fall exposure — worse on night shifts with poor lighting and uneven terrain. A guard who fractures a wrist or tears a knee ligament on a mobile patrol can generate a six-figure claim across surgery, physical therapy, and lost-time indemnity if it drifts.

Repetitive Stress and Ergonomic Conditions

Stationary post guards carry a slower-burning risk. Extended standing at entry points and long hours monitoring screens produce back, joint, and circulatory conditions over time. These claims develop gradually, often show up as several conditions at once, and are harder to drive to resolution than a clean acute injury — which is where an advocate who knows the file matters.

Occupational Exposure

Guards posted at hospitals, industrial sites, or construction zones face chemical fumes, allergens, and hazardous substances. Respiratory and dermal claims are hard to attribute and easy to dispute, stacking legal cost on top of medical cost.

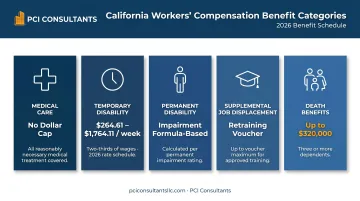

What Benefits Does Workers' Comp Cover for Injured Security Guards in California

California's system covers five core benefit categories for injured guards:

| Benefit | Description |

|---|---|

| Medical Care | All reasonable and necessary treatment for the work-related injury, with no dollar cap |

| Temporary Disability (TD) | Wage replacement while the guard cannot work |

| Permanent Disability (PD) | Ongoing benefits for lasting impairment |

| Supplemental Job Displacement | Voucher for retraining if the guard can't return to the same type of work |

| Death Benefits | Burial expenses and ongoing support for qualified dependents |

Every one of these is a legitimate benefit an injured guard is entitled to — and when a claim is genuine, we pay it without a fight. The advocacy comes in on the exaggerated claim, where a modest strain gets framed as a career-ending injury. Those get investigated and contested; the real ones get paid promptly. Individual results vary, but that split is the whole game.

Temporary Disability in Detail

When an injured guard can't return within three days, temporary disability benefits begin at roughly two-thirds of average weekly wages, subject to statutory limits. For injuries on or after January 1, 2026:

- Minimum: $264.61 per week

- Maximum: $1,764.11 per week

Each additional week of TD adds indemnity and feeds your experience modification rate. This is precisely why getting a recovering guard back to work — even in a limited role — beats letting the clock run.

Permanent Disability and Death Benefits

Lasting impairment — a back condition from a patrol fall, hearing loss from a violent confrontation — can qualify a guard for permanent disability, calculated from the extent of impairment, the guard's age and occupation, and the injury date. Death benefits apply to on-duty fatalities: burial reimbursement up to $10,000, ongoing weekly support of at least $224.00, and total death benefits reaching $250,000 for one total dependent and $320,000 for three or more. For armed or high-risk patrol operations, that exposure is real and it belongs in your risk plan.

How Workers' Comp Premiums Are Calculated for Security Guard Companies in California

The WCIRB Classification System

California uses a classification system administered by the Workers' Compensation Insurance Rating Bureau (WCIRB). Private security guard and patrol services fall under WCIRB code 7721(2); guards on armored-transport work fall under a separate code (7198(2)).

This is where risk classification saves real money. Your dispatchers, console operators, and back-office admins are not exposed to the same hazard as a guard walking a construction site at 2 a.m. — and they shouldn't be rated as if they were. Segmenting your workforce by actual risk keeps you from overpaying on low-risk clerical payroll, which is one of the most common and most expensive mistakes we correct on a security firm's policy.

The Base Premium Formula

The formula itself is simple:

(Payroll ÷ $100) × Classification Rate × Experience Modification Factor = Premium

The experience modification factor (X-Mod) is where it gets expensive. WCIRB compares your actual loss history to expected losses for comparable firms. An X-Mod above 100% multiplies your premium upward; strong safety practices and managed claims hold it below 100%. And here's the sticky part most owners learn the hard way: once a bad claim pushes your mod up, the premium rarely drops all the way back even after the claim closes. You pay for that one claim across multiple renewal cycles — which is why what happens in the first 48 hours of an incident matters more than which carrier's logo is on the policy.

Key Cost Drivers for Security Firms

- Assignment type — mobile patrol carries higher inherent injury risk than static post work; carriers price the difference.

- Client industry — guards at nightlife venues, hospitals, and construction sites sit in elevated-hazard environments.

- Payroll size and shift hours — premium scales directly with total payroll.

- Subcontracted or temporary guards — payroll must be disclosed and classified correctly; omissions are a classic audit trigger.

- Clerical and supervisory misclassification — folding admin or dispatch staff into the field-guard code inflates premium on your safest payroll.

Each of these compounds at audit, which is why classification accuracy has to be right before the carrier's review, not argued afterward. WCIRB's credibility weighting and rating methodology differ meaningfully from NCCI, so cleanup work built on generic bureau assumptions tends to fall apart when it hits the California rating engine.

How California Security Guard Companies Can Reduce Workers' Comp Premiums

Most brokers "reduce" your premium by re-shopping the same risk to a different carrier. That's a one-year trick. Real, durable savings come from changing what your loss runs look like and how your program is structured. And it's worth saying plainly: we're paid by commission from the insurer, not by your claims volume — so we have no incentive to let a claim run up. Our incentive is to keep you on the books happy, year after year. Three levers actually move the number.

1. We Handle the Claim Directly — and Correct the "Lawyer Number"

When a guard is hurt, your supervisor calls us, not the carrier. We evaluate the incident immediately and, where appropriate, get the injured worker to urgent care right away — which creates an accurate, timely medical record. That record is your best protection against a modest injury being re-framed weeks later as something career-ending.

Left alone, an insurer will often reserve an assault claim at a big round "lawyer number" — say $250,000 — and, if nobody pushes back, pay near that figure and call it a win. Actively managed, the real medical spend on that same claim might land near $30,000, paid incrementally (frequently in the ~$1,500–$2,000/month range as treatment proceeds) rather than as one lump sum. Genuine injuries get paid without dispute. Exaggerated or fraudulent ones — inconsistent injury mechanisms, suspicious attorney timing, patterned providers — get investigated and contested through claims and litigation management. That protects your loss history, and your loss history is what sets your future premium. Individual results vary, but the pattern is consistent.

2. Return Injured Guards to Work Faster

Under WCIRB's experience rating, lost-time claims weigh far more heavily than medical-only claims. So we build realistic modified-duty return-to-work roles for injured guards — console monitoring, dispatch coordination, internal training — and move people into them within weeks, not months. Bringing an injured guard back to a light-duty console seat, even at reduced capacity, converts a long-tail indemnity claim into a limited lost-time claim, cutting both the reserve and the mod impact. It's the same logic as moving an injured nurse to a receptionist-type role: the paycheck keeps flowing, and the claim stops bleeding.

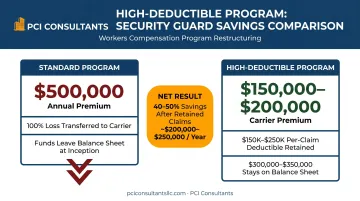

3. Restructure to a High-Deductible Program (For Qualifying Firms)

For security companies spending six figures a year on workers' comp, the structure of the policy is often the biggest lever of all. In a high-deductible program, the employer takes on a defined first layer of loss (for example, the first $200K of a $500K program) and the carrier covers the rest. Because the carrier's projected outlay drops, the underwriting premium can fall sharply — often roughly in half (a $100K premium moving toward $50K is a realistic illustration).

The part that scares owners is usually the part we handle:

- Retained claims are paid monthly as they age — think on the order of ~$3,000/month on an active file — and the payments stop when the condition resolves. You are not writing a lump-sum check at inception.

- The program is actively administered by us, not dropped in your lap — the same direct claims handling that keeps the numbers honest.

- This is not for everyone. Not every business qualifies — it depends on your loss history, payroll, and risk profile, and we'll tell you straight if it doesn't fit.

If you're a smaller or newer patrol operation, this may not fit yet — but it's often a destination we grow clients toward over a few renewal cycles. And multi-location owners (say, several guarded properties or facilities under one company) can frequently be consolidated onto a single master policy for better terms than each site carries alone.

Frequently Asked Questions

What kind of insurance should a security company have?

California security companies need workers' compensation (Labor Code 3700), general liability of at least $1,000,000 per occurrence (required for BSIS PPO licensing), commercial auto, and professional liability. Armed operations should add umbrella or excess liability given the catastrophic-injury exposure. Workers' comp is usually the largest and most volatile line — which is where active claims management pays for itself.

Who is exempt from workers' compensation insurance in California?

Labor Code Section 3352 exempts certain sole proprietors, corporate officers who sign written waivers, and general partners or managing LLC members with documented waivers. Any security company with W-2 guards on payroll almost certainly does not qualify and shouldn't assume it does.

Is workers' compensation insurance required for security guard companies in California?

Yes. Labor Code Section 3700 mandates coverage for any employer with one or more employees — no exceptions for industry, shift structure, or guard classification. BSIS-licensed PPOs face the same requirement under the Private Security Services Act.

How is workers' compensation premium calculated for security guards in California?

Payroll divided by $100, multiplied by the WCIRB rate for code 7721(2), then adjusted by your experience modification factor. Separating guard payroll from administrative and dispatch payroll is critical — commingling it at audit routinely triggers retroactive charges, and paying the field-guard rate on clerical staff is money left on the table.

What injuries are covered under workers' compensation for security guards?

All work-related injuries, under California's no-fault system: physical altercations, slip-and-falls on patrol, repetitive stress and musculoskeletal conditions, occupational chemical or allergen exposure, and on-duty fatalities. The guard doesn't have to prove employer negligence. Legitimate claims are paid promptly; exaggerated ones are where documentation and investigation matter.

How can security guard companies reduce their workers' compensation premiums in California?

The levers that actually work: direct, active claims management that keeps reserves honest and closes files faster; a return-to-work program with light-duty roles for injured guards; and — for qualifying firms — restructuring to a high-deductible program where you can roughly halve annual premium and pay retained claims monthly as they resolve. Individual results vary, but changing your loss runs beats re-shopping the same risk every year.

Want to know what your security operation is actually overpaying? The fastest way to find out is to send us two documents: a copy of your current workers' comp policy and your five-year loss runs. We'll review them and come back with a straight read on your X-Mod, your classifications, and whether a high-deductible structure fits — typically within 24 hours. Start with a no-cost workers' comp consultation.