Here is the part the insurance company usually won't tell you: left to their own devices, insurers tend to pay claims at or near face value and call it a win. Closing a file fast is easier than fighting one. That default behavior is exactly why an exaggerated claim so often gets paid as if it were legitimate, and why the cost lands on you.

This guide lays out how to identify, detect, and actually contest fraudulent workers' comp claims, and how the way a claim is handled from day one, not just a policy binder in a drawer, is what separates a $30,000 real cost from a $250,000 headline number.

Key Takeaways

- Genuine injuries should be paid quickly and without dispute; the goal is not to fight your workers, it's to contest the exaggerated and fraudulent minority that drive up everyone's cost.

- A day-one, accurate medical record, often created by sending the injured worker to urgent care immediately, is the single strongest defense against later exaggeration.

- Common red flags include unwitnessed Monday-morning injuries, stories that change, and refusal of reasonable diagnostics.

- Because premiums rarely fall back down once they rise, an inflated or fraudulent claim on your loss run is a multi-year cost, not a one-time one.

Common Types and Causes of Workers' Comp Fraud

Workers' comp fraud happens when someone intentionally deceives the system to collect a benefit they aren't owed, or to dodge a cost they do owe. It shows up on both sides of the ledger.

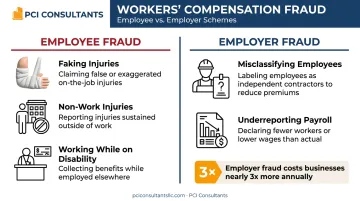

Employee (Claimant) Fraud and Exaggeration

The honest truth is that outright faked injuries are rarer than exaggerated ones. In a nursing home, the far more common scenario is a real but minor strain that gets stretched into months of lost time and a five-figure treatment plan. The patterns to watch:

- Exaggerating a genuine injury: A minor lifting strain becomes a debilitating, work-stopping condition. The injury is real; the severity and duration are inflated, often once an attorney is involved and the demand balloons into a "lawyer number."

- Claiming a non-work injury as work-related: An aide hurts a shoulder moving furniture at home over the weekend, then reports it as a Monday-morning transfer injury so the medical bills and lost wages get covered.

- Working while on disability: Someone collects temporary disability from your facility while quietly picking up cash shifts elsewhere, drawing pay from two sources for the same period.

Employer (Policy) Fraud

Employer-side fraud is a larger dollar problem than most people assume, and it is almost always about illegally shrinking a premium. The two main forms:

- Misclassifying employees: Labeling hands-on caregivers as "independent contractors" to avoid paying for coverage.

- Underreporting payroll: Reporting fewer employees or lower wages than reality to secure an artificially low premium.

Both blow up at audit time. The legitimate version of controlling premium is proper risk classification, segmenting your clerical and administrative staff away from your high-risk hands-on caregivers so you aren't overpaying on the receptionist's payroll while accurately reflecting the aides'. That's the honest lever, and it's one an advocate can pull for you without any exposure at audit.

The High Cost of Ignoring Workers' Comp Fraud

The damage from a fraudulent or padded claim runs well past the check that gets cut.

The "Lawyer Number" vs. the Real Cost

This is where most employers overpay without realizing it. A claim gets characterized as a "$250,000 claim," and everyone treats that headline as gospel. In reality, the actual medical spend behind it is often closer to $30,000, and it isn't handed over as a lump sum. It's paid incrementally, frequently in the range of $1,500 to $2,000 a month, and those payments should slow or stop as the worker's condition resolves.

When no one is actively managing the file, the insurer reserves against the scary headline number, that reserve hits your loss history, and your premium is set off the inflated figure. Correcting a lawyer number down to its real cost is one of the highest-leverage things active claims handling does. Individual results vary, but the gap between the demand and the true spend is routinely enormous.

Premium Stickiness

Here's the multi-year sting: once your premium goes up after a bad claim, it rarely comes all the way back down, even after the claim resolves. An exaggerated claim that never gets contested doesn't just cost you this year. It sits on your loss runs and quietly taxes you at renewal after renewal. That's why letting a questionable claim slide "to keep the peace" is usually the most expensive option on the table.

Operational and Cultural Damage

A suspicious claim also drains your managers' time and, left unaddressed, corrodes morale. Honest staff notice when someone games the system and picks up nobody's slack. Contesting the exaggerated minority while paying legitimate injuries promptly is what actually protects the culture, not looking the other way.

Red Flags: How to Identify Potential Fraudulent Claims

No single flag proves fraud. A cluster of them means the claim deserves a real look before anyone reserves six figures against it.

Suspicious Timing and Reporting

- The injury surfaces Monday morning or right after a weekend, holiday, or the end of a travel-nurse assignment.

- The claim lands just after disciplinary action, a poor review, or a layoff notice.

- There's an unexplained delay between the alleged incident and the report.

Inconsistent or Vague Incident Details

- The story changes or contradicts what coworkers on the floor describe.

- The incident report is thin on time, location, or mechanism of injury.

- No witnesses, despite the injury supposedly happening in a busy hallway or shared patient room.

Unusual Medical and Behavioral Patterns

- The claimant refuses reasonable diagnostics (an MRI or X-ray) that would confirm the injury.

- A history of multiple, similar claims across employers.

- The person becomes hard to reach, or unusually combative, once the claim is filed.

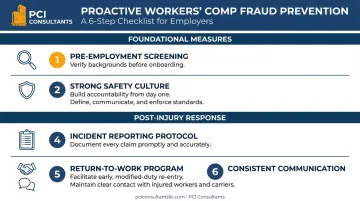

Proactive Strategies to Prevent Workers' Comp Fraud

The best defense is built before an incident ever happens, and it starts the moment one does.

The Day-One Medical Record

This is the single most underused tool employers have. When an incident is reported, the injury should be evaluated immediately, and in many cases the worker should be sent to urgent care right away. Not to be adversarial, but to create an accurate, contemporaneous medical record. That timely documentation is what protects you against exaggeration weeks later, when a minor strain has somehow become a permanent disability. It's also what confirms a serious injury fast so a genuinely hurt caregiver gets the right care without delay. When we handle a claim directly, this is step one, and it's why clients call us, not the insurer, the moment something happens.

Foundational Prevention Measures

- Pre-employment screening: Thorough background and reference checks, done in compliance with the Fair Credit Reporting Act, help surface a pattern of prior suspicious claims before you hire.

- A genuine safety culture: Regular training, clear transfer and lifting protocols, and hands-on management involvement cut real injuries and make faked ones stand out. OSHA has documented meaningful drops in injury claims following strong safety programs, including one study showing a 9.4% decline after a safety inspection.

- A clear, written fraud policy: Every new hire should sign off on a plain-language policy that explains what fraud is, the consequences, and how to report suspicions anonymously.

Post-Injury Response and Light-Duty Return-to-Work

- A formal incident protocol: Managers should know the exact steps: evaluate the injury, get the worker to care, secure the scene, interview witnesses immediately, photograph the area, and document everything while memories are fresh.

- A real return-to-work program: Light-duty transitions are one of the strongest fraud deterrents there is. An injured nurse who can't be on the floor can often move to a receptionist-type or intake role within weeks. That keeps a genuinely injured employee connected and paid, and it sharply cuts the real cost of the claim, while making it far less appealing for someone exaggerating an injury to sit home collecting benefits. A structured return-to-work program is where prevention and cost control meet.

- Consistent, supportive contact: Staying in regular touch signals you care about recovery and deters the person who'd otherwise go quiet and let a claim drift.

Building a Long-Term, Fraud-Resistant Approach

A checklist alone won't hold. What actually protects your loss history is having someone whose job is to work the claim, every claim, for the life of the policy.

Genuine Claims Paid, Exaggerated Claims Contested

The distinction matters. A legitimately injured aide should be paid promptly and without dispute; fighting real injuries is both wrong and shortsighted. The exaggerated and fraudulent minority are the ones that get investigated and contested. That balance is what keeps your loss runs clean and your future premiums protected, and it's the opposite of the insurer's default instinct to pay everything at face value and move on.

Who Actually Handles the Claim

At PCI Consultants, with more than 30 years in workers' comp, we handle the claim directly. When one of your caregivers is hurt, you call us, not the carrier. We evaluate the incident immediately, build the day-one medical record, push exaggerated "lawyer numbers" back down toward their real cost, and drive light-duty return-to-work. Because we're paid by commission from the insurer, not by how many claims you file, we're not incentivized to let your claims run up. Our interest is in keeping your loss history and your premium down.

For employers with stubbornly high premiums, we also administer high-deductible programs for qualifying businesses, where you take on a defined first layer of risk and the insurer covers the rest. Structured and actively managed, that can roughly halve an annual premium, though not every business qualifies. It works precisely because someone is managing each claim to its true cost rather than the headline. Individual results vary. If you want to see where you stand, our team can lower your overall costs starting with a review of your existing claims.

Frequently Asked Questions

What is the most common type of workers' comp fraud?

In healthcare, outright faked injuries are less common than exaggerated ones, a real but minor strain stretched into months of lost time and a five-figure treatment plan. On the employer side, underreporting payroll and misclassifying caregivers as independent contractors are the larger dollar problems. The fix for exaggeration isn't suspicion of every worker; it's an accurate day-one medical record and active management of the claim.

How do you tell a genuine injury from an exaggerated claim?

You don't guess, you document. Evaluating the incident immediately and, where appropriate, sending the worker to urgent care right away creates a timely, accurate medical record. A genuine injury is confirmed and paid; an exaggerated one becomes hard to sustain when the contemporaneous record doesn't match the later demand. Red-flag patterns (changing stories, refused diagnostics, unwitnessed Monday injuries) tell you which files to look at harder.

Why do fraudulent claims cost so much more than the actual injury?

Because claims are often characterized by a "lawyer number." A file called a "$250,000 claim" may reflect only around $30,000 in real medical spend, paid incrementally at roughly $1,500 to $2,000 a month, not as a lump sum. Left unmanaged, the insurer reserves against the inflated figure and your premium is set off it. Correcting that number down is a core part of active claims handling, though individual results vary.

What is the first step an employer should take if they suspect fraud?

Document the incident thoroughly and route it to whoever is actively managing your claims, ideally the same day. Don't confront the employee directly. In our model, that's when clients call us: we evaluate the incident, secure the medical record, and decide whether the claim is a legitimate one to pay or an exaggerated one to contest.

Does contesting one claim really affect my premium?

Yes, and for longer than most employers realize. Once a claim inflates your loss runs and your premium rises, it rarely comes all the way back down even after the claim resolves. That premium stickiness is why an uncontested exaggerated claim is a multi-year cost, and why it's worth managing every claim to its true value.

Can an employer commit workers' compensation fraud?

Yes. The most common employer schemes are underreporting payroll, misclassifying employees as independent contractors, and failing to carry required coverage. The legal way to control premium is accurate risk classification and active claims management, not misreporting, which blows up at audit and can carry serious penalties.