Here's what the insurance company won't tell you: your premium is not a fixed number handed down from on high. It is shaped by decisions you make before an injury happens, how the claim is handled the day it does, and how the underlying program is structured. Get any one of those wrong and you overpay — often for years, because premiums that rise after a claim rarely come all the way back down.

This article lays out 9 practical ways to reduce workers' compensation premiums, organized around those three levers, with the highest-leverage strategies covered in depth.

Key Takeaways

- Your E-Mod multiplies every dollar of base premium — actively managing it is your single highest-leverage cost lever

- Claim frequency damages your E-Mod more than claim severity — small, repeated injuries are the bigger threat

- How a claim is handled on day one — including an immediate, accurate medical record — largely determines what it costs

- The number a claimant's attorney floats is rarely the number the claim actually costs; the real spend is usually a fraction of it, paid monthly, not in a lump sum

- Once a claim pushes your premium up, it tends to stay up — so the cheapest claim is the one that's handled fast and closed clean

- High-deductible programs can roughly halve annual premium for qualifying businesses, but only with active claims management behind them

How Workers' Compensation Costs Actually Build Up

Workers' comp costs don't reset at renewal the way most employers assume. Each reported claim enters your loss history, feeds your experience modification rate (E-Mod), and that E-Mod multiplies your base premium at the next renewal and the two after it. One bad claim year costs you three times over — and because rates are sticky, the drift upward is far easier than the drift back down. We cover that dynamic in depth in does workers' comp go up after a claim.

The Hidden Cost Multiplier

Direct claim costs — medical bills, wage-replacement payments — are only part of the picture. OSHA's Safety Pays program uses indirect cost ratios of 1.1x to 4.5x on top of direct costs. In a nursing home those indirect costs are real: agency staff to backfill an injured aide, supervisor time on the incident, disruption on the floor, and the loss-history hit that raises next year's premium.

But here is the part most brokers gloss over. The face value of a claim and its real cost are two very different numbers. When a worker is injured and a lawyer gets involved, you may see a demand framed as a "$250,000 claim." Left alone, an insurer will often reserve near that figure and, if pushed, pay close to it and call it a win. In practice the actual medical spend on the same injury is frequently closer to $30,000 — and it is paid incrementally, roughly $1,500 to $2,000 a month, not as a lump sum, and it stops when the worker recovers. The difference between those two numbers is the difference between a premium that spikes for three years and one that barely moves.

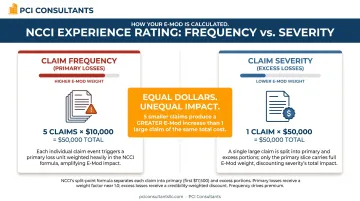

Why Frequency Matters More Than Severity

That E-Mod compounds faster than most employers expect, partly because of how NCCI's experience rating formula weights losses. Claims split into "primary" losses (reflecting frequency, weighted heavily) and "excess" losses (reflecting severity, weighted less). Five $10,000 claims hit your E-Mod harder than one $50,000 claim.

Controlling minor, repetitive claims — the strains, the slip-and-lift injuries that pile up on a busy caregiving floor — matters as much to your mod as preventing the catastrophic ones. Often more.

The Three Structural Drivers of What You Pay

Before the 9 tips, it helps to name the three inputs that actually set your bill.

Base premium is your payroll multiplied by a class code rate per $100 of payroll. Get the class code wrong — or let the auditor assign the wrong one — and you overpay before a single claim is filed.

The E-Mod score reflects your three-year rolling claim history against industry peers. Above 1.0 means you pay more than the average employer in your class; below 1.0 is a discount. Most employers treat it as fixed. It isn't — and that's where the most money is left on the table.

Claim-management quality is the most variable employer-controlled driver, and it feeds straight into the E-Mod. Three behaviors decide how much damage an open claim does:

- How fast the injury is reported and a medical record is created

- How aggressively a light-duty return to work is pursued to close the claim

- How effectively exaggerated or fraudulent claims are identified and contested

This is exactly where a brokerage that handles claims directly changes the math. At PCI Consultants, with 30-plus years doing this, the injured worker's employer calls us, not the insurer. We evaluate the incident immediately and, when warranted, send the worker to urgent care that same day — creating an accurate, timely medical record that protects you against a later, inflated version of events.

9 Expert Ways to Reduce Workers' Compensation Premiums

Organized across three levers: decisions that prevent cost, management that reduces cost once an injury happens, and program-level changes that address the structural drivers.

Tips That Reduce Costs by Changing Decisions

Tip 1 — Build a Written Safety Program and Actually Run It

A documented safety program is the most direct way to cut claim frequency, and it often carries a financial reward on top of fewer injuries. Pennsylvania's certified workplace safety committee program, for example, offers a 5% annual premium discount for qualifying employers, and many carriers add loss control credits for documented programs.

The components that matter:

- Hazard identification — formal job-hazard analysis for high-risk roles (patient handling, transfers, lifting)

- Written protocols — documented safe-lift and transfer procedures where injuries actually cluster

- A real training cadence — repeated reinforcement, not a one-time orientation

- A safety committee with authority to fix what it finds

The program only earns credit if it's practiced, not filed. Insurers increasingly verify implementation at audit — a binder on a shelf doesn't qualify.

Tip 2 — Classify Your Workforce by Actual Risk

Every role in your operation carries a class code and a manual rate per $100 of payroll. Lump a low-risk role into a high-risk code and you overpay on every dollar of that payroll. The fix is to segment the workforce by actual risk: your clerical and administrative staff should not be rated like your hands-on caregivers.

Common misclassification errors:

- Clerical and billing staff allocated to a hands-on care code

- Supervisors not split out from the code of the staff they oversee

- Drivers or maintenance folded into a higher-rated code

- Multi-state payroll not separated by state-specific differentials

California's WCIRB has found that more than 10% of test-audited policies carry incorrect class codes; the national picture is likely similar. Review your codes every year, and any time duties change. For a workforce with a real mix of clerical and high-risk roles, an independent class-code review routinely uncovers four- to six-figure annual overcharges.

Tip 3 — Hire Safety-Minded and Onboard Hard

New hires are a disproportionate injury risk. Travelers' Injury Impact Report found that more than one-third of all workplace injuries and one-third of claim costs occur among employees in their first year. You can't legally ask about prior comp claims, but you can:

- Use post-offer physical capability assessments to confirm fitness for patient-handling demands

- Ask safety-focused behavioral questions about how candidates have handled hazards and near-misses

- Front-load safety training in the first 30–60 days, when the risk is highest

The goal is to shrink the concentration of injuries in the riskiest employment window.

Tips That Reduce Costs by Changing How Claims Are Handled

Tip 4 — Report Immediately and Handle the Claim Directly

Delayed reporting is one of the most predictable and preventable cost drivers in comp. Liberty Mutual's reporting-lag study uses claims reported within 0–3 days as its baseline and finds costs climbing once reporting slips past a week. Late-reported injuries go untreated, medical costs accumulate, and — critically — the worker often talks to an attorney before the employer has established the facts.

This is where direct claims handling earns its keep. Left to itself, an insurer's default is to pay a claim at or near face value and move on; it isn't their money being multiplied through your mod for three years. With active claims management, the incident is evaluated the moment it happens, an accurate medical record is created same-day, and every claim is worked toward the fastest supportable close. Legitimate injuries are paid without a fight — that's the point of the coverage. Exaggerated or fraudulent ones get investigated and contested, which protects both your loss history and your future premium. See our approach to fraud prevention for how that works in practice.

And because PCI is paid by commission from the insurer — not by how many claims you file or how much they cost — our incentive is squarely aligned with keeping your total cost of risk down. Individual results vary, but the pattern is consistent.

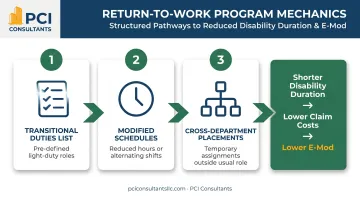

Tip 5 — Get People Back to Work on Light Duty, Fast

Every day an injured worker is fully off the job generates wage-replacement dollars that drive up both direct cost and E-Mod impact. A structured return-to-work program shortens that window, and the math is compelling. A peer-reviewed Washington State study found structured occupational-health models produced a 30% reduction in the risk of long-term disability versus standard care.

In practice this is faster and more concrete than employers expect. An injured nurse who can't return to the floor can often move into a receptionist-type light-duty role within weeks — still working, still earning, while the wage-replacement clock stops and the real claim cost drops sharply. Medical management that stays in contact with the treating provider is what makes that transition happen on a timeline of weeks instead of months.

An effective program is built on a pre-defined transitional-duty list specific to your operation, modified schedules, and cross-department placements — not generic placeholders.

Tip 6 — Read Your Claims History and Investigate Every Incident

Your insurer or TPA can break claims down by department, shift, role, and tenure. Ask for it — most employers never do — and you'll see exactly where injuries cluster (night shift transfers, a particular unit) so safety spending goes where it pays.

Every incident also deserves a real investigation: photos immediately, witness statements within hours, and a root-cause look aimed at fixing the hazard. That documentation does double duty. It drives prevention, and it's what lets us tell a genuine injury from an exaggerated one. A claim with inconsistencies in the mechanism of injury or the timeline is one a direct-handling brokerage can challenge — while the same-day medical record we create keeps an honest claim honest.

Tips That Reduce Costs by Changing the Program Itself

Tip 7 — Understand and Actively Manage Your E-Mod

Most employers get their E-Mod at renewal, note the number, and move on. That's expensive. The mod is built from loss runs filed with your rating bureau, and those runs carry errors — and open reserves — that inflate it more often than employers realize.

An E-Mod review should:

- Pull the detailed unit statistical report from the carrier or bureau

- Identify open claims still carrying reserves against the current mod

- Check for valuation errors and split-point miscalculations

- Push to close long-tail claims at supportable values — open reserves are the fastest route to an inflated mod

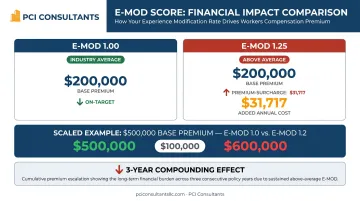

The stakes are real. In NCCI's own example, a 1.25 mod adds $31,717 to premium versus a 1.00 mod on a single policy. On a $500,000 premium, moving from 1.2 to 1.0 is tens of thousands in immediate annual savings — compounding across three policy years.

Tip 8 — Consider a High-Deductible Program (for Qualifying Businesses)

Standard guaranteed-cost policies bake the carrier's risk margin and profit into every premium dollar, no matter how few claims you file. For employers with a strong loss record, that means subsidizing the carrier's book year after year.

A high-deductible program works differently: you take on a defined first layer of loss — say the first $200,000 of a $500,000 program — and the insurer covers everything above it. Because the carrier's projected outlay drops, so does the premium, often roughly in half (for example, from about $100,000 down to about $50,000 a year). Retained claims are paid monthly as they age — on the order of $3,000 a month — and the payments stop when the condition resolves, not in a lump sum. It is not a set-and-forget product; it only works when the claims underneath it are actively administered, which is exactly what our direct-handling model provides.

This is not for everyone — not every business qualifies. It fits employers whose actual claim experience runs well below their mandated premium, with the cash flow to carry the retained layer. Healthcare operators with large, low-severity workforces are often a strong fit. We walk through the mechanics in large-deductible workers' comp.

Tip 9 — Audit Premiums and Consolidate Where You Can

Year-end premium audits are where employers quietly lose money. Common carrier errors:

- Overtime not capped to the straight-time rate

- Subcontractor payroll added when the sub carried its own coverage

- Officer exclusions not applied

- Per diems and reimbursements folded into the payroll base

Prepare before the auditor arrives — payroll documented by class code, current certificates on file — so you prevent errors instead of disputing them later. And if you operate multiple locations under one owner — several nursing homes, for instance — those separate policies can often be consolidated into a single master policy for better terms and cleaner administration. Smaller or newer operations can be grown into stronger programs over time as their loss history matures.

Conclusion

Workers' compensation is not a fixed line item. It's the output of decisions made before injuries, the way claims are handled when they happen, and how the program is structured. Cutting cost without knowing which lever is driving it is the most common and most expensive mistake employers make.

The insurer's default is to pay claims near face value and call it a win. A brokerage that takes the claim call directly, creates the medical record on day one, moves people back to light duty in weeks, and contests the claims that deserve contesting produces a very different loss history — and a very different premium. For qualifying businesses, a high-deductible structure on top of that can roughly halve the annual bill. Individual results vary, but the direction is consistent.

The concrete next step is simple. Send us a copy of your current workers' comp policy and your five-year loss runs. That's all we need to show you where your premium is leaking and what a managed program would look like for your operation. Start with a no-cost consultation, and if you run senior-care facilities, our nursing-home program work is a good place to see the approach applied.

Frequently Asked Questions

How do you reduce workers' compensation premiums?

Three levers: cut claim frequency with real safety and correct risk classification, manage each claim directly to limit its cost and E-Mod impact, and review whether a high-deductible structure fits your loss profile. The biggest single win for most mid and large employers is handling the claim actively from day one — creating an accurate medical record immediately and moving the worker back to light duty fast — so the claim closes at a fraction of its face value. The right mix depends on your history, premium volume, and industry.

What is an E-Mod and how does it affect my premium?

Your experience modifier is a multiplier built from three years of claim history versus your industry peers — above 1.0 raises premium, below 1.0 lowers it. Under NCCI's formula, frequency outweighs severity, so several minor claims hurt more than one large one. And because rates are sticky, a mod that climbs after a bad year rarely falls all the way back, which is why closing claims fast and clean matters so much.

Why is the real cost of a claim so different from the number I first see?

When an attorney gets involved you may hear a big figure — a "$250,000 claim." Left unmanaged, an insurer will often reserve and pay near that number. The actual medical spend on the same injury is frequently closer to $30,000, paid incrementally at roughly $1,500 to $2,000 a month and stopping when the worker recovers. The gap between those two numbers is what active claims handling protects. Individual results vary.

How does a return-to-work program lower costs?

Every day off the job generates wage-replacement dollars that inflate the claim and your mod. A light-duty transition — for example, an injured nurse moved into a receptionist-type role within weeks — stops that clock while the worker is still earning. Shorter disability means smaller reserves, lower E-Mod impact, and lower premium at renewal, compounding across three policy years.

What is a high-deductible workers' comp program and who benefits?

You take on a defined first layer of loss (say the first $200,000 of a $500,000 program) and the insurer covers the rest, which can roughly halve your premium. Retained claims are paid monthly as they age — on the order of $3,000 a month — and stop when the condition resolves. It works only with active claims administration behind it, and not every business qualifies: it fits employers whose real claim experience runs well below their mandated premium and who have the cash flow to carry the retained layer.

How does employee classification affect my premium?

Each role carries a class code with its own rate per $100 of payroll. Rate a low-risk clerical worker like a hands-on caregiver and you overpay on every dollar of that payroll — silently, until someone audits it. Segmenting the workforce by actual risk fixes it. California's WCIRB has found more than 10% of test-audited policies contain incorrect class codes, so an annual review routinely pays for itself.

What do you need to review my program?

Two documents: a copy of your current workers' comp policy and your five-year loss runs. With those we can quote coverage or evaluate taking it over, spot class-code and audit errors, and model whether a high-deductible or actively-managed structure would lower your total cost of risk. We respond within 24 hours.